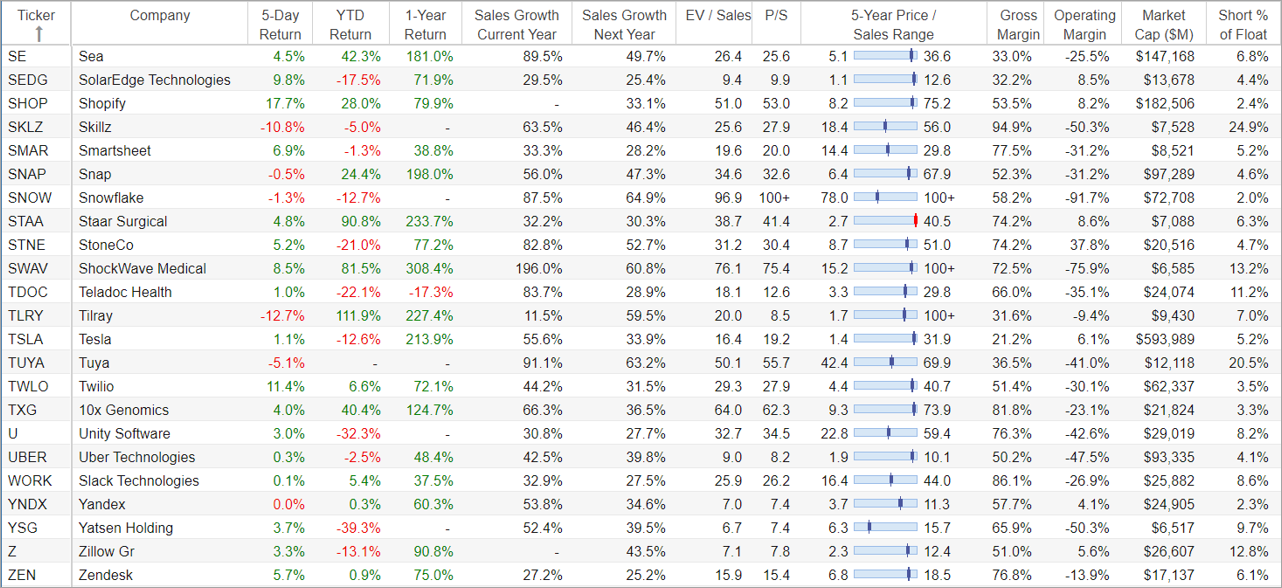

We’re going to kick this report off with a table of 50 top growth stocks (see below) to help frame the discussion, and to help us whittle our way down to three in particular that are highly attractive and worth considering for investment. You may recall, last week we shared a report on the 40 Biggest Safe Dividends (including 3 that are particularly attractive), and if you are looking for similar types of stocks, then this report is absolutely not for you. This report is focused on top growth stocks with massive long-term upside.

50 Top Growth Stocks:

To get right to it, here is the list:

source: StockRover, data as of 17-Jun-21, includes: (CRWD) (DOCU) (ENPH) (MELI) (NET) (MU) (PINS) (ROKU) (SE) (SNOW) (STNE) (TDOC) (U)

In order to qualify for inclusion in the above top growth stock table, we required a minimum expected revenue growth rate of 25% for next year. And if you scroll through the list, you’ll see many of them actually have much higher expected growth rates than that for this year and next. And if you are into top growth stocks, you’ll likely see a lot of names you’ve heard of, as well as a few names you haven’t.

We hope this table is helpful in that it provides additional metrics, such as valuation multiples, margins, market cap, price performance and recent short interest, to name a few. These can be useful metrics, but good investors require a much deeper dive.

A few things we look for in top growth stocks (besides high revenue growth trajectory, strong gross margins, and relatively reasonable valuation metrics) include large total addressable markets (“TAM”) so there is room to keep growing rapidly, industry leadership and strong leaders (often founders) running the business.

And to the chagrin of people that were into last week’s 40 top dividend stocks list, we do not look for strong earnings when we consider top growth stocks. This may sound counterintuitive to some people, but it’s not. In fact, it can be concerning if a top growth stock does have a lot of earnings, and it’s usually totally unacceptable if a top growth stock even pays a dividend.

Why?

Because top growth stocks are rapidly growing companies that have so much tremendous opportunity for growth that they should be plowing all of their financial resources into growing (revenues) because it can help them maximize long-term/future value. Again, this may sound counterintuitive, but its not. These are businesses racing to establish dominance in young but massive and rapidly growing industries so they can stay far ahead of the competition and enjoy the long-term benefits of being the dominant player.

Honorable Mention: Shopify (SHOP)

Before we get into the three particularly attractive top growth stocks for this article, we first review an honorable mention. Shopify is a top growth stock that currently trades at about $1,445 per share, and that we originally purchased in August 2018 for only about $142 per share. That’s a 9-bagger in less than 3 years.

Source: Ycharts

source: Blue Harbinger

Here are a couple excerpts from our report on Shopify back on August 8, 2018:

“Naysayers believe Shopify’s valuation is way too high, but they are making the classic Wall Street mistake of being way too shortsighted. The recent sell-off has created an attractive entry point.”

“Shopify is a rare and very powerful growth opportunity. It’s growing rapidly, and it is expected to keep growing rapidly considering its very large total addressable market (TAM) and its complete lack of any formidable competition. This is a powerful company in the right place at the right time. The shares can be volatile, and we just purchased shares on this latest pullback because we expect the price to increase dramatically in the years ahead.”

As you can see, Shopify exhibited back then, many of the qualities we look for in top growth stocks today. And technically speaking, even though Shopify is only an honorable mention in this report, it still exhibits many of the qualities you want to see in a top growth stock, the share price is below its all-time highs (thereby providing some margin of safety for “would be” buyers), and we do continue to own shares of Shopify today (with no intention of selling anytime soon). You can access our latest members-only report on Shopify here:

3 Top Growth Stocks Worth Considering:

So with that backdrop in mind, on to the three particularly attractive top growth stocks we want to share with readers.

NIO, Inc. (NIO)

NIO is a Chinese automobile company that designs and manufactures electric vehicles primarily targeting premium markets. And in addition to its very high growth rate (see earlier table) and very big TAM (so it can keep growing rapidly for a long time), there are a variety of things that make this one special, including its unique Battery as a Service (BaaS) solution (to address the challenging costs of electric vehicle batteries), supportive government policies, and its consistent improvement in top and bottom lines.

image source: NIO homepage

Of course, it does face risks (such as production slowdowns due to chip shortages, a rollback of subsidies and intense competition), however the massive TAM for electric vehicles leaves plenty of room for multiple players to succeed.

Source: Ycharts, data as of 17-Jun-21

Overall, this one is a leading play on the traditional engine to battery transition, and although we do not yet own shares, it is high on our watchlist. Here is how we concluded our recent full report on NIO:

“[NIO] has the potential to add significant long-term gains to your portfolio if you are patient and can handle some price volatility. We do not currently own shares, but we are considering nibbling at a very small long-term position based on this most recent share price pullback.”

Members can access our previous NIO report here:

Digital Turbine (APPS)

Digital Turbine Inc. (APPS) is another top growth stock worth considering. It is basically an on-device media platform which works with wireless carriers and device OEMs (original equipment manufacturers) to pre-install apps on new devices. And the company’s business is growing rapidly with a very large TAM to keep growing rapidly.

source: Seeking Alpha

If you don’t already know, the business model is for app developers to pay Digital Turbine for placement on phones, and this revenue is split with the carriers. This strategy basically allows Digital Turbine app developers to target specific customers across carriers (such as AT&T (T) and Verizon (VZ)).

Source: Ycharts, data as of 17-Jun-21

For some perspective on the size of this market, Digital Turbine’s technology platform has already been adopted by more than 40 mobile operators and OEMs, and has delivered more than 4.8 billion application preloads. Yet the industry remains young with multiple ways to grow (such as new IoT devices, new products and robust advertising demand) as the truly massive global digital transformation rolls on. We concluded our recent full report on Digital Turbine as follows:

“Digital Turbine is a compelling growth story benefitting from the burgeoning mobile app install advertising market. We see multiple catalysts for growth led by new devices, new products and robust advertising demand. The inherent operating leverage in the business model should continue to support margin expansion and free cash flow growth. The stock offers a compelling long-term investment opportunity for growth investors. We do NOT currently own shares of Digital Turbine, but we are considering a purchase.”

Digital Turbine and NIO are both currently included on our top growth stock watchlist, and as you can see in the excerpt below—performance has recently been strong.

Source: view this data in real time.

Palantir (PLTR)

Palantir is a software company that is growing rapidly and has a massive total addressable market (to keep growing for a long time). It provides big data analytics solutions (ranging from data mining to visual analytics), on a single consolidated platform, thereby enabling informed decision-making. The company is having great success landing and expanding government agency contracts, but is also recently attempting to diversify into enterprise-grade commercial organizations too.

Source: Ycharts, data as of 17-Jun-21

The share price has pulled back from all time highs in recent months, but with a forward price-to-sales multiple of over 30x—it appears expensive (even compared to other software peers) and many investors are still afraid. However, it is Palantir’s unique business and growth opportunity that make the shares significantly undervalued—if you are a long-term investor with the discipline to hang on through volatile patches in the market. For example, the high expected future revenue growth will help bring down the valuation multiples in the years ahead.

We also really like Palantir’s subscription model, its high gross margins, and its customizable solutions (which lead to a very sticky customer base).

If you are looking for more detailed information and analysis on Palantir (including it business model, its market opportunity, financials, valuation and risks) be sure to check out our new detailed report on Palantir here:

Important Takeaways:

It’s one thing to say you like top growth stocks with massive upside, but do you really have the discipline to stomach the volatility? For example, top growth stocks soared in 2020, but have taken a significant breather since mid-February of this year. On the other hand, dividend stocks are showing increasing signs of strength as vaccines roll out and inflation concerns rise, and you might instead prefer to consider our recent report titled The 40 Biggest Strong Dividends. However, at the end of the day, it’s critically important to know your goals as an investor and to then stick to opportunities that meet your own personal needs.

And also remember, compound growth is far more powerful than most people realize. Members can access all of our current holdings here.

We first purchased Shopify at ~$143 per share in August of 2018. It now trades at ~$333 per share. Not a bad return—until you realize the shares have fallen over 80% in the last 6 months! This report compares Shopify’s business fundamentals (including its business strategy, ongoing revenue growth and margins) to its current valuation, and then examines the question of whether Shopify CEO, Tobias Lütke, continues to imprudently push an easy-money, high-growth business strategy in an increasingly sober new market paradigm—now characterized by higher costs of capital and a starkly less friendly meme stock environment (yes—Shopify is a meme stock). We conclude with our opinion on who might want to invest—or if it’s simply time to sell and move on.