The Blue Harbinger Watch List contains information on attractive investment opportunities that we do not currently own, but may consider purchasing if/when market conditions are right. Without further ado, here is the list…

Saratoga Investment Corp (SAR): 9.2% Yield

Featured

Ares Capital (ARCC): 9.3% Yield

Featured

Stag Industrial (STAG): 5.8% Yield

Featured

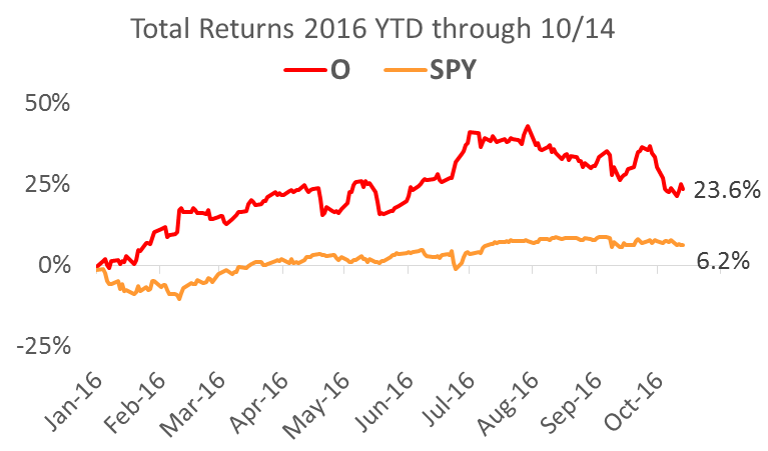

Realty Income (O): 4.4% Yield

Featured

Welltower (HCN): 5.2% Yield

Featured

Potash (POT): 2.0% Yield

Featured

Main Street Capital (MAIN): 6.1% Yield

We first wrote about the attractiveness of Main Street Capital back in May (read that report here), and it has since increased modestly in price. It also raised its already big monthly dividend. And what makes it particularly attractive right now is its recent selloff in November as the Fed signaled higher rates are coming and high yield equities (like Main Street) sold off in general. We also like its internal management team, as well as the possibility (and track record) of additional supplemental dividends, above and beyond the standard 6.8% dividend yield. Main Street announced earnings last week, and exceeded street expectations by $0.03 per share.

Country-Specific ETF: +2% Yield

Featured

Starwood Properties (STWD): 8.5% Yield

Featured

W.P. Carey REIT (WPC): 6.6% Yield

Featured

Want access to our current holdings and 100% of our members-only content? Consider a subscription...