In case you have been living under a rock, the stock market is down big, thanks (in large part) to turmoil caused by President Trump's new tariffs. Without arguing the pros and cons of these draconian tariffs, it has most certainly created a lot of fear. And fear creates opportunity. Like every other market crisis, we believe this too shall pass. But before it does, investors may want to take advantage of the attractive "buy low" sales prices it has created (in select big yield opportunities). This report ranks our top 7 big-yield investment opportunities (currently on sale) starting with #7 and counting down to our very top ideas.

So without further ado, let's get into it...

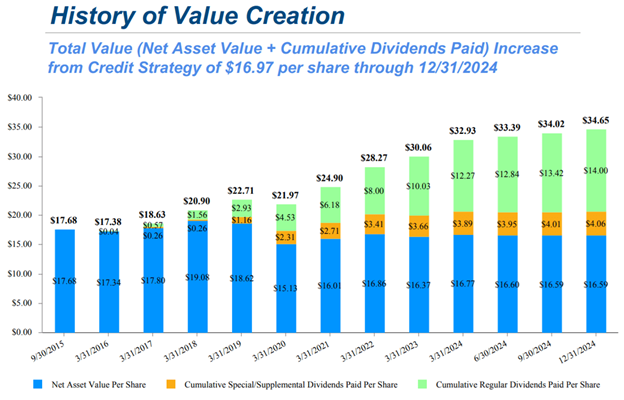

7. Capital Southwest (CSWC),Yield: 13.6%

CSWC is a big-yield (double-digit) middle-market lending firm (it’s a BDC) focused on supporting the acquisition and growth of middle-market companies across the capital structure. Based in Dallas and with only 33 employees, it's internally managed (this is important) and it has total balance sheet assets of around $1.8 billion.

Importantly, Capital Southwest has a strong history of creating value for investors through both a healthy net asset value and strong, growing dividend payments.

CSWC also has an investment-grade credit rating (Baa3 from Moody's and BBB- from Fitch) which is better than the companies it lends to, but also a benefit of being a diversified BDC with a strong balance sheet (and loans heavily tilted towards first lien, safer, at 98%).

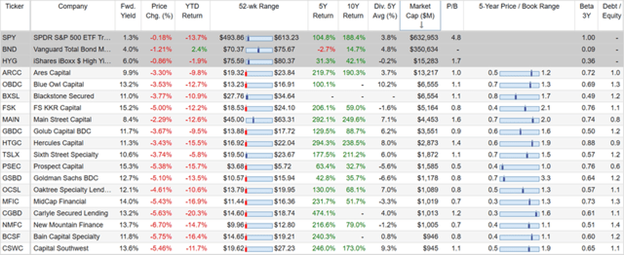

From a valuation standpoint, the shares are down over the last month (as investors react to net valuation write-downs of $0.54 cents per share to the debt portfolio, as several of its 118 portfolio companies were moved to tier 3 and 4 ratings, despite steady new deal flow continuing), and the shares now trade at only 1.1x book value, which is low by historical standards for this healthy internally managed BDC (see historical book value range in our earlier table).

If you have been waiting for a pullback in share price and price-to-book-value (“NAV”) for this healthy, long-term BDC, the recent market price declines provide you with some additional margin of safety.

6. Reaves Utility Income (UTG), Yield: 7.6%

The Reaves Utility Income Trust (UTG) is a special, utility sector focused, closed-end fund (“CEF”) offering big, tax-advantaged, monthly income (7.6% yield) and unique exposure to the AI datacenter megatrend, which has just pulled back and thereby offers some compelling price appreciation potential (not to mention it also trades at a small but attractive discount to net asset value (“NAV”)). This report reviews the fund’s strategy, holdings, distribution safety, valuation (and megatrend exposure) and risks, and then concludes with our strong opinion on investing.

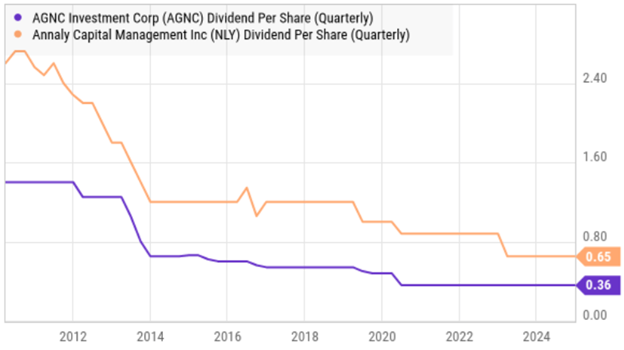

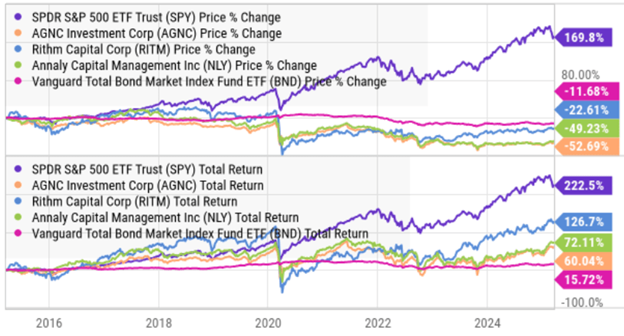

5. AGNC Investment (AGNC), Yield: 16.0%

To be clear, mortgage REITs (such as AGNC) are very different than property REITs. Specifically, where property REITs own mainly physical real estate properties, mREITs own real estate securities (such as those issued by US federal government agencies to fund home ownership).

Mortgage REITs generally offer higher yields than property REITs, but they also come with unique risks (such as higher leverage, or borrowed money).

In the case of AGNC, this mortgage REIT invests mainly in Agency Mortgage Backed Securities, which are considered particularly safe (they’re guaranteed by US government-sponsored agencies). However, AGNC uses significant leverage (recently 7.2x) to magnify the otherwise low returns on these securities, which also magnifies the risks (particularly when interest rates get choppy or when credit spreads widen).

As you can see in our earlier tables, AGNC (and other mREITs) offer attractive double-digit yields, but they also have a history of declining prices and dividend cuts over time.

So if you're going to invest in mREITs, be aware of the dividend and price dynamics (which are totally fine to some investors who just want the outsized dividends, despite the potential for declines over time), whereas others are turned off by the price declines and relatively lower long-term total returns.

A lot depends, of course, on market conditions and valuations (such as price-to-book values, which are currently attractive - sub-1.0x multiples - following the latest market "flash crash").

The Top 4

The Top 4 big yields are reserved for members only, and you can access them here: Top 7 Big Yields (Members-Only Edition). It includes an attractive mix of top ideas, offering steady big income and trading at attractive current prices.

Members can also access all 23 positions in our Blue Harbinger "High Income NOW" Portfolio (aggregate current yield is 9.6%).

The Bottom Line

If you like big steady income, and you are looking to take advantage of the current market turmoil, the big yield opportunities in this report are particularly attractive right now.

Of course there will be more volatility, but focusing on big yields can help you sleep better at night.

At the end of the day, you need to do what is right for you. And if you are a disciplined, long-term, income-focused investor, the big yields in this report are attractive and absolutely worth considering.