Omega Healthcare Investors (OHI) is an attractive, big-dividend (8.5%), real estate investment trust (REIT). Omega has delivered poor performance so far this year (as shown in our recent article: Big-Dividend Healthcare REITs, Ranking the Best and Worst) not only because of macroeconomic headwinds that caused REITs to pullback, but also because of heightened Affordable Care Act (ACA) uncertainty (especially following the recent U.S. elections), and because of the market’s overly pessimistic view of skilled nursing facilities (for example, short-interest is significantly high). We believe these three big risks (i.e. macroeconomic headwinds for REITs, ACA uncertainty, and overly pessimistic sentiment) have created an attractive opportunity for diversified long-term investors.

Overview

Omega is a triple-net equity REIT that provides financing to support Skilled Nursing Facility (SNF) operators. And considering the shifting demographics of the US population, Omega has a big tailwind at its back that will help it going forward as shown in the following charts.

And the following map provides information on the well-diversified locations of Omega’s properties.

This next table provides additional information on the diversified nature of Omega’s investments by dollars, geographic location and occupancy.

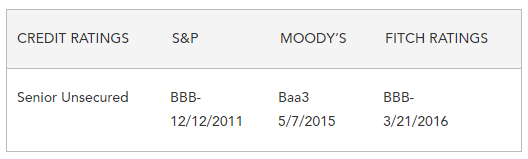

And worth noting, Omega maintains healthy investment grade credit ratings (as shown in the following table).

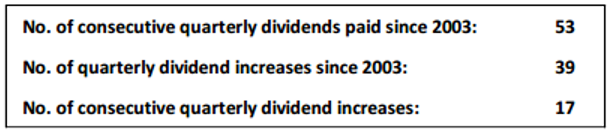

Also worth noting, Omega has an outstanding dividend payment record as shown in the following graphic.

Despite all of the good things Omega has going for it, the share price has declined and underperformed this year as shown in our earlier performance chart.

Macroeconomic Headwinds

One of the reasons why Omega has underperformed recently is macroeconomics. Specifically, real estate securities (and high dividend stocks in general) have sold off as the outlook for growth continues to improve, especially following the recent US elections. With regards to growth, investors have rotated from low volatility stocks (such as REITs) and into “growthier” investments such as financials and industrials. This rotation has caused REITs (such as Omega) to underperform the rest of the market as shown in the previous total returns chart. Another macroeconomic reason REITs have sold off is because they generally use a fair amount of debt (see debt bar chart below) to fund their businesses, and interest rates are increasingly expected to rise which will make operations more expensive for REITs. However, Omega’s business remains healthy and its valuation is attractive (more on valuation later).

Affordable Care Act Uncertainty

Another reason Omega has sold off is uncertainty about the future of the Affordable Care Act. Expansion of government mandates has continued to weigh heavily on the stock throughout 2016, and new uncertainties have arisen following the recent US elections whereby the Republican controlled House, Senate and Presidency seem determined to repeal (or at least modify) the ACA. Omega describes these risks extensively in its annual report. For example:

Healthcare Reform

A substantial amount of rules and regulations have been issued under the Patient Protection and Affordable Care Act, as amended by the Health Care and Education and Reconciliation Act of 2010 (collectively referred to as the “Healthcare Reform Law”). We expect additional rules, regulations and interpretations under the Healthcare Reform Law to be issued that may materially affect our operators’ financial condition and operations.

Government Regulation and Reimbursement

The healthcare industry is heavily regulated. Our operators are subject to extensive and complex federal, state and local healthcare laws and regulations. These laws and regulations are subject to frequent and substantial changes resulting from the adoption of new legislation, rules and regulations, and administrative and judicial interpretations of existing law. The ultimate timing or effect of these changes, which may be applied retroactively, cannot be predicted. Changes in laws and regulations impacting our operators, in addition to regulatory non-compliance by our operators, can have a significant effect on the operations and financial condition of our operators, which in turn may adversely impact us.

Reimbursement Generally

A significant portion of our operators’ revenue is derived from governmentally-funded reimbursement programs, consisting primarily of Medicare and Medicaid. As federal and state governments focus on healthcare reform initiatives, and as the federal government and many states face significant current and future budget deficits, efforts to reduce costs by government payors will likely continue, which may result in reductions in reimbursement at both the federal and state levels. These cost-cutting measures could result in a significant reduction of reimbursement rates to our operators under both the Medicare and Medicaid programs. Additionally, new and evolving payor and provider programs, including but not limited to Medicare Advantage, dual eligible, accountable care organizations, and bundled payments could adversely impact our tenants’ and operators’ liquidity, financial condition or results of operations. We currently believe that our operator coverage ratios are adequate and that our operators can absorb moderate reimbursement rate reductions and still meet their obligations to us. However, significant limits on the scopes of services reimbursed and/or reductions of reimbursement rates could have a material adverse effect on our operators’ results of operations and financial condition, which could adversely affect our operators’ ability to meet their obligations to us.

Medicaid

State budgetary concerns, coupled with the implementation of rules under the Healthcare Reform Law, may result in significant changes in healthcare spending at the state level. Many states are currently focusing on the reduction of expenditures under their state Medicaid programs, which may result in a reduction in reimbursement rates for our operators. The need to control Medicaid expenditures may be exacerbated by the potential for increased enrollment in Medicaid due to unemployment and declines in family incomes. Since our operators’ profit margins on Medicaid patients are generally relatively low, more than modest reductions in Medicaid reimbursement or an increase in the number of Medicaid patients could adversely affect our operators’ results of operations and financial condition, which in turn could negatively impact us.

Medicare

On April 1, 2014, President Obama signed the “Protecting Access to Medicare Act of 2014” which calls for the United States Department of Health and Human Services (“HHS”) to develop a value based purchasing program for SNFs aimed at lowering readmission rates beginning on October 1, 2018.

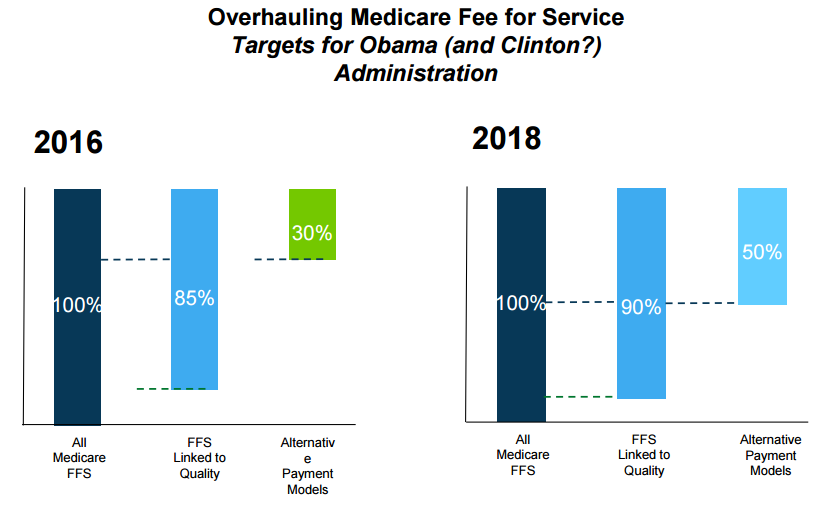

And for additional perspective, on November 2nd (one week prior to the election) Omega’s 2016 Investor Day presentation included the following charts which suggest the company’s expectation of an expanding Affordable Care Act

In particular, Alternative Payment Models and Medicare Advantage were expected to increase, but now the rate of that expansion is in question following the election, and this could be a good thing for the profitability of Omega’s operators and ultimately Omega. As mentioned in the annual report excerpt (above) “[N]ew and evolving payor and provider programs, including but not limited to Medicare Advantage, dual eligible, accountable care organizations, and bundled payments could adversely impact our tenants’ and operators’ liquidity, financial condition or results of operations.”

Worth considering, the following table shows how much of Omega’s operator revenues come from government programs, Medicaid in particular.

These percentages help quantify the material impact government programs have on Omega’s business, and lower regulatory burdens (more free markets) under Republican lawmakers may bode well for Omega over the long-term.

Overly Pessimistic Investors

Another reason that Omega has underperformed is overly pessimistic investors. For starters, short interest recently exceeded 12%.

This high level of short-interest is indicative of investors’ aversion to ACA uncertainty, as well as fears related to rising interest rates and sector rotation out of high dividend stocks such as REITs. Additionally, many income-investors in general invest in REITs for their stability (in addition to the dividends) and Omega appears more risky than other REITs because of the high level of regulatory uncertainty surrounding skilled nursing facilities (i.e. many income-investors have favored other healthcare REITs- a good thing for contrarians interested in Omega).

The current high dividend yield is another indication of overly pessimistic investors. Specifically, management has historically allowed the dividend yield to hover around approximately 6%, but it raises and lowers as the stock price becomes undervalued and overvalued, respectively, in our view (see chart below for historical dividend yield). We believe the current high dividend yield is a signal that the stock is undervalued, and management has the confidence that they’ll be able to keep paying it (and raising it) in the future.

Valuation

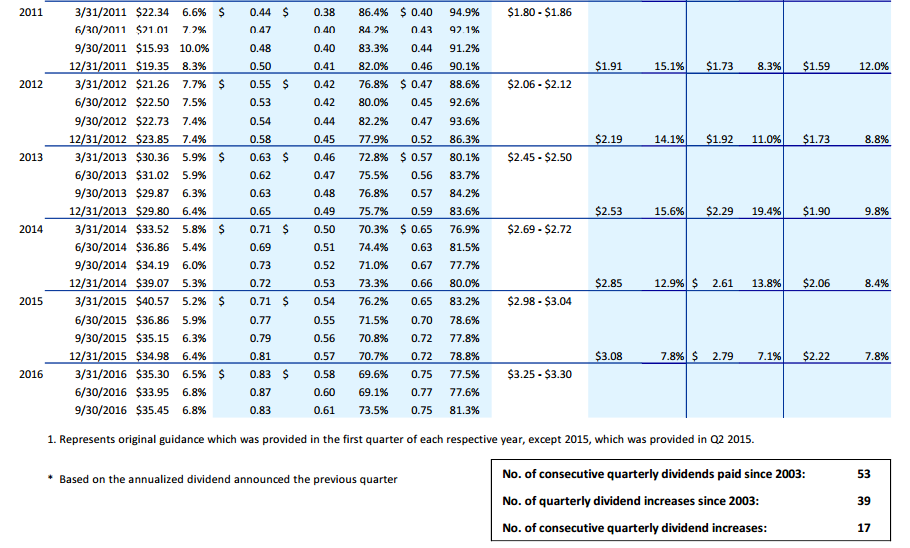

The above data table provides a variety of useful information in gauging Omega’s value. For example, Omega’s Adjusted Funds from Operations (AFFO) and Funds Available for Distribution (FAD) both continue to grow. Additionally, the FAD payout ratio is relatively low by historical standards (indicating a strong and healthy dividend). And management continues to exceed its own AFFO guidance, and it appears it will again this year (2016) as management has again raised guidance above its original estimate.

And worth re-mentioning, Omega has demographic tailwinds at its back (a growing aging population), as well as the potential for regulatory benefits too (i.e. less costly entitlement regulation) following the recent US elections.

Conclusion

Without question, Omega faces uncertainty. However, three of the biggest risks (macroeconomic headwinds, ACA uncertainty, and overly pessimistic investors) have created an attractive opportunity, in our view. The valuation is attractive, the big dividend is safe and growing, and Omega could be a very valuable addition to a well-diversified, long-term, income-focused, investment portfolio.