I believe in owing a prudently diversified portfolio of long-term investments. However, if I could own only one stock, I’d want it to be something with with a lot of growth, value, steady cash flow, and competent leadership. Microsoft (MSFT) fits that bill. Under the leadership of Satya Nadella, Microsoft has experienced an impressive turnaround in recent years whereby its top-line growth has been fueled by its cloud computing solutions (which continue to gain ground on Amazon Web Services (AMZN)). And although the valuation appears higher compared to its own history, it has transformed itself from a boxed product seller to a subscription-based SaaS provider, thereby warranting a higher valuation (i.e. Microsoft is still inexpensive versus its peers). Not to mention, the company’s massive steady cash flow creates a lot of opportunity and eliminates a lot of risk. In this report, we analyze Microsoft’s business model, its market opportunities, competitive positioning, valuation, risks, and finally conclude with our opinion on investing.

Overview:

Microsoft offers a variety of software and hardware solutions for both commercial and personal use. Co-founded by Bill Gates and Paul Allen in 1975 as an operating system developer, Microsoft was listed as a publicly traded company in 1986 and has grown to become one of the largest tech companies with a market cap of over $1.6 trillion. Since the 1990s, Microsoft has cemented its position as the market leader in the operating systems space with its Windows OS and has also diversified into other business segments via LinkedIn, Xbox devices, and its Azure platform.

Microsoft conducts its business through three operating segments: -

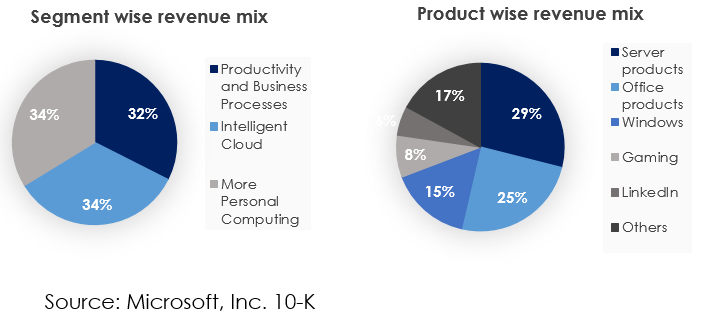

Productivity and Business Processes: This segment primarily consists of productivity, communication, and information services solutions offered by Microsoft. Revenue in this segment is generated from commercial or consumer subscriptions to Office 365, as well as licensing of its suite of productivity and cloud solutions such as Teams, SharePoint, Exchange, Skype, Office 365 security, outlook.com, and OneDrive. This segment also includes Microsoft’s social media platform LinkedIn along with cloud-based ERP and CRM solutions. The segment contributes 32% to the overall top-line of the company and generates an operating margin of 40%.

Intelligent Cloud: This segment consists of all server products and cloud solutions offered by the company, which include Azure, SQL server, Windows Server, Visual Studio, System Center, GitHub, etc. This is the fastest growing segment for Microsoft and accounts for 34% of total revenue. Operating margin of this segment stands at 38%.

More Personal Computing: This segment houses products and services that deliver personal user experience. The products include the Windows operating system, Surface and Xbox. This segment also contributes 34% to total revenue of the company but generates relatively speaking lower operating margin of 33% as it includes more hardware-based solutions.

In terms of product exposure, server products account for 29%, followed by Microsoft office products which contribute 25% to the topline.

Although all segments have shown impressive performance in recent years, a significant portion of the growth has been driven by the Intelligent cloud segment which houses Microsoft’s cloud computing Azure business. As business digitalization and cloud-based solutions expand globally, there has been an increasing demand for cloud computing platforms such as Azure, which provide analytics, virtual computing, storage, networking, and other solutions without the need for costly, inflexible on-premise server infrastructure.

Industry leading position in business productivity software and operating system segments

Microsoft has consistently maintained a dominant position in the PC operating system segment since the launch of its first IBM compatible DOS version in 1980s and is continuing to cement its near monopolistic position in the desktop/laptop userbase. While the company has observed a slight loss of market share to Apple’s mac OS, Windows OS still remains the leader with a global market share of over 85% as per netmarketshare.com. MacOS stands at a distant second position with a share of just 8%. Windows 10, which is the latest OS version released by Microsoft is now used by approximately 60% of the global Desktop/Laptop users. Once a user adapts to an operating system, it becomes an integral part of computer workflows, and switching to alternatives may not be viable given additional effort required to learn new functions. Given these dynamics, we believe the company’s dominance in the PC/Laptop operating system segment is secure in the near to medium term.

Having said that, it is important to note that Microsoft significantly lags its counterparts in the fast-growing mobile operating system market. Smartphones have seen significantly faster growth than desktop/laptops in recent years and Google Android has emerged as the clear winner in the handheld devices O/S space with a market share of over 70%. Apple’s iOS which functions on iPhone and iPad hardware has a market share of around 29%. Microsoft entered the smartphone OS business with a tie-up with Nokia and later went on to acquire Nokia’s mobile division in 2013 for around $8 billion. However, this business acquisition turned out to be a failed experiment. Later in 2015, Microsoft announced discontinuance of its mobile OS segment as it was unable to get mobile app developers on board.

While the company’s mobile OS business has been weak, it has made solid progress on making its productivity suite cloud friendly. With increased demand for cloud-based software solutions, the company released Office 365. Besides several new features, Office 365 also includes cloud computing integration that allows users to easily share, collaborate, and co-author work through files centrally stored in the cloud. Apart from improved efficiency, Office 365 also provides improved security and is cost effective, especially for enterprise customers. Also, Office 365 is offered through a subscription-based business model that provides sticky and recurring cash flows to the company. Revenue from Office 365 overtook the on-premise Office suite back in 2017 and it has become the most used enterprise cloud software solution globally. One quarter of Microsoft’s top-line is made up of Office products and revenue is increasing at a growth rate of 13% with expanding user adoption. The company faces competition from G-Suite which is Google’s cloud friendly version of Office. However, through constant innovation and upgradation to its Office suite, Microsoft still occupies a significant share of the business productivity solutions market.

Gaining share in the cloud computing market

Microsoft offers its cloud computing services through its Azure platform. Azure is the fastest growing product segment for the company and has remained the driving force behind Microsoft’s impressive financial performance in recent years. Azure is a cloud computing service which provides a platform for creating, testing, deploying, storing, and managing applications and services through its managed data centers located all over the globe. It is a flexible platform in that users can scale computing resources as per their needs.

Cloud computing is a rapidly growing technology market segment. The primary driver behind this strong growth is the push towards business digitalization along with efficiency. Cloud allows organizations to access software, computing power, and other applications without the need for in-house hardware infrastructure, thus leading to reduction in large scale capital expenditure investments and maintenance. As per Statista, the global cloud services market size currently stands at $258 billion and is expected to expand to over $364 billion by 2022, translating into a CAGR of around 15%. Please note that Azure is not only growing at a fast pace in absolute terms, it is also significantly outperforming its peers.

Amazon Web Service (AWS) is the largest player in the cloud computing space with 33% of worldwide market share. It enjoys the first mover advantage and was launched in 2006 whereas Microsoft played catch up by launching Azure in 2010. Despite that initial disadvantage, as evident in the chart below, Azure has been slowly taking market share from AWS. Although AWS and Azure provide almost the same service specifications, Azure provides better hybrid cloud capabilities i.e. users can easily move between on-premise data centers and Azure’s public cloud infrastructure. Also, since most of the organizations already have agreements with Microsoft for use of software such as Office suite or Windows OS, they are entitled to receive loyalty discounts for availing Azure services. Additionally, the cloud infrastructure market segment has been undergoing consolidation. The market share of top 3 vendors has increased from 51% in 2017 to 60% by Q2 2020. This market share movement highlights that scalability is important in cloud IaaS business and service providers that can consistently invest capital in building an increasing number of data centers will continue to garner additional market share.

Source: Statista

More recently, the COVID-19 pandemic has accelerated the need for Cloud solutions as global organizations are pushing for digital transformation and see cloud platforms as a logical solution to achieve business continuity in the post pandemic new normal of social distancing and work from home. During Microsoft’s most recent Q3 earnings call, CEO Satya Nadella had this to say:

“As COVID-19 impacts every aspect of our work and life, we have seen two years’ worth of digital transformation in two months. From remote teamwork and learning to sales and customer service, to critical cloud infrastructure and security, we are working alongside customers every day to help them stay open for business in a world of remote everything. There is both immediate surge demand, and systemic, structural changes across all of our solution areas that will define the way we live and work going forward.”

Continuous Innovation and Opportunity

One thing Microsoft has Not done is to rest on its laurels. The company has continued to innovate, especially under the leadership of Satya Nadella, and it has the cash flow to keep innovating in the future (more on cash flow later). Aside from expanding beyond its Windows operating system and into the cloud-based digital transformation, Microsoft constantly looks for new opportunities. For example, Microsoft recently attempted (unsuccessfully) to team with Walmart (WMT) to acquire video social media company, TikTok. It has also recently partnered with Datadog (DDOG), and launched services to complete with Twilio (TWLO) and Amazon (AMZN). The two important points here are that (1) Microsoft continues to innovate and evolve with the market (a very good thing) and (2) it has more than enough steady cash flow to keep doing it (also a good thing).

Strong operating performance despite COVID challenges

Microsoft reported revenue of $38 billion in FY Q4 2020, which represents a constant currency growth of 15% on a YoY basis. Growth in Office suite license purchases remained suppressed in Q4 because of reduced purchases by small and medium sized enterprises as they curbed operational expenditures. Slow growth in the productivity and business processes segment was offset by strong expansion in the personal computing segment because of increased demand for gaming consoles and surface devices as people stayed at home during the pandemic. The slated release of Xbox Series X and Surface devices later this year is expected to provide a further boost to this segment in the coming quarters.

Intelligent cloud continued to remain the fastest growing segment for Microsoft as the Azure business saw a YoY increase of 50%. Investors must note that this was the weakest growth Azure has reported since its launch which suggests that Microsoft’s cloud computing business has started to mature. Having said that, we believe that a 50% top-line increase on such large base is commendable. Azure is still growing at a faster rate than both Google cloud and AWS implying that Azure continues to take market share. The strong push for business digitalization in the post-pandemic world and rise in demand for cloud infrastructure will provide enough ammunition to Azure in near to medium term.

Strong Cash Position and High Margins

On the profitability front, Microsoft continues to expand its operating margins as it grows its higher margin businesses such as Intelligent cloud and business productivity solutions. Its operating margin has expanded from just 25% in FY 17 to 37% in FY 20. Besides, it is a cash rich company and generates a significant amount of cash flows. In FY 20, Microsoft generated free cash flow of $43 billion which represents a YoY increase of 20%. Please note that the company has been consistent in returning cash back to the shareholders. In FY 20, Microsoft distributed $38 billion to its shareholders in the form of dividends and share buybacks, which translates into a payout ratio of 89% in terms of free cash flow. The company ended the year with a net cash position of $73 billion which we believe puts Microsoft in a robust position as far as financial stability is concerned. It has more than enough sources to fund potential acquisitions (such as the failed TikTok acquisition) without impacting the quality of its balance sheet in a meaningful way.

Valuation: Shift to SaaS-based business warrants multiple expansion

Microsoft’s valuation multiples have been consistently expanding over the last few years. The stock is currently trading at a Price to Sales multiple of over 11.4x and EV to EBITDA of 23.5x which is at the higher end of its valuation range.

This is primarily because under the leadership of Satya Nadella, Microsoft has transformed itself from a boxed product seller to a subscription-based Software-as-a-service (“SaaS”) provider through its several cloud-based applications including Office 365 and Azure. Apart from rekindling top-line growth, this shift has helped the company achieve higher margins and more predictable cash flows. Therefore, while Microsoft’s valuation has expanded over the years, it is for justifiable reasons and relative to other SaaS subscription peers (NOW) (ADBE) (CRM) (SAP) (ORCL) it is still trading at reasonable multiples.

Risks

Competition: Microsoft faces significant competition from Amazon (AMZN) and Alphabet (GOOGL) in the cloud computing space. Intensifying competition may force all players, including Microsoft, to reduce pricing for their services in order to maintain market share which will impact segment margins.

Prolonged business spend slowdown. A deep and protracted slowdown in corporate spending will impact the company’s growth momentum despite strong digital transformation tailwinds. Having said that, we believe any slowdown is likely to be temporary and the company’s strong balance sheet provides it with enough staying power.

Valuation: As mentioned, Microsoft’s valuation is near the higher end of its historical range. However, this is primarily because it has wisely transformed itself from a boxed product seller to a subscription-based SaaS provider, thereby warranting a higher multiple. Furthermore, relative to peers, Microsoft is relatively less expensive, especially considering its strong growth trajectory.

Conclusion

Microsoft is one of the largest technology companies in the world. It has consistently delivered strong top and bottom line growth in recent years (primarily through the success of its SaaS and public cloud solutions). Further, the company has ample growth opportunities as it continues to ride the cloud trend for the foreseeable future.

Like many top growth stocks I follow, the share price has experienced a slight price pull back over the last month thereby creating some margin of safety, but if you are still concerned the valuation multiples are too high, you might consider an income-generating options trade that gives you a chance to pick up the shares at a lower price and generate attractive upfront premium income for you to keep (such as this one).

Overall, the business continues to have plenty of long-term price appreciation potential, while also exhibiting the factors I’d look for if I could only own one stock, such as high-margin revenue growth (Microsoft actually received an honorable mention on my top 10 pure growth stocks list), attractive valuation, abundant cash flow and competent leadership. I am currently long shares of Microsoft (in my 27-stock Disciplined Growth portfolio), and I have zero intention of selling anytime soon.