New Senior is a small equity REIT, operating in the highly-fragmented, but very large and rapidly growing senior housing space. New Senior is struggling with a heavy debt load (they’re trying to sell more assets to pay down debt), and they’re also struggling with a small handful of troubled operators. It seems if New Senior can get through near-term challenges then there are plenty of healthy profits (and dividend payments) ahead, and for this reason we've ranked it #14 on our list of "15 Attractive +7% Yields Worth Considering".

However, considering New Senior’s external management group was recently acquired by a large, deep-pocketed, Japanese firm (Softbank) that is looking to deploy cash, there may be a more direct way for New Senior to get through its near-term challenges. In our view, there are clear benefits (the cost of debt could be dramatically lowered) and incentives (there are significant “economies of scale” opportunities in the large and growing senior housing space) for Softbank to acquire New Senior at healthy premium to its current market price.

About New Senior

New Senior Investment Group (SNR) is a publicly-traded real estate investment trust (“REIT”) with a diversified portfolio of senior housing properties (managed properties and triple net leased) located across the United States.

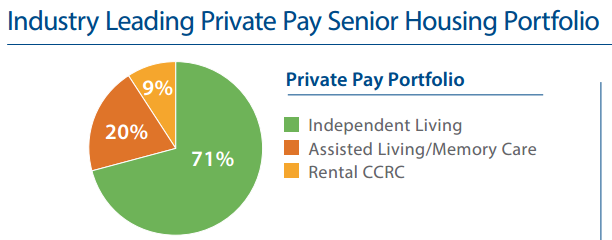

Very Importantly, New Senior relies on private pay sources of revenue which are considering more stable and predictable compared to government reimbursed property types which rely significantly on payments from Medicaid or Medicare. For this reason, New Senior is dramatically less sensitive to healthcare law changes that currently weigh heavily on peers, such as Omega Healthcare (OHI), for example.

The property mix includes mainly Independent Living and Assisted Living properties.

The company recently released its fourth quarter financials which show strong improvement in net operating income, but the company continues to struggle with debt and negative earnings.

According to the earnings release: “The year-over-year decrease in the fourth quarter net loss was primarily driven by a gain on sale of real estate of $13.4 million and a decrease in expenses of $6.8 million.” Specifically, New Senior sold $38.5 million in assets over the last six months and the proceeds were used to pay down debt.

Also, as noted by the company, it is currently considering strategies to deal with five trouble operators.

When asked during the fourth quarter earnings call about the five underperforming assets, New Senior CEO, Susan Givens, explained: “So of those five, I think, we have a few that we’re actually considering selling and a few that we’re working with either our existing operators, or in certain cases, considering transitioning to new operators to try to improve performance.”

The Dividend

Many investors at attracted to New Senior because of its big dividend yield (currently 10.2%). However, the dividend does not have a large margin of safety. For example, New Senior’s quarterly dividend payment is 26 cents per share, but its Adjusted Funds From Operations (AFFO) and Funds Available for Distribution (FAD) just barely cover the divided, as shown in the following table.

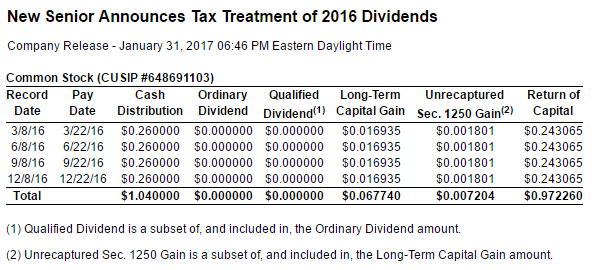

And worth noting, the tax treatment of the most recent dividend (as shown in the following table) was largely a return of capital, not a qualified dividend (this means you defer the tax payment until you sell the shares, unless your cost basis has been totally returned to you before then).

New Senior’s Management

There are a lot of interesting things going on with New Senior’s management and leadership team. For starters, New Senior has no employees. The company is externally managed and advised by FIG LLC, an affiliate of Fortress Investment Group LLC, which is a leading global investment management firm. Further, affiliates of Fortress manage private equity funds that currently own a majority of New Senior’s largest tenant, Holiday. And Blue Harbor, New Senior’s second largest tenant, is also an affiliate of Fortress. So there are some significant conflicts of interest here.

Additionally, New Senior’s CEO, Susan Givens, is also a Managing Director in Fortress’s Private Equity group. Further, the chairman of New Senior’s board, Wesley Edens, is a principal and a Co-Chairman of the Board of Directors of Fortress Investment Group. Further still, New Senior board member, Michael Malone, is a former Fortress Managing Director.

More interesting still, Fortress recently announced it will be acquired by Japanese technology giant SoftBank Group for about $3.3 billion in cash. In our view, it is critically important to consider the intentions of Softbank before investing in New Senior.

The Opportunity

With Sofbank now basically calling the shots at New Senior (because Softbank now essentially owns New Senior’s external manager and board of directors via Fortress), it’s important to consider New Senior from the perspective of Softbank. From Softbank’s perspective, New Senior is very small (New Senior’s market cap is less than $1 billion, Softbank’s is around $77 billion), but New Senior does fit into a larger growing real estate play by Softbank which includes not only its management interest in New Senior but also its ownership and management of New Senior tenants and Fortress affiliates Holiday and Blue Harbor. And according to the Wall Street Journal article:

“SoftBank believes it can double Fortress’s assets in the next few years, partly by shopping its funds to [its]… network of sovereign funds and global billionaires, according to people familiar with the matter. It plans to sell a slice of Fortress’s operating unit, known as the general partner, to some in that network, the people said.”

In our view, this suggests a consolidation of real estate interests is on the table considering the large growing industry opportunities, potential economies of scale, and Softbank’s desire for growth. For example, if Softbank were to acquire New Senior, it could easily refinance its debt and increase its profitability almost immediately. Also, a deep-pocketed Softbank could eliminate the liquidity concerns of many New Senior investors, thereby reducing the perceived risks, and increasing its valuation. Further, the long runway for growth and consolidation in the senior living industry fits Softbank’s growth aspirations in terms of the large size of the opportunity.

For perspective, according to New Senior’s annual report:

We believe that the rapidly growing senior citizen population in the U.S. will result in a substantially increased demand for senior housing properties as the baby boomer generation ages, life expectancies lengthen and more health-related services are demanded. The U.S. Census Bureau estimates that the total number of Americans aged 65 and older is expected to increase from approximately 47.8 million in 2015 to 79.2 million by 2035, with the number of citizens aged 65 and older expected to grow at four times the rate of the overall population by 2035. Healthcare is the largest private-sector industry in the U.S., with healthcare expenditures in the U.S. accounting for approximately 17% of gross domestic product in December 2013.

And for further prospective, also according to New Senior’s annual report:

We believe there are significant investment opportunities in the U.S. senior housing market driven by three factors: (i) growing demand from significant increases in the senior citizen population, (ii) highly fragmented ownership of senior housing properties among many smaller local (“mom and pop”) and regional owner/operators and (iii) operational improvement opportunities to increase property-level net operating income leveraging the experience and economies of scale of our Manager. We estimate the size of the senior housing industry in the United States to be approximately $300 billion, and, according to the 2015 American Seniors Housing Association 50 Report, approximately 58% of these senior housing facilities are owned by mom and pop operators with 5 or fewer properties. Given our strong track record of external growth, we believe an opportunity exists to continue to participate in the consolidation of this fragmented industry as many of these smaller owner/operators may decide to sell their portfolios. An attractive investment opportunity exists to acquire high quality properties where operational performance can be improved by leveraging the experience of our Manager.

Valuation:

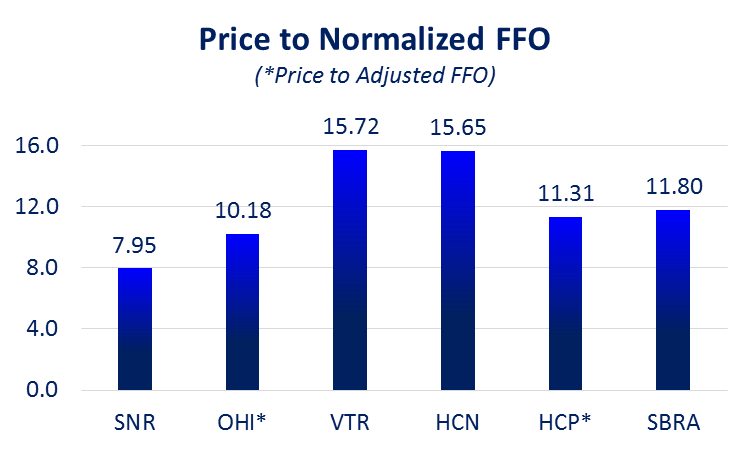

Relative to healthcare REIT peers, New Senior is trading at a very low price. For example, the following chart shows SNR’s low price relative to funds from operations (FFO) compared to some of it healthcare REIT peers.

These are all healthcare REITs, so it’s NOT an apples to oranges comparison, but it is a Macintosh to Granny Smith comparison. For example, New Senior (SNR) is focused exclusively on senior housing whereas Welltower (HCN) is diversified across senior housing, post-acute communities, and outpatient medical properties. Also, SNR deals with private pay operators, whereas the skilled nursing facilities of Omega Healthcare (OHI) are very sensitive to healthcare reforms as they pertain to Medicaid. Regardless, New Senior is very cheap relative to peers.

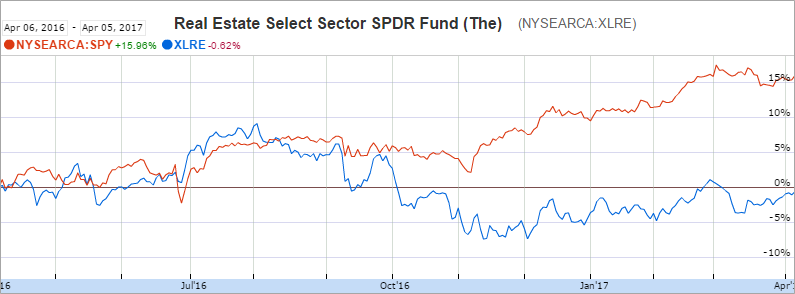

Another valuation consideration is the impact of rising interest rates on the real estate sector, in general. As the following chart shows, publicly traded real estate (as measured by the real estate sector ETF) has significantly underperformed the S&P 500 (SPY) over the last year.

Many investors fear that rising rates will negatively impact the real estate sector which relies on borrowing to fund its operations. Also, many dividend stocks in general have fallen out of favor as the pro-growth “Trump Rally” has continued to run. In our view, investor fear is already baked into prices, and REITs currently provide an attractive contrarian opportunity, especially for income-focused investors.

The Risks

In our view, New Senior is ripe to be acquired, but obviously there is no assurance that this will happen. And if New Senior isn’t acquired by someone with deep pockets, then it will be challenging for the company to pull itself up by its own bootstraps to get its debt under control and maintain its dividend.

As we mentioned earlier, there is very little margin of safety with New Senior’s dividend payments considering they consume essentially all of the company’s AFFO and FAD. And if New Senior cannot get its debt under control (by selling more asset) and by dealing with its troubled operators, then the company runs the risk of being forced to cut its dividend (a very bad thing from the vantage point of many income-focused investors).

Another risk is that its business is highly concentrated among two large tenants (Holiday and Blue Harbor). If something goes wrong with one of these tenants then New Senior could face dire challenges.

Further, New Senior’s business is not diversified as they focus very specifically on senior housing. If this industry suffers a significant downturn (or less growth than New Senior investors are anticipating) then the company could suffer significant losses.

Conclusion:

Without question, New Senior faces uncertainties. This is a huge dividend REIT that may experience significant price appreciation if it can get its debts and troubled operators under control. It can also experience significant price appreciation if it is acquired at a premium to its current market price, as we believe it is ripe for such an acquisition. However, if none of these positives occur then the company could face a dividend cut or further price declines.

The good news is that New Senior’s stock price is already extremely cheap considering the high risks have already been priced in, in our view. If you are looking for a big dividend healthcare REIT that is less correlated to the risks of healthcare reform, is trading at a very low price, and has significant near-term and long-term price appreciation potential, we believe New Senior is worth considering for an allocation within your diversified, long-term, income-focused investment portfolio.