If you are looking for a high yield business development company trading at an attractive price then Medley Capital Corporation (MCC) is worth considering. Even though this company may need to cut its dividend modestly over the next six months (because its net investment income and dividend coverage ratio are both trending lower), we expect the share price is resilient, especially considering it already trades at a discounted price versus its book value. For this reason, we've ranked Medley #12 on our recent list of "15 Attractive +7% Yields Worth Considering." More specifically, given its diversified portfolio, attractive positioning for rising interest rates, and our current position in the market cycle, we believe Medley Capital will continue to provide very attractive dividends for income-hungry investors.

About Medley

Medley Capital Corporation (MCC) is an externally managed business development company (“BDC”). The company’s objective is to generate current income and capital appreciation by lending to privately-held middle market companies.

Medley’s investments are currently diversified across a variety of industries, geographies and investment types, as shown in the following graphic.

Further, the company’s portfolio is well-diversified by issuer.

And very importantly, Medley is well-positioned for a rising interest rate environment considering it has transitioned the majority of its assets to floating rate and its liabilities are increasingly fixed rate.

This is important because as interest rate expectations continue to increase, Medley is ready.

The Market Cycle

The current rising interest rate environment is a good reminder of where we are in the market cycle and how this will impact Medley. For starters, the reason interest rates are so low is because we are still in the process to returning to more normal market conditions following the financial crisis. More specifically, the distressed conditions of the financial crisis created high yield opportunities for Medley and BDCs in general. As banks were being forced to de-risk, BDC’s were the only viable financing option for many distressed companies. And this resulted in the high yields and asset appreciation that many BDCs experienced in the years following the financial crisis as distressed companies recovered. However, now that the distress is largely gone, so too are many of the highest yielding opportunities, and BDCs (including Medley) are repositioning their investments accordingly. Specifically, BDCs are taking on less risk, and as a result they are being forced to lower their return expectations and in some cases their dividends.

Medley’s 11.5% Dividend Yield

As you may be aware, Medley lowered its quarterly dividend last summer to $0.22 per share from $0.30 per share. In our view, this reduction was prudent given the company’s decreasing net investment income (driven by the market cycle), and the market agreed with us as Medley’s stock price barely budged when the lower dividend was announced.

For perspective, Medley used to provide a chart of its net investment income and dividend payout ratio in its quarterly investment presentations up until September of 2015 when the ratio started look less favorable thereafter.

For reference, Medley’s dividend exceeded its net investment income in four out of the next five quarters (not good!) since they stopped including the above chart in their quarterly investor presentations. Specifically, in the quarters ending December 2015 through December 2016, Medley’s dividend per share was $0.30, $0.30, $0.22, $0.22 and $0.22, respectively, while the net investment income was only $0.28, $0.26, $0.20, $0.23, and $0.19, respectively. And while Medley has already declared another upcoming dividend of $0.22 per share, we won’t be surprised to see the company reduce the dividend again to better align it with the net investment income, assuming that Medley’s planned $50 million in additional upcoming share buybacks won’t reduce total dividend payments enough to keep the dividend per share amount healthy relative to the net investment income per share. And importantly, even if Medley cuts the dividend (like it did last summer), we believe the market may “yawn” again (i.e. no significant price move) especially considering Medley already trades at a discounted share price relative to its book value.

Valuation and Peer Comparison

For some perspective, the following chart shows Medley’s (MCC) price-to-book-value relative to many of its BDC peers.

We like that Medley trades at approximately 80% of its book value because this suggests the market is already factoring in future risks such as a potential dividend cut and the idea that the company may experience lower returns (still high returns, just lower) than it experienced during the distressed conditions that followed the financial crisis.

Also important, Medley trades at a larger discount than many of its peers because its portfolio is perceived to be riskier (as we showed earlier, not all of its portfolio loans are senior secured first liens). However, Medley has been working to reduce its risk exposures, and it still maintains investment grade ratings. Plus Medley is still closer to its five-year price-to-book low than many of its peers.

For reference, the following table provides more information on Medley’s performance versus many of its BDC peers.

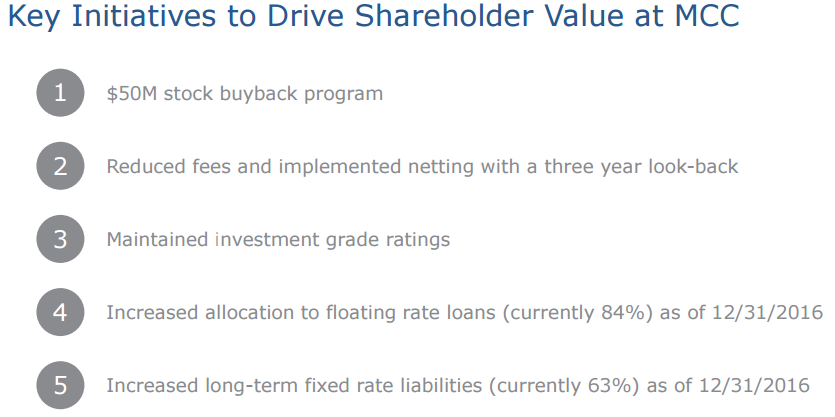

And from a summary perspective, Medley highlights the following key initiatives in its recent investor presentation as drivers of shareholder value.

Risks

Of course there are risks associated with investing in Medley. For starters, the rate of slowing net investment income we showed earlier could speed up, and Medley may be required to cut its dividend even more dramatically than it did last year. This is a risk that could have a negative impact on the company’s ability to succeed.

Another risk factor is a severe market-wide economic downturn. This seems unlikely given current market conditions, but if it did happen it would negatively impact Medley’s portfolio companies’ ability to pay their debts, which would impact Medley negatively.

Yet another risk factor would be renewed competition from big banks. As we mentioned earlier, big banks were forced to de-risk following the financial crisis, and this was a positive for BDCs like Medley as shown in the following graphic.

However, less regulations under the new administration could allow banks to begin competing with BDCs for loans. Further, new regulations could impact the viability of BDCs and registered investment companies, which could have a negative impact on Medley.

Conclusion

Medley is very likely to continue paying big dividends for many years to come. And even if the company is forced to lower its dividend again, it will likely be a moderate reduction that has little impact on the share price (just as last summer’s dividend cut had very little impact), especially considering Medley’s price is already discounted versus its book value and compared to its peers. If you are a diversified income-focused investor, we believe Medley Capital is worth considering.