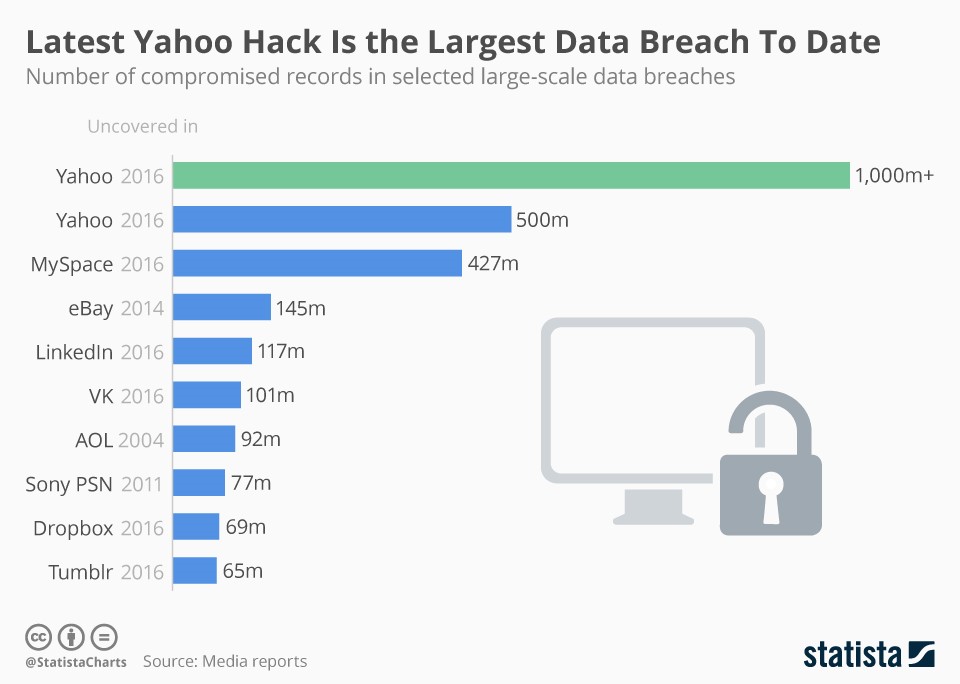

When Verizon conducts its quarterly conference call in about a week, we will perhaps learn more about its plans for acquiring Yahoo since the recent revelation that Yahoo’s data breach was dramatically more far-reaching than originally reported. As we’ve written before, Verizon needs Yahoo, and that need continues to grow despite the data breach. Specifically, Verizon needs Yahoo to fight growing challenges on two fronts...

First, Verizon must change to stay relevant (and profitable) because its traditional wireline and wireless businesses are becoming marginalized and saturated, respectively, and Yahoo (combined with the earlier AOL acquisition) will help Verizon evolve into the profitable and growing online advertising space that the company is strategically pursuing out of necessity.

And second, Yahoo will help Verizon keep the cash flow spigots open so as to constantly feed the big, safe, growing, dividend payments that Verizon shareholders demand.

Verizon’s Evolution:

“In periods of rapid change, the most important question a corporate leader can ask is, are we the company we need to be for the future?”

That was the question posed by Verizon’s CEO, Lowell McAdam, in his most recent annual letter to shareholders. And while Verizon is making significant efforts to be the company it needs to be, it’s doing so out of dire necessity. For example, Verizon has become a leader in building out the nation’s best wireless network because it was clear that wireless would marginalize its traditional wireline revenues.

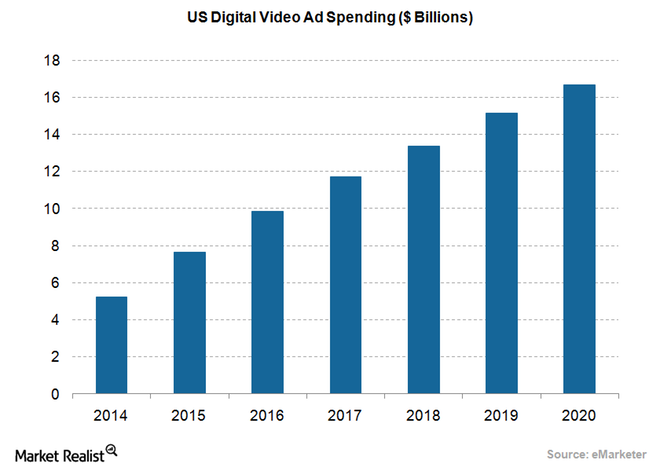

And now as wireless becomes increasingly saturated, Verizon is looking to digital media and advertising to stay competitive. Specifically, Verizon paid $4.4 billion in 2015 for AOL, and has proposed $4.8 billion for the acquisition of Yahoo, both of which will expand Verizon’s efforts in digital media and advertising, a space which is expected to continue growing rapidly as shown in the following chart.

However, Verizon’s pursuit of growth in this area is not because it is a bold innovator (Facebook and Google already dominate mobile advertising), Verizon is pursuing growth in this area out of dire necessity, particularly with regards to feeding it’s big dividend (4.4%) that shareholders absolutely demand.

Verizon’s Big Dividend:

Without question, many dividend investors love Verizon’s big steady dividend which has now been increased for ten consecutive years. But to put things in some perspective, the following chart shows Verizon’s recent dividend payout ratio as a percent of free cash flows

And as the above chart shows, the payout ratio has continued to climb dramatically in recent years. In our view, the climbing payout ratio makes CEO Lowell McAdam’s statement about being “the company we need to be for the future” particularly dire. Specifically, the industry is changing rapidly, and if Verizon cannot adapt (e.g. it’s trying to harness the growing online advertising market) then it will become very challenging to keep supporting the big dividend.

By way of comparison, the following chart shows the free cash flow dividend payout ratio for AT&T, Verizon’s peer and also a big dividend payer at 4.8%.

And as this chart shows, back in 2014, AT&T faced the same challenge Verizon currently faces in terms of a precipitous dividend payout ratio. However, AT&T was able to address the issue by acquiring DirectTV (mainly for its cash flow qualities, but also for longer-term strategic reasons), and that subsequently helped improve AT&T’s dividend payout ratio (i.e. the deal was structured in a way that used a combination of debt and equity, instead of cash, so as to improve the aggregate dividend payout ratio to a more manageable level).

In Verizon’s case, the strategic Yahoo acquisition (and the earlier AOL acquisition) are designed to do largely the same thing (i.e. improve cash flow in the short-term, and provide longer-term strategic growth opportunities). For example, Yahoo doesn’t pay a dividend, and neither did AOL, but both businesses generate plenty of free cash flow that helps Verizon meet it cash flow needs in the short-run, but also help with Verizon with its longer-term evolution strategy.

Worth noting, Verizon also helped support its big dividend payments in 2016 by selling some of its telecom properties to Frontier Communications for $3.3 billion in cash and $5.2 billion in Frontier stock (the cash helps support Verizon’s dividend, and the Frontier stock isn’t horrible either considering the large amount of government subsidies it receives via the “Connecting America Fund”). Additionally, Verizon raised over $5 billion in cash in 2016 by selling tower assets to American Tower Corp.

Valuation:

Using a discounted free cash flow model, Verizon’s current stock price is reasonable with some upside potential depending on growth. For example, we can back into Verizon’s current market price (~$52 per share) if we assume an average long-term growth rate of 1.9%, which is not unreasonable considering the 29 analysts surveyed on Yahoo finance expect the 5-year growth rate to be 1.68%. Additionally, given the company’s low beta and long-term stability, and the attractiveness of its big dividend to income-focused investors, we believe Verizon’s price is unlikely to decline dramatically.

Also worth considering, Verizon’s forward price-to-earnings ratio is not unreasonable versus it recent history as shown in the following chart. For example, it’s certainly cheaper than it was this time last year when investors were almost insatiably bidding up the price of “safe haven” dividend stocks.

Risks:

Verizon faces a variety of risks worth considering. For starters, the company is stuck in the challenging position of trying to be both a growth company and a value company. It’s a value company in the sense that it’s a mature and extremely cost conscious, and it pays a big dividend. However, it’s a growth company in the sense that it is forced to search for new growth opportunities (such as digital marketing) as its traditional communications industry continues to evolve. Balancing these two aspects of the business creates challenges (for example, Verizon is not able to pursue growth as aggressively as other companies that do not spend large amounts of cash on dividends), however Verizon has been able to navigate the space and find a successful niche thus far, and provide the stable dividend growth that its investors want.

Another risk for shareholders is that Verizon’s volatility and dividend policies may change over time. For example, as Verizon pursues more growth opportunities, its volatility may increase. Additionally, Verizon may have less cash available to maintain the current pace of dividend increases as it is forced to spend on new opportunities. For example, we’ve already seen how Verizon’s dividend payout ratio is being stretched (see previous chart above).

Other risks include the intense competition in the communications and digital marketing industries, the constant threat of new regulations, and the risks of meeting its long-term legacy pension liabilities given the persistent possibility of market volatility and declines.

Conclusion:

Despite the risks, we consider Verizon an attractive investment for income-focused investors. In fact, we’ve ranked Verizon #9 on our list of top 10 Big Dividends Worth Considering because of its valuation and because we believe it will be successful in generating the cash flows it needs to support the big, growing, dividend payments. Ideally, we’d like to see Verizon add to its cash flows via strategic initiatives (such as digital marketing revenues through a successful Yahoo integration). However, the company also has the ability to keep raising cash by selling off assets, if need be (i.e. Verizon does have the best wireless network in the US). Overall, if you are a long-term, income-focused investor, we believe Verizon is worth considering for an allocation within your diversified investment portfolio.