This diversified energy co ($50B mkt cap) announced strong Q3 earnings Tues am (non-GAAP EPS of $6.46 beat by $1.43). Shares up 4% this am. The co generated $3.1B in op cash flow and returned $1.2B through dividends and share repurchases (div yield is 3.7%). Trading at 4.7x EV-to-EBITDA (fwd), the co is special b/c as it continues to expand midstream, it deserves a higher valuation multiple due to the steadier nature of that largely-fee-based business. During Q3, the co increased its economic interest in DCP Midstream. Long.

Solid Energy Play: 4.3% Yield, Buybacks and Upside

If you like dividend-growth stocks, offering an attractive yield and price appreciation potential, you may want to take a hard look at this diversified energy manufacturing and logistics company. It’s coming out of its toughest year in operating history (2020, thanks to covid), but is giving strong indications there are more share price increases, share buybacks and eventually dividend hikes, once it gets the additional 2020 debt under control—which we believe it will quite soon (i.e. it’s currently turning the corner hard). In this report. we review the business, dividend safety, valuation, risks and then conclude with our opinion on investing.

In the Face of Panic: Selling Income-Generating Put Options, Phillips 66 Edition

Trying to call a bottom to the current energy and coronavirus-driven market sell off is a fool’s errand. No body knows. It could end soon or it could be long and drawn out. However, it’s okay to be a bit opportunistic during the current market sell off, so long as it is consistent with your long-term investment goals (e.g. “be greedy when others are fearful,” and “buy when there is blood in the streets.”). One such opportunistic strategy that’s become particularly attractive now, is selling out-of-the-money income-generating put options on stocks you’d like to own for the long-term. This article shares one such example, Phillips 66 (PSX).

Phillips 66: Powerful Dividend Growth, Significantly Undervalued, So What Gives?

Phillips 66 (PSX) has a diversified business model that reduces earnings volatility and delivers steady cash flows. As such, it has been able to raise its dividend every year for the last seven consecutive years. The stock offers a solid dividend yield of 3.4% along with a high probability of dividend increases and price appreciation. In this article, we dig deeper to ascertain the sustainability of dividends and also the company’s growth prospects. We review the health of the business, cash flow position, balance sheet flexibility, valuation, risks, dividend safety, and conclude with our opinion about why PSX may be worth considering if you are a long-term income-focused investor.

Top 5 High-Yield Blue Chips for Contrarians

When to Let Your Winners Run!

This chart shows the returns on the 10 stocks and 3 ETFs we purchased in our Income Equity strategy on January 8th of this year (the names are reserved for members-only). The only other trades we've done this year in the Income Equity strategy were on May 6th when we purchased 6 additional stocks which have also performed very well. This week’s Weekly provides our view on when to take profits versus when to let your winners run!

Our 28 Favorite Stocks: July Performance Review & Outlook

In this week’s Blue Harbinger Weekly, we provide a brief performance review and outlook for each of the 28 holdings across our Blue Harbinger strategies. We also provide access to a members-only report on our “Top 3 Covered Call Stocks.” Lastly, you’ll notice we’ve updated performance though the end of July, and all three Blue Harbinger strategies continue to significantly outperform.

Phillips 66: Big Dividend, Attractive Long-Term Opportunity

Phillips 66 has recently under-performed the market because investors are too focused on the short-term crack spread impacts, rather than on the long-term growth into chemicals and midstream businesses. It is also a cash generation machine with a big growing dividend. Warren Buffett recently increased his ownership to nearly 15%. It announces earnings this Friday (7/29). We own it in our Income Equity strategy.

Top 5 Donald Trump Stocks Worth Considering

This week's Blue Harbinger Weekly is a continuation of our free report titled Ten Donald Trump Stocks Worth Considering. Specifically, we provide detailed reports for each of the top five stocks. We believe each stock offers a particularly attractive dividend yield and significant price appreciation potential. Without further ado, here are the top 5 Donald Trump stocks worth considering...

Three Terrific Buying Opportunities

This week’s Blue Harbinger Weekly reviews three of our current holdings that present terrific buying opportunities right now. First, a diversified refining company that recently sold off thus creating an attractive buying opportunity. Second, a revenue-growing juggernaut that likely can’t be stopped for many years to come. And third, a smaller utility company that may soon be acquired. Log in to view all the details, and if you’re not currently a member, consider a subscription.

Are You Diversified? Appropriately?

Long-term investors should not forget the risk-reward tradeoff. For example, if you were diversified into investment-grade bonds over the last year then your account balance probably hasn’t suffered as much as if you’d invested entirely in stocks. However, over the long-term, we expect stocks to significantly outperform less-risky bonds. This week’s Weekly highlights some extremely attractive stock-specific opportunities that have been created by 2016’s recent market volatility.

Phillips 66 (PSX) - Thesis

Phillips 66 (PSX) – Thesis

Rating: BUY

Current Price: $75.20

Price Target $96.00

Thesis:

Phillips 66 (PSX) is the most diverse of the major refining companies, but you wouldn’t know it based on the way the stock trades. Specifically, the market has assigned PSX a valuation similar to other refiners, and the stock trades in lock step. However, the company’s chemicals and midstream businesses warrant a different valuation multiple, and the stock price shouldn’t be quite as highly correlated with other refiners. We believe PSX offers a decreasingly volatile but growing earnings stream and deserves a higher stock price based on its attractive free cash flows that are used to profitably grow the business and reward shareholders with stock buybacks and increasing dividends.

Phillips 66 Overview and Outlook:

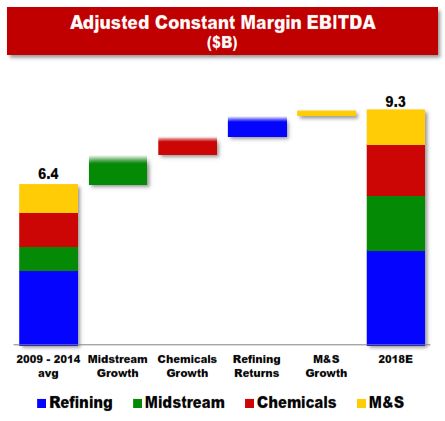

The following table from the company’s latest Investor Update shows the earnings (before interest, taxes, depreciation and amortization) of Phillips 66 over the last five years as well as the company’s expectations for 2018.

Fast growing midstream and chemicals businesses will generate a significant portion of EBITDA growth, but refining and marketing & sales will also contribute. Refining and marketing & sales are the main business activities of most refining companies, but Phillip’s 66 is unique in the large (and growing) portion of earnings from other businesses (i.e. midstream and chemicals).

Valuation:

This next table shows the typical EV/EBITDA valuation multiple assigned to the various business activities in which PSX is involved (EV is enterprise value, and it’s basically a summation of a company’s total debt and equity value with some minor adjustments). The PSX valuation is higher than its refining peers, but the market is still not giving the company enough credit for the size and growth potential of its chemicals and midstream businesses. Midstream businesses receive a significantly higher multiple due largely to the very stable earnings they generate from long term fee agreements.

If PSX were to receive full credit for its various business segments then its stock would trade significantly higher (around $93 per share) based on its current business mix as high as $100 per share based on its expected 2018 business mix. However, even without this business mix multiple expansion, the stock has significant upside from the large expected EBITDA growth between now and 2018. And unlike its refiner peers, this growth will be generated largely by midstream and chemicals (as well as some growth contributions from refining and marketing & sales). For added perspective, if PSX achieves its expectation of around $2.3 billion of midstream EBITDA in 2018 then the midstream business is worth around $34 billion as a stand-alone company (we used a 14.5x multiple), not far below what the entire company is worth now.

PSX will spend heavily to generate the midstream and chemicals growth, but the company generates more than enough cash to fund the growth and to also reward shareholders with share buybacks and increasing dividends. The following charts show the mix of capital spending as well as the breakdown of cash returned to shareholders.

Conclusion:

PSX is offers an attractive dividend yield and significant capital appreciation opportunity. And if PSX meets its growth expectations and generates $9.3 billion of EBITDA in 2018 then the company is worth significantly more than its current stock price suggests. Further, the stock has even more upside if the market starts giving it credit for its midstream and chemicals businesses instead of just lumping it in with other large (less diversified) refiners.