There are a lot of people that demand “big yield” from their investment portfolios. And they demand it, pursue it and define it, in widely different ways. In this report, I review 5 different big-yield portfolio strategies (ranging from 10%+ yields, monthly-pay strategies, and dividends versus distributions) for investors with $2 million in investable assets (or thereabouts), as well as a handful of risks and mistakes to avoid. I conclude with my strong opinion on which strategy is best.

What is “big yield” and why is it desirable?

To some people, a dividend yield over 3.5% is considered “big” (as long as it is steady and growing). To others, a yield must be over 10% or it’s not even worth considering. This juxtaposition also raises the critical distinction between a dividend yield (i.e. the income an investor receives solely from dividends as a percentage of a stock's price) and a distribution yield (which can include dividends, capital gains and sometimes a return of your own capital, frequently used in closed-end funds, for example).

Also, people desire big yields for widely different reasons. For example, some people need steady income to pay the bills, whereas others simply reinvest the dividends because it gives them added comfort and security that their investments are healthy and safe. Or said differently, they don’t want to chase after volatile high-growth stocks, many of which have never even turned a profit.

1. Schwab US Dividend Equity ETF (SCHD)

The Schwab US Dividend Equity ETF (SCHD) is a beautiful strategy that keeps steadily increasing its dividend each year by investing in “high dividend yielding stocks issued by U.S. companies that have a record of consistently paying dividends, selected for fundamental strength relative to their peers, based on financial ratios.”

SCHD is revered by many for its dividend growth, relatively-lower volatility (as compared to the total US stock market) and low expense ratio (recently only 0.06%).

SCHD continues to deliver exactly what many investors want and need, and it’s no surprise that its assets under management (i.e. fund size) has continued to grow so dramatically over the years. SCHD has made a lot of money for a lot of people, while also allowing them to sleep well at night.

2. PIMCO Dynamic Income Opps (PDO)

When you think about “big yield” some investors scoff at SCHD because the yield is simply way too low for them (they also sometimes scoff because the returns have trailed the S&P 500, more on this later). On the other hand, the double-digit distribution yield offered by PIMCO’s Dynamic Income Opportunities fund (PDO) is dramatically more attractive.

PDO offers at 10.9% distribution yield, paid monthly, by investing in a mix fixed income securities (e.g. bonds) from across a variety of market sectors.

Important to note however, PDO’s yield is a distribution (not a dividend) and it has historically included dividends, interest, capital gains and even sometimes a return of capital. To some investors this is completely okay (as long as it keeps delivering those big monthly distribution payments), but to others it is unattractive because it sacrifices long-term price appreciation, gains and compound growth in exchange for big current income.

But again, if it is simply big monthly income you want, PDO is attractive, especially relative to other big-yield PIMCO funds right now. You can read my report on PDO here.

3. Vanguard 2040 Target Date Fund (VFORX)

While PDO is mostly bonds, and SCHD is stocks, some investors take a dramatically different view of income through a balanced investment strategy (stocks and bonds) that focuses on optimizing low volatility with steady growth and high income through a combination of dividends, interest and long-term price appreciation.

For example, here is a look at the asset allocation mix of a popular Vanguard target date fund, which includes US and international stocks and bonds.

This strategy focuses on total returns (i.e. dividends and interest plus price appreciation), and many investors argue it’s an exceptional way to generate around a 4% yield during your retirement years, without ever running out of money (and your actual distribution payment amount increases each year to keep up with inflation). Noteworthy, the fund yields only around 2.6% and it is expected part of the income it produces is achieved by selling a little bit of your holdings each year (although important to note you should be selling less than your average long-term gains on the strategy).

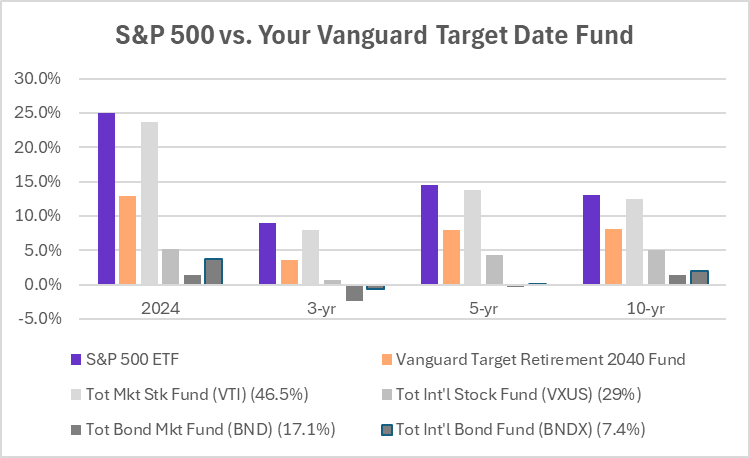

However, as you can see in the earlier chart above, the return on this Vanguard Target Date strategy has dramatically underperformed a simple S&P 500 ETF (i.e. a low-cost way to simply invest in the ~500 largest US stocks, which are diversified across sectors).

4. S&P 500 Index Fund (VOO) (SPY)

Keeping with our theme of “distribution” yield (instead of “dividend” yield) and a focus on total return (instead of simply yield), some investors argue you should just buy a low-cost S&P 500 index fund, and generate whatever spending cash you need by selling some of your winners.

For example, if the fund averages over 12% total return each year (which it has over the last decade), and you sell 10% (for income each year) then you have a 10% distribution yield, and your nest egg keeps growing (by 2%) over time.

Obviously, the problem with the above strategy is that in some years the market (e.g. the S&P 500) is down big, and if you sell some of your holdings when the market is down then you’ll miss out of the subsequently rebound and gains. Said differently, investing purely in the S&P 500 when you need your investments to produce steady income is a very risky strategy that could actually blow up in your face.

For instance, you could have been forced to sell a significant portion of your nest egg (for income) during the depths of the covid crash, the great financial crises or right after the tech bubble burst—yuck!

On the other hand, if you truly are a long-term investor, and you don’t need the immediate cash, then a 100% stock market portfolio (e.g. no bonds) may be worth considering (depending on your situation and personal tolerance for volatility).

5. Building a Custom Big-Yield Strategy

Finally, you may also consider a custom big-yield strategy, whereby you invest in a combination of things (such as a mix of SCHD, PDO, VOO and whatever additional specific stocks and/or bonds meet your needs).

You can develop a custom strategy to achieve the gains you want through a personalized mix of yield and price appreciation that adheres to your own personal time horizon, volatility tolerance and need for current income. You can even add in specific stocks you like (for example, have you been eying a few specific AI stocks? deep value stocks? or other?).

The great thing about a custom big-yield strategy is it’s all about you and your personal situation, goals and needs.

Things to Avoid (Unnecessary Risks)

There are a few important things you may want to avoid when building your big-yield portfolio. For example:

Excessive Fees: If you are going to invest in big-yield funds, watch out for high fees. Excessive expenses and fees simply detract from your bottom line. For example, at 0.06% annual expense ratio, SCHD is very good, but at 0.03% VOO is even better. And at 6.6% PDO is downright frightening to some people (in PDO’s defense, the high expense ratio largely comes from the interest expense on borrowing—interest rates have been on the rise and PDO uses over 35% leverage/ borrowed money). Some people wouldn’t touch PDO with a 10-foot pole because of this, whereas others don’t mind as long as that big steady monthly income keeps rolling in).

Excessive Leverage: At 35% leverage, PDO’s borrowing is a risk, but considering the bonds it invests in are typically safer and less volatile than stocks, in aggregate, PDO’s leverage is reasonable for the strategy). However, be aware that leverage can increase income and returns in the good times, but increase losses in the bad times.

Yield Chasing: A lot of times, individual stocks or funds that offer high yields are really just strategies in distress. For example, as price falls, yield mathematically increases (all else equal). So sometime, when a stock offers a big yield its really just a business that is in decline, possibly heading towards bankruptcy. Similarly, when a fund offers a really big yield, a lot of times it’s an indication that it is just really risky (either it owns risky stocks and bonds or it is using too much leverage that could blow up in your face). Yield chasing is a little like picking up nickels in front of a steam roller. Arguably (and empirically), SCHD gives up a little long-term returns in exchange for higher current yield (it’s not a huge difference, but it is significant, and it is worth keeping on your radar).

Insurance Products: If you have built a $2 million dollar nest egg, you may experience a lot of financial salespeople trying to sell you a lot of financial products. For example, insurance companies can structure a lot of products (such as annuities and long-term care insurance) that sound really appealing, but in actuality are just really expensive. For instance, if you have over $2 million in assets you might skip a long-term care insurance product and just “self insure” instead. It’s often dramatically more cost-efficient and effective.

Undiversified Strategies: Watch out for overly concentrated big-yield strategies too. For example, if you put all your money in real estate investment trusts (REITs) because they pay big income, you are probably exposing yourself to way too much concentration risk (for example, a lot of people did this 10 years ago thinking REITs were safe big-dividends, but they have dramatically underperformed the market as interest rates and the real estate market have undergone dramatic changes). Stay prudently diversified.

Wasting Time: Time is an extremely valuable asset, and if you are wasting it stressing over your investments or simply researching things that don’t add a lot of value anyway, it might be time to consider a new strategy. Perhaps you don’t need to own quite so many individual stocks (ETFs can work well for part of your money) and maybe you just need to hire someone to manage your investments (or at least review them) so you have more free time and can sleep better at night. Time is a terrible thing to waste.

The Bottom Line:

Big yield can be a beautiful thing, when you do it right. You’ve worked hard to build that nest egg, now make it work for you. But please, don’t let anyone pressure you into a strategy that is not right for you. There seems an endless supply of investment strategies and experts that think they know what is right for you.

Just know that prudently-diversified, goal-focused, big-yield investing continues to be a winning strategy. And the best strategy is the one that is right for you based on your own individual situation.