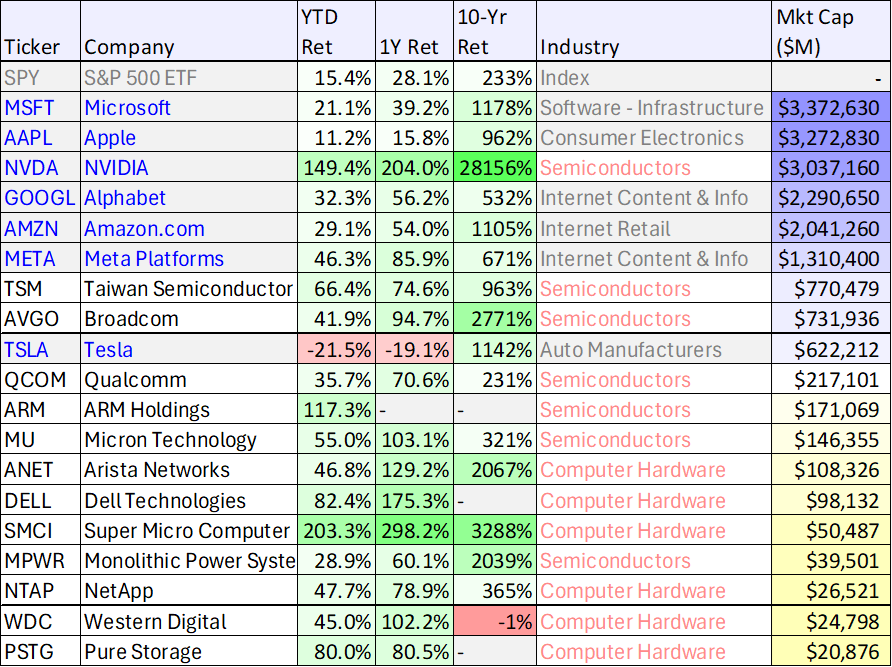

Owning top businesses for the long-term doesn’t mean turning a blind eye to the risks and rewards of market rotation. While Main Street is just now hearing about Nvidia for the first time (it’s up nearly 3,000% over the last 5-years), most investors know chip stocks (like Nvidia) are notoriously cyclical and (despite powerful long-term megatrends, like AI) 50% pullbacks are not uncommon. In this report, we countdown our top 10 growth stocks (July edition) with a special focus on market cycle risks and outstanding opportunities with big long-term upside.

Market Rotation:

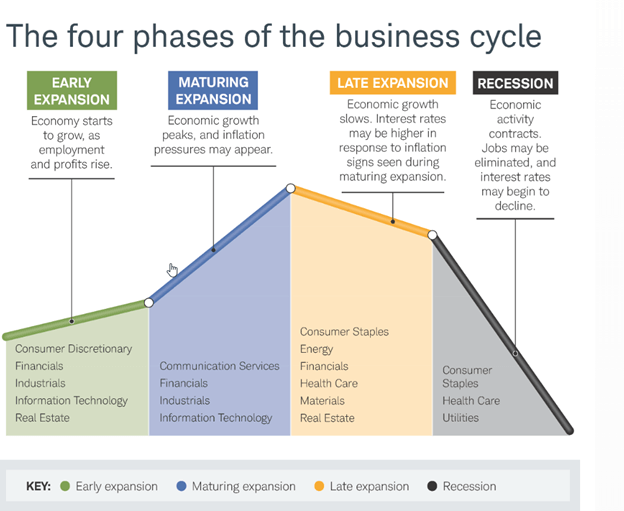

In theory, it’s pretty easy to draw a market cycle (for example, see the illustration below), but in reality it’s not realistic to perfectly time the top and/or bottom (that’s a bit of a fool’s errand, actually).

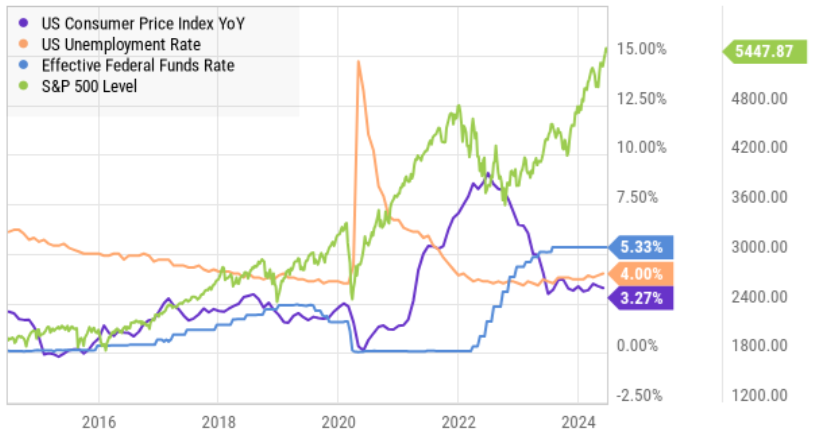

Based on current macroeconomic conditions, we’ve arguably entered a “late expansion” stage as higher interest rates (in response to inflation challenges and lower unemployement) may cause a new set of market leaders to increasingly emerge (i.e. a “changing of the guards” of sorts, whereby recent market leaders pass the torch to a new batch of opportunities).

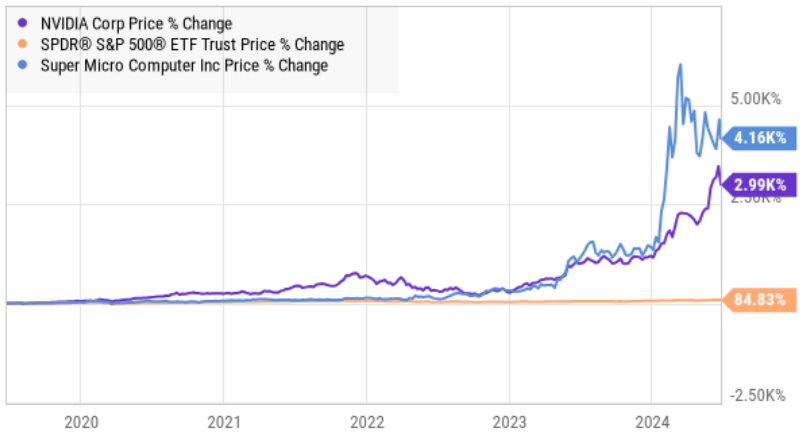

Of course there are individual businesses that are so powerful (disruptors and megatrend beneficiaries) they can succeed in almost any market environment. But that doesn’t mean you shouldn’t at least consider lightening up on some of them (such as Nvidia and/or Super Micro Computer, after their incredible recent price rallies courtesy of the cloud and AI megatrends, see chart below).

For a little perspective, famous value investor, Seth Klarman, once said:

“The stock market is the story of cycles and of the human behavior that is responsible for overreactions in both directions.”

*Honorable Mention: Nvidia (NVDA):

Before getting into the official top 10, we’re including Nvidia as an “honorable mention” on this list. As you likely already know, Nvidia makes computer chips (semiconductors) that are powering two long-term mega trends. One, the great cloud migration (Nvidia chips are used in the datacenters behind the cloud) and two is artificial intelligence (AI requires massive computational power, and Nvidia chips are the leading solution).

And considering the massive long-term growth potential for Nvidia, it might sound ridiculous to suggest selling even one share. However, just know that chips stocks are notoriously cycical, and Nvidia has a history of pulling back dramatically more than the S&P 500, as you can see in the following chart (i.e. Nvidia shares have sold off more than 50% four times since 2000, and it can happen again).

Nvidia is a critically important part of the global economy, but if your position in the stock has grown dramatically over the last few years (as the share price has climbed), it might be a good time to consider rebalancing your portfolio to bring Nvidia’s weight back down to a level you are comfortable with.

For example, there a lot of computer chip and hardware companies (see table above) that have peformed extremely well over the last year (courtesy of AI and the cloud), and if they’ve grown to very large positions in your investment portfolio (for example, over the last year, we’ve owned Nvidia, Super Micro, Monolithic Power and Pure Storage), you might want to consider a little rebalancing (when they fall, they fall hard), depending on your personal goals and investment situation.

Here are a few tips we wrote on position sizing and tax strategies (for Nvidia, in particular) if you’re considering a little rebalancing.

Top 10 Growth Stocks

So with that backdrop in mind, let’s get into the official top 10 ranking and countdown. We currently own all 10 names on the list (in varying weights, more on this later), and we have attempted to include an attractive mix of two types of top growth stocks…

Blue Chip Growth Stocks: benefiting from powerful megatrends, and currently trading at attractive prices (relative to their long-term value).

Disruptive Growth Stocks: with massive (albeit volatile) upside potential.

We start with #10 and count down to our very top ideas.

10. Aspen Aerogels (ASPN)

The world is changing, and whether you like them or not—electric vehicles are a global megatrend. And even though Aspen Aerogels does NOT make electric vehicles, this materials company (founded in 2001) is achieving new growth in recent years from its aerogel insulation products used in lithium-ion batteries in electric vehicles.

The company continues to win deals with major automakers and expects more through the end of the year. it’s also highly rated (“strong buy”) by the 10 Wall Street analysts covering this $1.8 billion small cap stock (see rating in table below).

We previously wrote this one up in detail here, and if you are looking for attractive long-term growth from a company in the materials sector, Aspen Aerogels is worth considering. We’ve owned shares for just over 6 months now (in our Blue Harbinger Disciplined Growth Portfolio), and look forward to more gains ahead.

(Data as of Tues, July 2nd. source: StockRover)

9. Mercado Libre (MELI)

Mercado Libre is the leading Latin American online commerce platform, and it offers some attractive undervalued long-term growth potential. With revenue growing well over 20% per year, and the shares trading at only 1.1x forward PEG, Wall Street has a “strong buy” rating, and we think there is room for significant long-term growth as the market opportunity is large and Meli is the clear leader.

Mercado Libre’s ecosystem of solutions includes its commerce marketplace plus payments/lending (Mercado Pago/Credito), shipping (Mercado Envios) and ads (Merado Ads). The company continues to grow its user base initially with low-cost (subsidized) shipping and membership rewards (“MELI+”), as well as an easy-to-use listing platform for sellers.

In a highly-competitive marketplace Meli has a huge competitive advantage (“moat”) due to its first mover advantage and growing economies of scale (not to mention its powerful self-reinforcing ecosystem). This already very profitable business is attractive, especially as margins continue to improve. Lots of room for continuing long-term growth (5-year EPS growth estimate is over 40% per year). We own shares in our BH Disciplined Growth portfolio.

8. Enovix (ENVX)

As smart phone energy demands grow (especially with the proliferation of AI apps), Enovix is working to scale its disruptive battery architecture to improve efficiency and capacity. And the company’s total addressable market (“TAM”) is enormous, expanding beyond just smart phones and into wide-ranging Internet of Things (“IoT”) devices and electric vehicles.

To be clear, Enovix is not yet profitable, and the risks are significant, but if it can keep moving towards scale, the upside is enormous. Wall Street rates it a “strong buy,” and we’re including it here in our top 10 list as a very attractive, albeit risky, long-term growth opportunity.

If you have room in your long-term growth portfolio for a higher-risk opportunity, Enovix has massive upside potential, and the shares are worth considering. You can read our new full report on Enovix here.

7. Microsoft (MSFT)

Simply put, Microsoft is an amazing business. Thanks to Microsoft Windows, Microsoft Office and Microsoft Azure (cloud), the company has extremely high margins (wide moat) and it continues to spend heavily on innovation and growth opportunities (a good thing, especially as Azure continues to make up ground on the number one cloud service provider, Amazon Web Services).

And despite recent price gains, Microsoft still trades at a reasonable 2.3x forward PEG multiple and 34.5x forward PE ratio. One of only two publicly-traded stocks with a “AAA” credit rating (not even the US government is rated this high), Microsoft will likely be trading much higher in the years and decades ahead. We are very long Microsoft, and you can read our previous full reports and writeups on the company here.

The Top 6

The remainder of this report is reserved for members only, and it can be accessed here. The top 6 includes an attractive mix of powerful blue chip and disruptive high growers, and we currently own all of them.

The Bottom Line

There are many attractive growth opportunities in the market today, and they’re not all named Nvidia. If the explosive outsized growth in GPUs was phase one of the new AI revolution, we could see impressive outsized growth in phase two from companies using those chips (e.g. Microsoft just bought a ton of Nvidia GPUs). And of course attractive growth exists in other industries too (such as the names on this list).

However, if you are a growth investor, you need to construct a growth portfolio that is right for you, based on your own individual situation and needs. Disciplined, goal-focused, long-term investing continues to be a winning strategy.