In this report, we rank our top 20 dividend stocks. The rankings include a split between opportunities with very big yields (yields of 7.0% and up) and very attractive total returns (i.e. solid dividend payments plus significant price appreciation potential). We also highlight 7 dividend market themes that are critically important in the current environment (including: (1) BDCs > Banks, (2) Midstream Stocks > MLPs, (3) A Bird in Hand > Two in the Bush, (4) Falling Rates > Rising Rates, (5) Bond CEFs > Bonds, (6) Contrarian Income > Herd Income, and (7) Value vs Growth). Without further ado, let’s get into the themes and the rankings (starting with #20 and counting down to our top ideas).

BDCs > Banks

Our first dividend theme is that in the current market environment, Business Development Companies (“BDCs”) are “greater than” banks. BDCs and banks are similar because they both generally borrow money at lower rates and then lend it out at higher rates. For example, at a traditional bank, you add your money to a savings account, the bank pays you a small amount of interest, and then the bank loans out your money to someone else and demands a higher rate of interest on that loan. This is called the “net interest margin” and it is how traditional banks make money.

Similarly, BDCs borrow money at a lower rate (based on the strength of their balance sheets) and then turn around and lend it out (BDCs generally lend to “middle market” sized companies) at a higher rate. BDCs were created by an act of Congress (in the 1980s) to encourage more lending to smaller businesses, and as such, BDCs generally don’t pay corporate income tax as long as they pay out most of their net income as dividends to investors (this is why BDCs generally offer such large yields). Further, BDCs often make loans to businesses that may be considered too small, too risky or too unique for traditional banks to work with (especially considering regulatory differences).

Based on the current market environment, an argument can be made that “BDCs are greater than banks” because banks are subject to increasingly restrictive capital reserve requirements (especially following the 2008-2009 financial crisis) and are under close watch by regulators following the latest string of bank failures. On the other hand, the regulatory borrowing limit for BDCs was increased just a few years back (they’re now allowed to leverage their balance sheets up to 2x).

Of course, there are a lot more differences between banks and BDCs (and they both come in a wide variety of shapes and sizes). But based on current market conditions, we’re seeing select attractive opportunities in the big-yield BDC space, such as the one described below.

20. Ares Capital Management (ARCC), Yield: 10.4%

Coming in at #20 on our list is big-yield BDC, Ares Capital. As a quick reminder, our rankings include big-yield opportunities (such as Ares Capital) and attractive total return opportunities (i.e. solid dividends, plus significant price appreciation potential). We include both, intermittently, in the countdown.

Regarding ARCC, it is the largest publicly-traded BDC in the US. It has a large well-diversified portfolio of investments (mainly loans to businesses in need) across market sectors. It also has an investment grade credit rating and a well run business. We’ve previously written about ARCC in great detail here.

Ares announced quarterly earnings at the end of April, and the results were solid. In particular, we were concerned as interest rates rise (and the economy heads towards recession) that too many of Ares loans would start going bad. However, Ares reassured its loan portfolio is in good shape and it has plenty of capital to weather the storm. We own several BDCs in our Blue Harbinger portfolios (because of the industry’s attractiveness), but Ares standouts (we own shares of Ares) for its financial strength and industry leadership position.

Midstream Stocks > MLPs

Another big-yield theme we’re seeing in recent years is that an increasing number of Master Limited Partnerships (“MLPs”) are converting to more traditional C-Corp structures, and they are sticking investors with some very large tax bills in the process. For example, Kinder Morgan (KMI) did it in 2014, and just recently Magellan Midstream (MMP) and Oneok (OKE) announced a deal.

And despite some extremely attractive big-yield opportunities in the MLP space (such as Enterprise Products Partners (EPD) and Energy Transfer (ET), which both have loads of steady fee-based revenue to support their compelling large distributions), we’re choosing to invest in midstream companies outside of the MLP structure (because we don’t like the headaches of receiving a K-1 at tax time, and because many investors are simply not allowed to own MLPS in their tax-advantaged Individual Retirement Accounts (“IRAs”), depending on their broker).

19. Phillips 66 (PSX), Yield: 4.4%

Known mainly as a refiner, Phillips 66 has grown its midstream business and deserves a higher valuation multiple (midstream businesses generally trade at higher multiples due to their steadier long-term fee based income). It also has a solid dividend (which was just recently increased by 8% to $1.05 per quarter) and the company also just repurchased another $800 million in shares (attractive).

To put the strong performance into perspective, PSX recently announced non-GAAP EPS of $4.21 thereby beating expectations by $0.65. And the earnings beat was due to much bigger than expected refining earnings (strong market conditions) and from higher midstream and marketing earnings.

In a nutshell, PSX is a great business. It is very profitable, positioned to benefit from higher crude prices going forward, plus benefits significantly from its increased midstream business. And at only 5.4x forward EV/EBITDA these shares are attractive for long-term investors seeking growing dividends and share price appreciation. You can read our past PSX reports here.

A Bird in the Hand > 2 In the Bush

Switching back to investment themes, there is an old saying that “a bird in the hand is better than two in the bush,” and this applies to dividend investing too. The meaning is basically that it’s better to be content with what you have rather than risking everything (and losing) in search of something better. With regard to income investing, many greatly prefer to receive big steady dividend payments now, instead of “rolling the dice” on more volatile growth stocks (or on companies that pay lumpy, uncertain, less-frequent dividends). More specifically, many investors believe (prefer):

Current Yield > Yield on Cost

Monthly Dividends > Annual Dividends

Dividend Income > Price Gains

Growing Income > Falling Income

For example, we really like (and own shares) of big-distribution (6%+ yield) closed-end fund Adams Diversified Equity (ADX), but it didn’t make it onto this top 20 list because it pays three smaller quarterly distributions, followed by a larger distribution in the fourth quarter, and many income-focused investors cannot stand this lumpy cadence (even though the fund has consistently been paying distributions for over 80 years!).

Similarly, some investors really like big dividend mortgage REITs (such as Annaly Capital (NLY) and AGNC Investment Corp (AGNC)) because they offer large dividend yields, often over 10%. However, no mortgage REITs made our top 20 list because the business models tend to be highly sensitive to the market cycle (particularly interest rates), and they often reset their dividends to a lower level (something a lot of investors just can’t stand!).

18. PIMCO Corporate and Income (PTY), Yield: 11.4%

Regarding “a bird in hand is better than two in the bush” we are including this big-distribution bond fund (PTY) in our top 20 because of its massive distributions, which have been paid without interruption since the fund’s inception over 20 years ago. And not only are the distributions steady, but PTY also occasionally pays additional special dividends too. Further, this fund pays distributions monthly (instead of quarterly or annually) another characteristic a lot of investors really appreciate.

Further still, this fund may be priced significantly more attractively than usual considering it trades at a smaller premium to NAV than it has in recent history (premiums are often par for the course for PIMCO funds—the leader in the industry). Plus, it seems interest rake hikes by the fed may finally be over (bond funds have been hurt badly by the recent rapid rate hikes because as rates rise, bond prices fall). We’ll have more to say about fed rate hikes later in this report, but we like PTY and we own shares. And we would have ranked it even better on this list if it weren’t for other opportunities (including other PIMCO bond funds) that we find even more attractive. If you are looking for big steady income, PTY is absolutely worth considering.

17. Schwab US Dividend Equity ETF (SCHD), Yield: 3.7%

Whether it is due to great marketing by Schwab or pure strong demand by investors, the Schwab US Dividend Equity ETF is extremely popular, especially considering recent market volatility and this fund’s track record of strong performance.

For some background, SCHD is a passive ETF benchmarked to the Dow Jones U.S. Dividend 100 Index. That means Schwab isn’t actively selecting any stocks for the fund, instead they’re passively buying all the stocks in the underlying benchmark through a full replication technique. That (combined with economies of scale) is how they keep the SCHD expense ratio fairly low (it’s recently 0.06% annually). Here is a link explaining how the Dow Jones U.S. Dividend 100 Index (and ultimately SCHD) actually works (see page 19), but in a nutshell it’s basically using a thoughtful formula to select high-dividend stocks.

If you are curious, to be included in SCHD, a stock has to be in the Dow Jones US Broad Market Index—excluding REITs (this index has around 2400 constituents-excluding REITs), it tilts towards stocks that have a strong history of dividend growth, it has to meet minimum market cap and trading volume requirements (this eliminates mainly micro-cap stocks), and then it includes the 100 top-ranked stocks (that score well according to free cash flow, return on equity, yield, and 5-year dividend growth rate) according to dividend yield.

There are more nuances in terms of weightings and rebalancing (as you can read about in the link provided above). And it may sound complex, but SCHD is basically just selecting stocks with relatively higher-dividend yields and subject to the financial metric requirements defined in the index methodology.

We wrote in more detail about SCHD here, but if you are simply looking for low-cost passive exposure to dividend growth stocks, SCHD is more than decent enough to be included in our top 20 list.

Falling Rates > Rising Rates

At this point, we’ve all felt the impacts of rapidly changing interest rates. For example, the economy benefited from near-zero interest rates during the pandemic. However, the chickens have come home to roost, and we’re all now feeling the pain of high inflation (that is the direct result of pandemic stimulus).

Similarly, many investors that complained (rightfully) about the 0.0% interest they were receiving in their savings accounts, are now experiencing small victories as savings rates have gone up, certificates of deposits (“CDs”) are now actually worth considering (many offering yields in the 4.0% to 5.0%) range, and short-term treasuries are even better (the 6-month rate is over 5.0%, although longer-term treasuries yield less and this “inverted yield curve” is often a sign of an ugly looming recession).

Further still, growth stocks soared “to the moon” when interest rates were at zero, but then crashed very hard as the fed started aggressively hiking. And of course as rates go up, bond prices fall. Bond investors have felt historic levels of pain as rates have risen quickly (and bond prices fell hard). And with some characteristics similar to bonds, preferred stocks have also fallen hard.

16. iShares Preferred Stock ETF (PFF), Yield: 6.9%

Although referred to as preferred “stocks,” they’re really a lot more like “bonds” in the sense that they typically have a stated face (or par) value (usually $25 per share) and they have a contractual interest rate. However, unlike bonds, preferred stocks typically don’t have a set maturity date, and with regards to the capital structure, preferred stocks rank junior to all other bonds (which means in a bankruptcy situation—the bond holders may get some of their money back, whereas the preferred stock holders often get nothing). Further, like bonds, when interest rates rise, preferred stock values fall (and vice versa), and when market volatility (i.e. fear) rises—preferred stock values also typically fall.

Further, every preferred stocks has its own unique details in terms of interest rates, possible (but not mandatory) redemption dates and more. One good resource to look up the details on an individual preferred stock is quantum online.

According to BlackRock (i.e. the company behind iShares), the iShares Preferred and Income Securities ETF seeks to track the investment results of an index composed of U.S. dollar-denominated preferred and hybrid securities. It gives investors exposure to U.S. preferred stocks, which have characteristics of bonds (pay a fixed dividend) and stocks (represent ownership in a company). It gives investors access to the domestic preferred stock market in a single fund, and it can be used to pursue income that can be competitive with high yield bonds.

Since inception, PFF has done what it was designed to do, and its total returns have kept pace with its index. And it may be particularly right now as interest rate hikes may finally be over (as rate rise, preferred stock prices fall). And if rates actually fall through the end of 2023 (as some experts are predicting as recession looms) “lookout above” for preferred stocks and PFF.

Overall, preferred stocks can be an attractive big-yield asset class, depending on your goals. They tend NOT to provide as much total return as common stocks over the long-term, but they do generally provide more income and less short-term price volatility. For these reasons, many investors choose to passively invest some of their portfolio in ETF PFF (i.e. they want exposure to the preferred stock asset class for income and for diversification purposes). You can read our previous PFF report here.

Bond CEFs > Bonds

As mentioned, as rates rise, bond prices fall. And that is exactly what happened as the fed aggressively raised rates following unprecedented pandemic stimulus. And as hard as bond prices fell, some extremely-popular bond CEFs (closed-end funds) fell even harder because they use leverage (borrowed money) to magnify income in the good times (which also magnified the pain in the bad times as rates were rising).

However, there are reasons to believe bond CEFs are now more attractive than simply investing in bonds. For starters, many market analysts and experts are now predicting the fed’s interest rate hikes are finally over (and CME fed fund futures are even predicting multiple rate cuts before the end of 2023 perhaps to offset the impacts of looming recession). And if this is true that means bond prices will finally stop falling (all else equal), and may even start to rise (if rates are reduced).

This environment bodes well for bond CEFs because if rates stabilize then levered bond CEFs are left with higher income-generating power than simply owning bonds (because the bond CEF leverage will magnify the income). Further, if rates fall, then bond CEFs will be dually helped by rising prices (as rates fall, prices go up, and levered bond CEFs own more bonds per dollar than unlevered investments). And on top of these benefits, many popular bond CEF prices have fallen faster than their Net Asset Values (“NAVs”) as frightened investors shunned them thereby creating even more attractive entry prices, relatively speaking. Also worth mentioning, bond CEFs are generally limited to 50% leverage (a prudent limit in our view considering the relative volatility of the asset class).

15. BlackRock Multi-Sector Income (BIT), Yield: 10.3%

Simply put, we like (and own) this big-yield bond fund for a variety of reasons. For starters, the distribution yield is large, it has been consistent since inception in 2013, and the fund has also occasionally paid additional special dividends. Further, BIT currently trades at a small discount to NAV, it is managed by world-class manager BlackRock (they have loads of resources and “economy of scale” advantage) and it uses a prudent amount of leverage (recently ~34.6%). Finally, it has some conservative interest rate exposure (duration was recently 2.5 years) so if rates fall, this fund has some attractive upside (and that is in addition to its big steady monthly distribution payments to investors).

Contrarian Income > Popular Income

Mark Twain once said:

“Whenever you find yourself on the side of the majority, it is time to pause and reflect.”

That seems like it could have been pretty sound advice for all the growth stock investors that piled into aggressive growth stocks (right before the pandemic bubble burst), and for all the income-hungry investors that piled into popular big-yield PIMCO bond CEFs at huge price premiums (right before bond prices crashed and those premium prices largely evaporated thereby increasing the pain).

Similarly, many contrarian investors like to purchase attractive businesses when they are out of favor with the market. And regarding contrarian income, we share a couple highly compelling opportunities below.

14. Celanese Corp (CE), Yield: 2.6%

Celanese is materials company, and it is hated by the market (because of the ongoing lagged effects of pandemic disruption—more on this in a moment).

For some background, Celanese manufactures performance engineered polymers and it is also the world's largest producer of acetic acid (and its chemical derivatives). Celanese materials are used in a wide variety of products such as automobiles, medical applications, consumer electronics and many more. The company currently offers 63 different products

Like much of the rest of the world, Celanese’s business was disrupted by the pandemic (specifically by supply chain disruptions and manufacturing shutdowns, both in the US and abroad). The shares are down nearly 40% over the last year. Celanese is a value stock.

We view Celanese as an attractive contrarian value stock because it has cost advantages over peers (due to its scale and because it has access to low cost feedstocks courtesy of its Clear Lake Texas operations and low cost US natural gas), and because we are near a low point in the market cycle (hopefully!) that was caused by pandemic disruption.

Trading at 9x earnings, with a net margin of 17.2%, and having grown its dividend to investors for 13 consecutive years, we view Celanese as an attractive contrarian opportunity with significant share price appreciation potential as pandemic supply chain disruptions resolve and Celanese emerges as the low cost leader with increasing economy-of-scale advantages.

We wrote about Celanese in more detail here, and if you are looking for an attractively priced contrarian opportunity that also pays a big growing dividend, Celanese is worth considering.

13. British American Tobacco (BIT), Yield: 7.5%

If ever there was a company (or industry) that should pay a big dividend, it is British American Tobacco (and the tobacco industry, in general). BTI is very profitable, but doesn’t have a ton of long-term growth (because the industry is viewed very negatively by many consumers and government regulators). Nonetheless, BTI has very high profit margins, high cash flows, a very well covered dividend, and a very wide moat (that gives it competitive advantages). Further, we view BTI as particularly compelling right now from a valuation standpoint (i.e. the shares have significant upside from multiple expansion—i.e. the P/E should be higher).

If you are looking for a steady big-dividend grower, that also has share price appreciation potential, British American Tobacco is absolutely worth considering. We currently own shares in our High Income NOW Portfolio and you can read our recent full report on BTI here.

Value Stocks vs. Growth Stocks

A controversial topic is the constant “value versus growth” debate. It’s controversial because investors can become extremely loyal to one style versus the other, and because some investors simply don’t care about broad market styles (they prefer instead to focus only on attractive individual investment opportunities).

As mentioned in the previous section, a lot of growth stocks got absolutely annihilated when the fed started raising rates and the pandemic bubble finally burst. And as much as those stocks are hated right now, some of them are very healthy businesses trading at dramatically more attractive prices than previously. We shared multiple attractive contrarian value stock opportunities in the previous section (above), and now we share an extremely attractive “contrarian growth stock” opportunity below (we’d feel remiss if we didn’t at least acknowledge such opportunities in the current market environment.

12. SoFi Technologies (SOFI)

To be clear, SoFi is different from other opportunities on this list because it does NOT pay a dividend and because the share price is extremely volatile. If you are looking for steadiness and income—do not invest in SoFi. But if you are looking for powerful (albeit volatile) long-term growth, these shares are worth considering.

SoFi is an online financial services company and bank that targets younger high-income customers. It generates the majority of its revenues from loan origination, and it has recently faced heavy fear and selling pressure. Specifically, a Supreme Court decision (regarding student loan forgiveness and forbearnace) is expected in the next few weeks, and it could significantly affect the business and the share price.

In addition to legal challenges, fear regarding recent bank failures have kept the price artificially low in our view (the shares trade at only 2.9 times sales) despite continuing rapid revenue growth.

Rising interest rates have been a significant driver of revenue growth recently as the shares head toward GAAP profitability this year. And if sentiment changes (like we believe it should) these shares can rise significantly in the short run, and over the long-term the upside is even bigger as the total addressable market opportunity is quite large. SoFi is down sharply over the last year (and well below its all-time highs—during the pandemic), but the long-term upside potential remains enormous from here. You can read our previous SoFi report here.

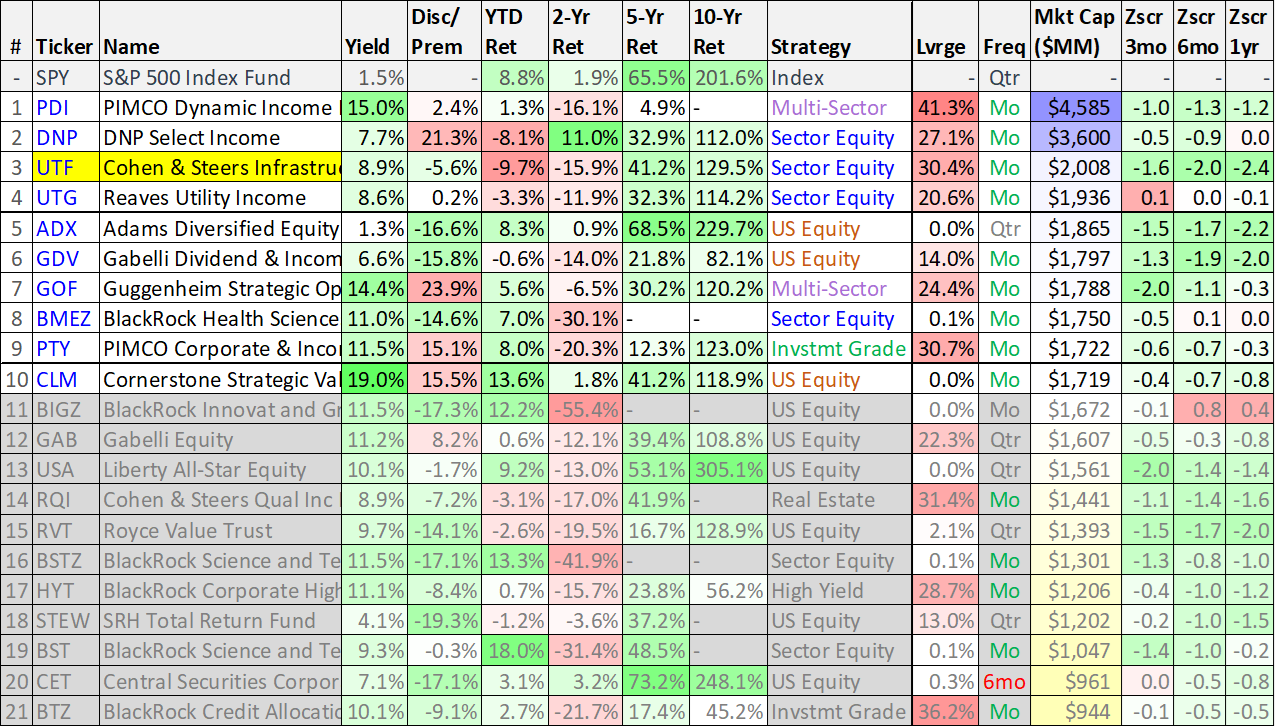

*Honorable Mention: Guggenheim Strategic Opportunities Fund (GOF), Yield: 13.9%

The Guggenheim Strategic Opportunities fund is revered by many income investors thanks to its big 13.9% distribution yield (paid monthly) which has never been reduced since inception in 2007. But before you go investing in this impressive high yielder (which recently held 94% of its assets in fixed income securities, and utilized 24% leverage), first consider its premium. Specifically, GOF currently trades at an extremely high premium (+27.5%) as compared to the net asset value of its underlying holdings. Further, not only is this premium very large, but it is large by GOF’s own historical standards. Of course there is no guarantee that this premium will ever get bigger or smaller, however it is a risk factor investors should consider.

11. Cohen & Steers Infrastructure (UTF), Yield: 8.2%

The Cohen & Steers Infrastructure Fund is another popular CEF, and unlike GOF, UTF currently trades at an attractive discount to its NAV (recently -5.2%). Both are income-focused CEFs, but they do follow different strategies. For example, UTF invests in infrastructure securities (both stocks and bonds) including utilities, pipelines, toll roads, airports, railroads, marine ports, telecoms and other infrastructure companies. UTF recently held 240 individual positions, and it uses around 30% leverage. We view UTF as an attractive contrarian opportunity (especially as compared to GOF), and it is worth considering if you are looking for a big-yield alternative (especially considering its yield seems a bit more sustainable and it currently trades at an attractively discounted price while holding a diversified portfolio of infrastructure-related securities).

The Top 10:

Our top 10 dividend ideas are reserved for members only, and they can be accessed here. The list includes an attractive mix of "High Income NOW" opportunities and dividend-growth opportunities. Members also get access to our 25+ position High Income NOW Portfolio, and 30+ position Income Equity Portfolio. For income-focused investor, the market continues to present a select variety of very attractive opportunities.

Conclusion:

If you are an income-focused investor, you have a lot to choose from, including high current yields versus powerful total returns (i.e. solid dividend payments plus significant price appreciation potential), plus the seven themes we have described in this report. And in particular, we believe the 20+ oppotunities we have highlighted in this report are exceptionally attractive and worth considering. However, at the end of the day, you need to invest only in opportunities that are right for you based on your own individual situation. Disciplined, goal-focused, long-term investing continues to be a winning strategy.