If you like steady dividend income and the potential for healthy share price appreciation, REITs are worth considering. Especially this year as share prices are down and dividend yields have mathematically risen. However, not all REITs are created equally. In this report, we share data on over 100 REITs, sorted by industry (and including a brief commentary and outlook for several important REIT industries), and then countdown our top ten REIT ideas (starting with #10 and finishing with our top idea).

A Note on REIT Industries:

Importantly, the various REIT industries in the tables throughout this article are very different (as we will explain below) and the specific REITs within each industry can also be extremely different. With that backdrop in mind, lets get into some REIT industry details and our top 10 countdown.

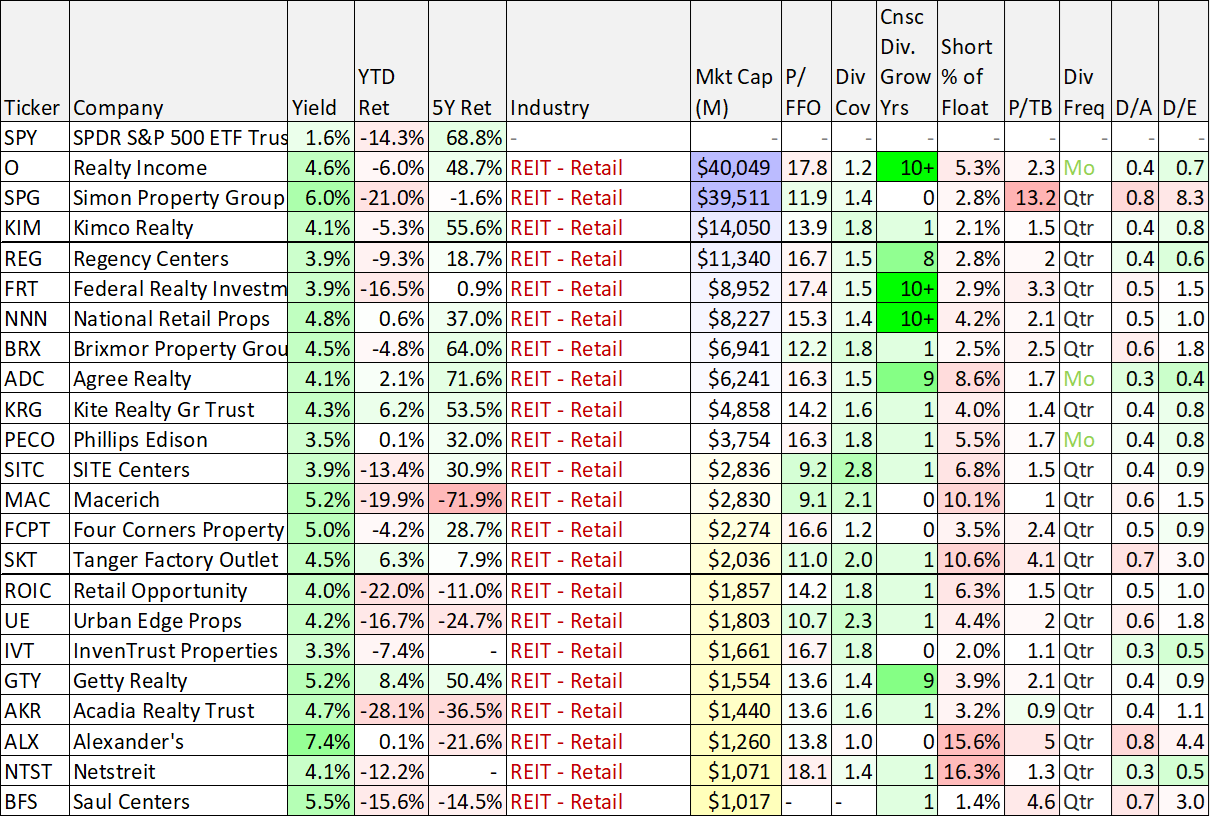

Retail REITs

As you can see in the table above, most retail REITs have been ugly this year, and the past few years haven’t been much better. The very high-level oversimplified explanation for the weak performance is that online shopping is destroying demand for retail properties, as you might infer from the chart below.

And while there is some truth to the “death-of-brick-and-mortar-real-estate” narrative, not all retail real estate is actually dying. In fact, A-class retail properties will continue to grow over time as the old adage “location, location, location” matters just as much now as it ever has. As we will explain below, our expectation is that poorly-located retail real estate is entering a “death spiral,” but select prime location properties will continue to grow over time (and keep paying big growing dividends).

10. Simon Property Group (SPG), Yield: 6.0%

Coming in at #10 on our list, Simon Property Group is the largest retail mall REIT (shopping malls and premium outlets) in the US. It is focused mainly on A-class properties (more than 80% of operating income), whereas B-class constitutes ~15% of NOI and C-class (and below) less than 1.0%. Without doubt, the ongoing growth of online shopping is disrupting the retail industry, but it is our view that A-class properties will not only survive, but also thrive, whereas C-class and lower will become largely extinct over the next decade.

We recently wrote up Simon in detail for our members, but the basic thesis is that despite the market’s hatred for retail REITs, Simon has a very strong “investment grade” balance sheet, an extremely well-covered dividend (that will likely keep growing as the payout ratio is still overly conservative following the pandemic, see table above), a compelling low valuation multiple (forward P/AFFO is below 11x), and its properties at located in highly sought after locations (based on foot traffic and the need for prime retail locations for companies to market to their omni-channel customers). If you are looking for an attractive long-term contrarian opportunity, Simon Property Group is worth considering.

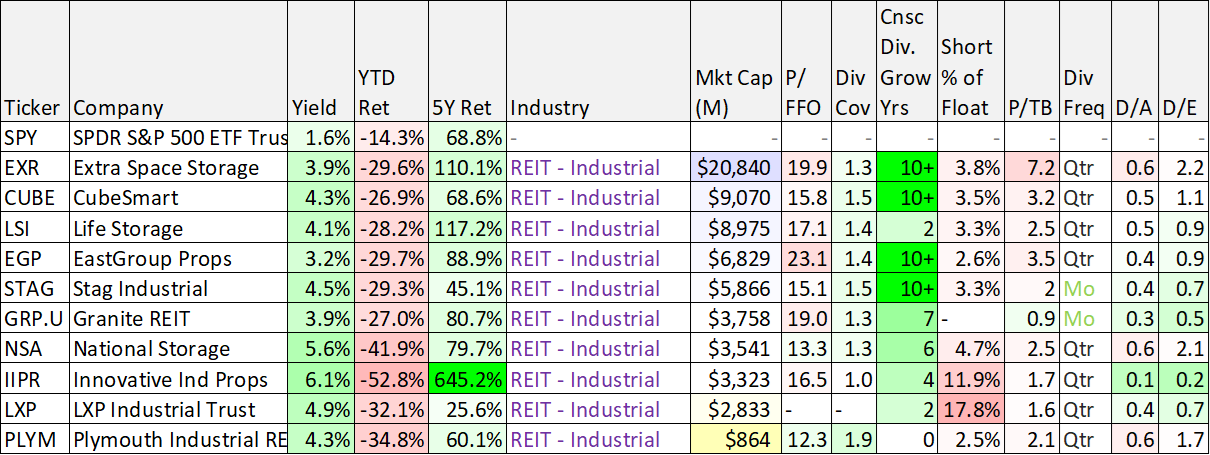

Industrial REITs

In our view, industrial REITs have particularly attractive long-term prospects because they are supported by economic growth, both online and brick-and-mortar. Industrial REITs experienced strong gains as supply chains adjusted to the pandemic disruptions, but have since sold off hard (thereby making for some very attractive opportunities). Further, industrial property rents continue to grow while vacancies fall (both good things for industrial REITs).

Industrial Real Estate: Warehouse/Distribution (W/D). Source: Colliers

As you can see in our table below, industrial REITs tend to have some of the lowest dividend yields among REITs, but one of the reasons for that is because they also have some of the best long-term growth prospects.

9. EastGroup Properties (EGP), Yield: 3.2%

Sticking with our “location, location, location” theme (it matters just as much now as it ever has), EastGroup properties owns industrial properties in prime distribution hub locations across the Southern sunbelt US states. Like other industrial REITs, EGP shares have sold off hard this year, but it will benefit from continuing long-term demand and economic growth (considering its highly valued strategic supply chain hub locations). And it currently trades at only 23 times FFO, low by its own historical standards. We also like EGP because it has a lower market cap that industrial REIT leader, Prologis (PLD) for example, which will make it easier to move the growth needle going forward. If you are looking to buy an attractive industrial REIT at a lower price and attractive valuation, EastGroup Properties is worth considering. We have owned the shares in the past, and may add them back again soon.

Office REITs:

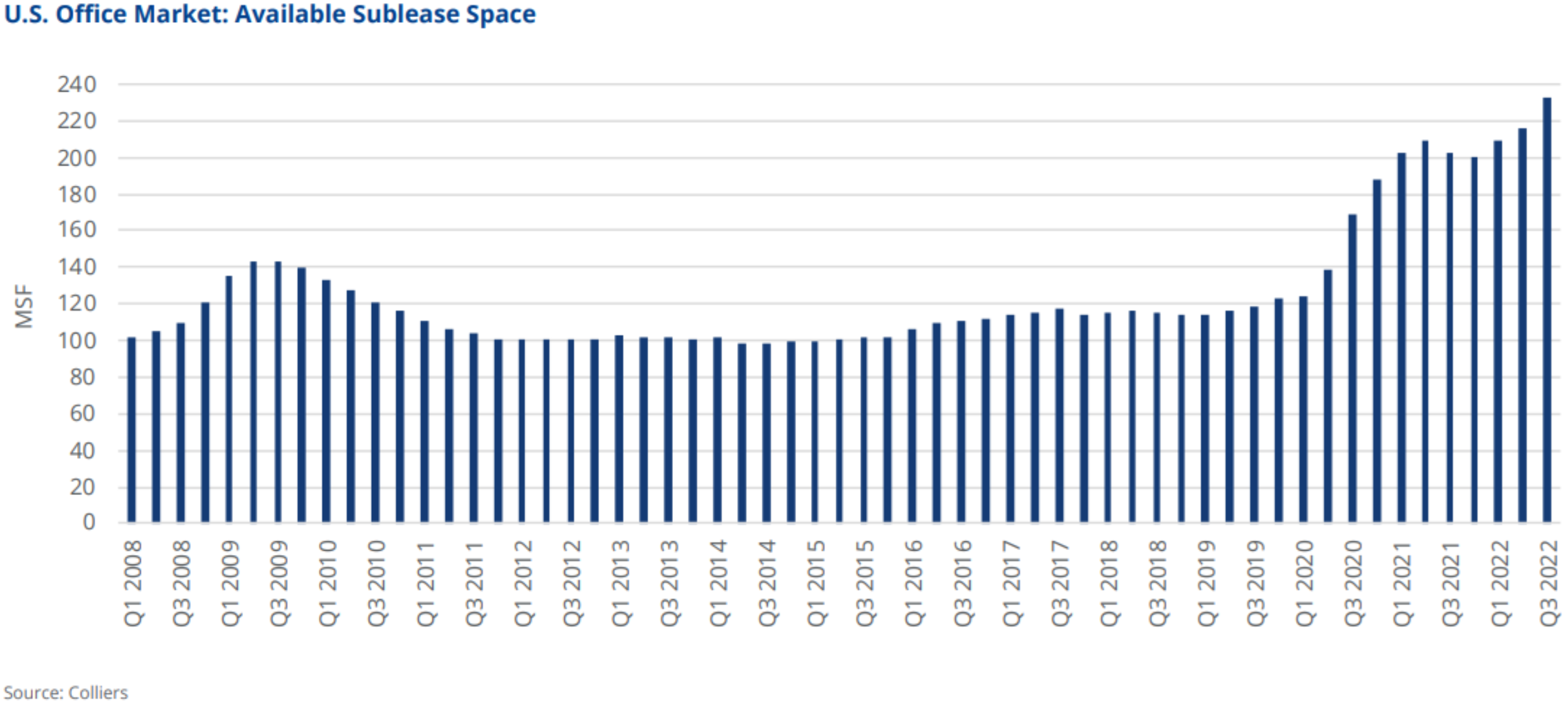

In perhaps an unexpected twist, many of the most sought after office property locations have experienced sharp declines in demand as pandemic lockdowns forced people to work from home—a trend that still continues to a very significant extent. For example, here is a look at available sublease space in the US (below), and as you can see supply is high (not a good sign for the space).

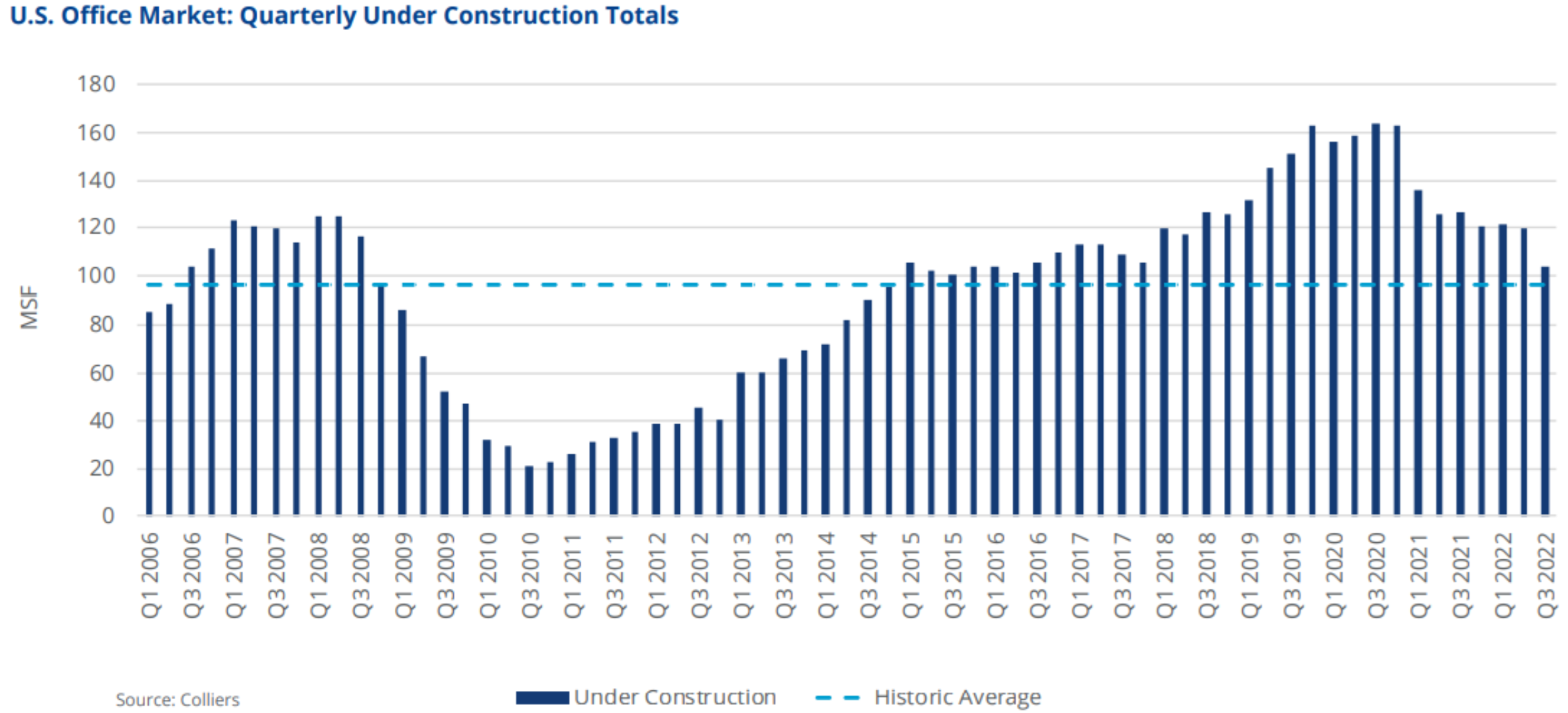

Further still, office construction is down but still high, not a good sign for supply and demand dynamics.

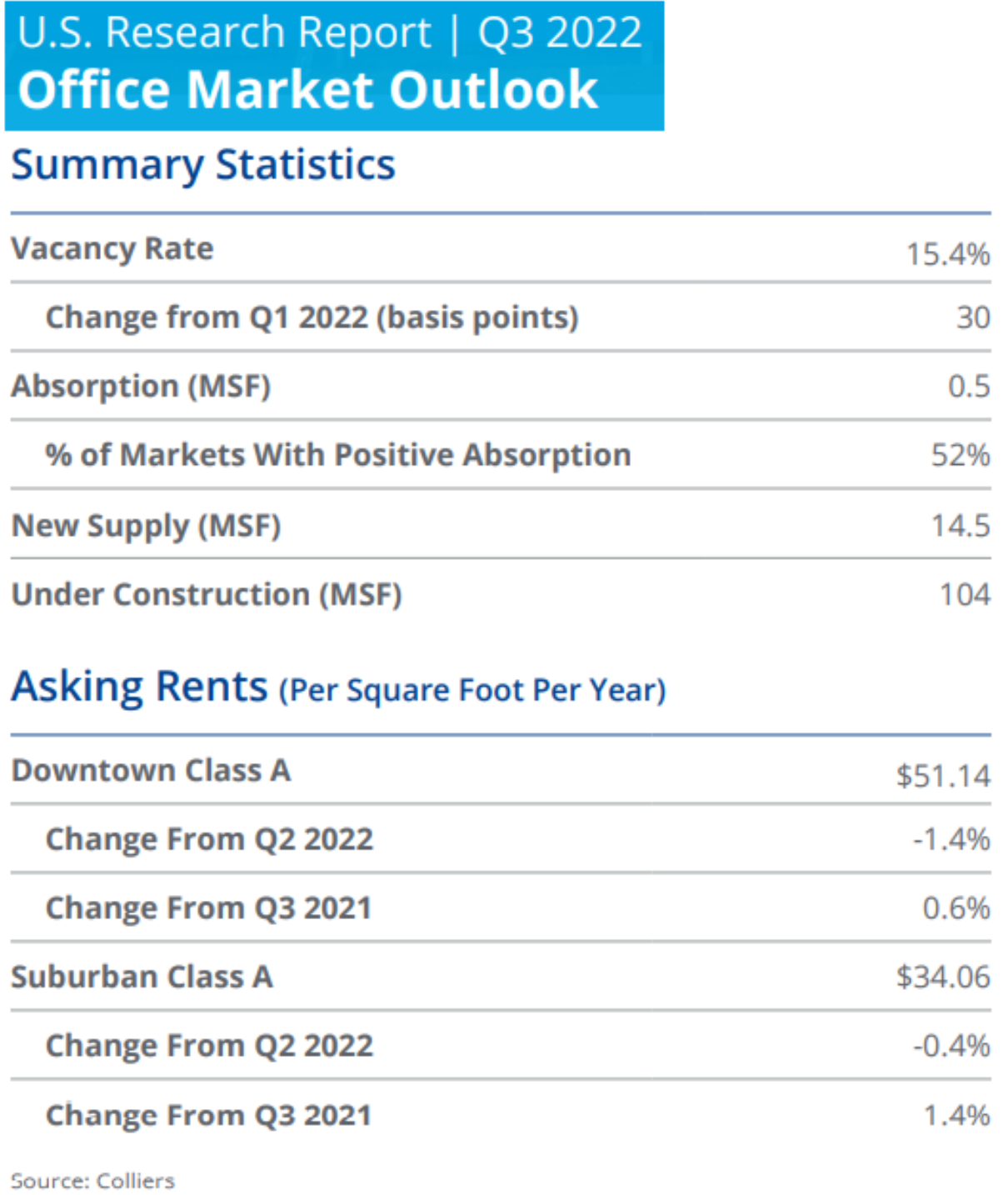

For perspective, the office vacancy rate is high across the US and rents are down (also not a good sign).

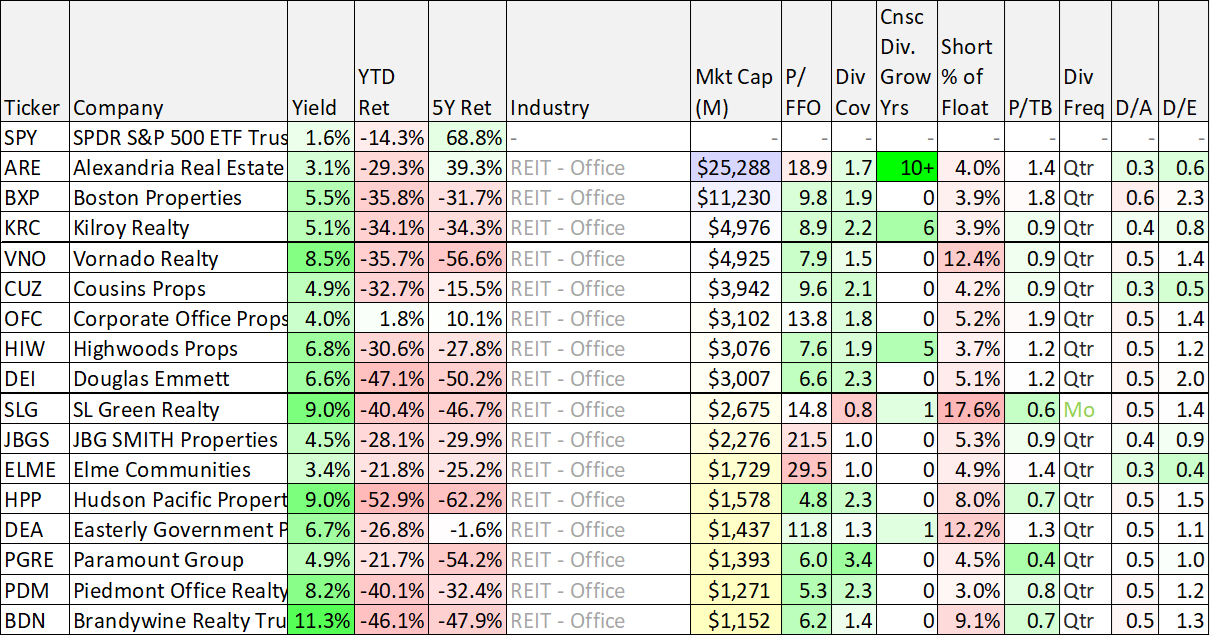

There may be plenty of attractive contrarian opportunities in the office REITs space (you can see examples of opportunities in our table below), however we have not selected any office REITs for this top 10 list.

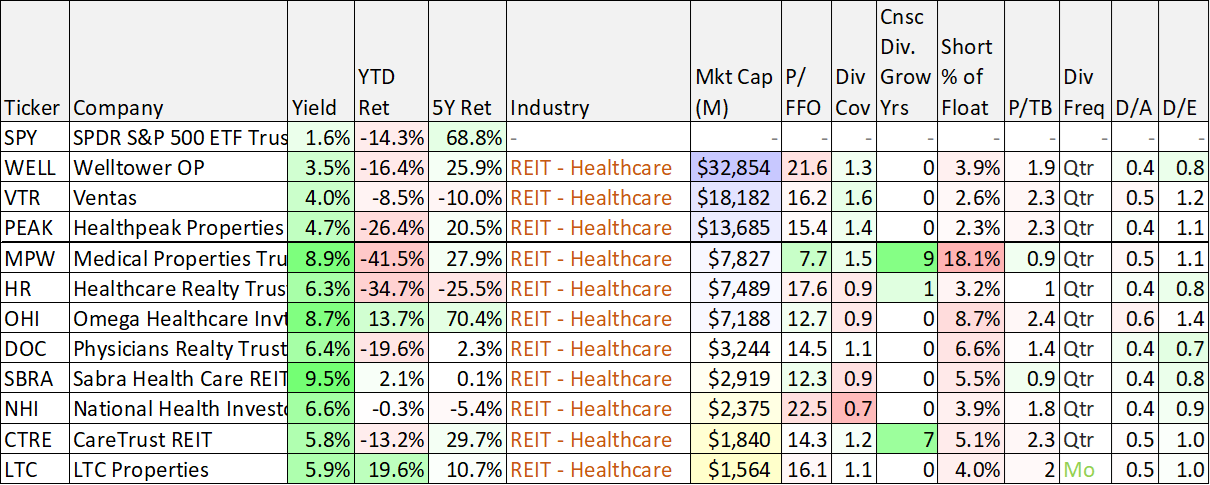

Healthcare Facility REITs

Healthcare facility REITs are widely diverse, ranging from assisted living, to hospitals, outpatient care and even private prisons. However, one thing they have in common is they were greatly disrupted by the coronavirus as many of their tenant occupants and employees were at high risk. Another thing they have in common is depressed share prices and larger than normal dividend yields.

8. Medical Properties Trust (MPW), Yield: 9.1%

Coming in at #8 on our list is a somewhat controversial pick, Medical Properties Trust. MPW has performed worse than most REITs this year (and the shares have been highly shorted), as it faces challenging headwinds from struggling hospital operators, heavy debt and rising interest rates. However, there are reasons to believe these headwinds are subsiding as fundamentals improve (for example, operators are bringing down costs, reimbursement rates are increasing and debt challenges are being worked out with Prospect and Steward) and macroeconomic headwinds may be subsiding (i.e. inflation is showing signs of slowing and the fed may slow its rate of interest rate hikes).

We recently wrote up this REIT in detail for our members, but the basic gist is that if you are a highly risk-averse investor, MPW is not right for you. But if you can handle the volatility, the shares are worth considering for a spot in your prudently-diversified long-term income-focused portfolio (especially considering the very low P/AFFO ratio and the very large dividend yield).

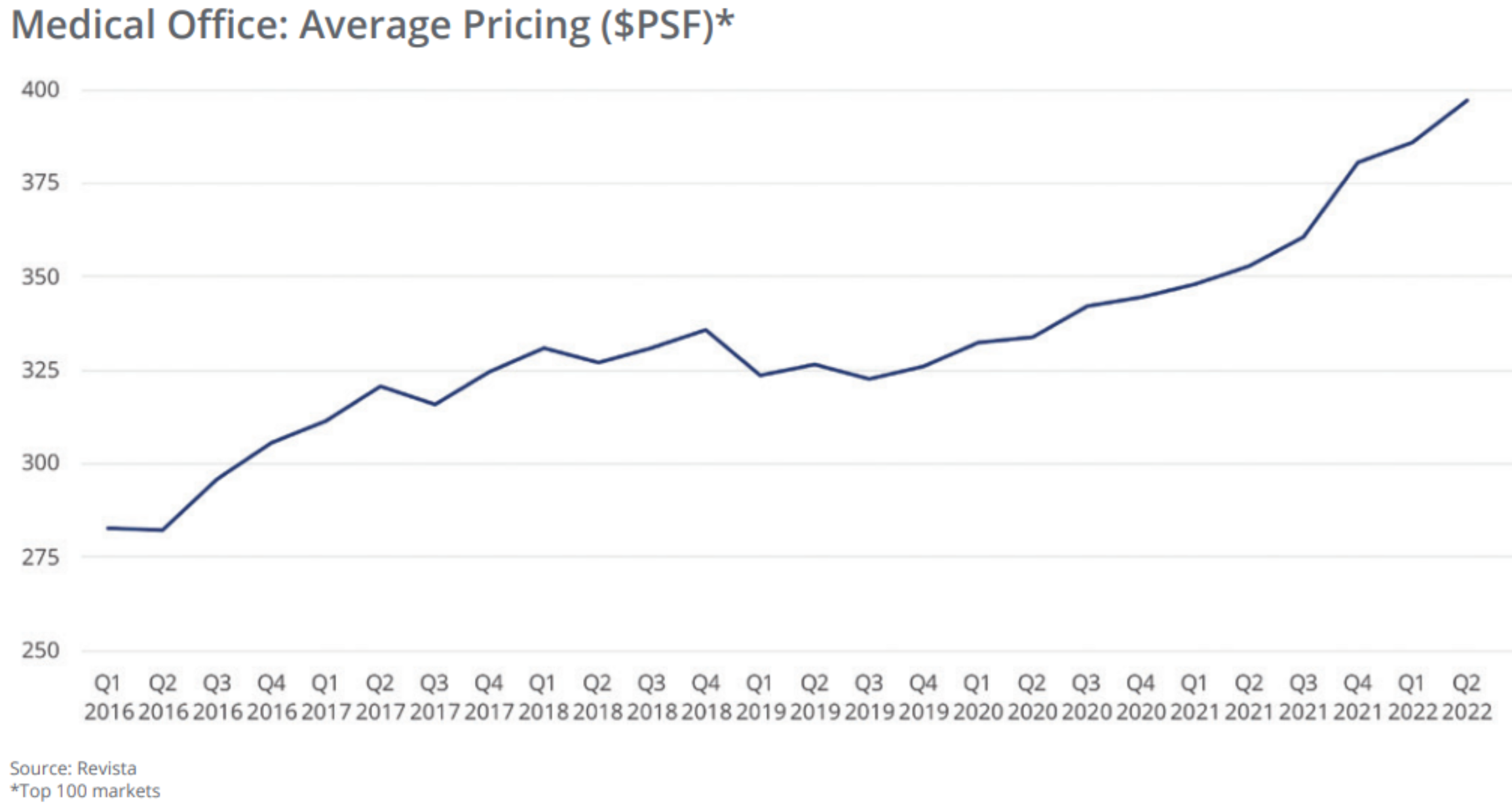

Medical Office Buildings:

Another interesting sub-industry within healthcare REITs is medical office buildings. This group is somewhat less sensitive to current macroeconomic headwinds, as described by Colliers in their Q2 U.S. Healthcare Services Report:

“While no property sector will be immune to the impact of high inflation, a slowing economy and rising operating costs, the MOB sector is well placed to weather the storm. Underlying business fundamentals for medical tenants are stronger than a typical office user, which reduces concern over future income streams. There is greater stability in demand for medical services and, potentially, pent up demand from procedures canceled or postponed during the pandemic. In addition, U.S. Census data estimates that one in five Americans will be 65 or older by 2030, rising to one in four by 2060, thereby under-pinning demand for medical office facilities.”

And to put that in perspective, here is a look at the healthy pricing trend for Medical offices (from the same Colliers report).

*Honorable Mention:

*Physicians Realty Trust (DOC), Yield: 6.4%

Physicians Realty Trust isn’t the fastest growing REIT, and it has far less dramatic upside price appreciation potential than recently troubled (but improving) industry peer Medical Properties Trust (as we described earlier), but DOC does have much more stability and financial health.

If you don’t know, Physicians Realty Trust owns healthcare properties that are leased to physicians (as well as hospitals and healthcare delivery systems). DOC also offers a well covered dividend, a reasonable valuation, less debt and is in a much stronger financial position than many of its industry peers. If you are looking for a steady dividend yield (along with some price appreciation potential), Physicians Realty Trust is worth considering.

Specialty REITs: Data Centers

The specialty REIT industry is diverse, but one interesting subset of the group is data centers. Data centers basically house servers to support data that is “in the cloud.” And considering the massive secular trend by enterprises around the globe to digitize everything and then migrate it to the cloud for better access, data center REITs (such as Digital Realty (DLR), Equinix (EQIX) and now even Iron Mountain (IRM) to some extent) stand to benefit.

Like the entire real estate sector, most data center REITs have sold off hard this year. And one common negative viewpoint is that they are becoming increasingly obsolete faster than they can build out (or acquire) properties to meet demand. For example, according to Morningstar analyst, Matthew Dolgin, who has a “buy rating” on data center REIT, Digital Realty:

“Virtualization and other technological advances could allow Digital's tenants to do more with less space and fewer connections, reducing their data center needs.”

7. Digital Realty Trust (DLR), Yield: 4.4%

Digital Realty is a specialty REIT focused on data centers. The shares have sold off way too hard this year as it’s gotten caught up in the tech sell off (tech stocks are down more than the market averages this year). Noteworthy, DLR has low debt, a very reasonable valuation and a dividend (that has been growing every year for 10+ years) that is well covered by FFO. In our view, the selloff is overdone, and DLR currently represents an attractive value. Simply put, if you are looking for a steady big-dividend with some reasonable share price appreciation potential, Digital Realty is a blue chip REIT worth considering.

Diversified REITs

Diversified REITs are typically involved in more that one industry, such as office, retail and industrial, to name a few. The following table shares data on a variety of diversified REITs, and you probably recognize at least a few of your favorites.

6. W.P. Carey (WPC), Yield: 5.3%

When it comes to big-dividend REITs, WPC is a stalwart favorite (it has increased its dividend for over 10 years straight). More specifically, it is a diversified, large cap, net lease REIT, specializing in the acquisition of operationally critical, single-tenant properties in North America and Europe. It owns properties across a variety of market segments (e.g. Industrial (26%), warehouse (25%), office (20%) and retail (16%)). It’s also in a financial strong position, the dividend is well covered, and the yield is high by historical standards (all good things). We recently wrote up WPC in detail, and you can review that report here.

The Top 5:

Our top 5 big-dividend REITs are reserved for members-only and they can be accessed here. The top 5 focuses on the most attractive opportunities and we currently own four of them (and the fifth is high on our watchlist). In aggregate, we view the REIT space as ripe with attractive long-term investment opportunities.

Conclusion:

REIT share prices have taken a big hit this year, but many of them have maintained their big dividend payments, thereby making the sell off easier for some investors to tolerate. What’s more, many REITs are positioned to not only survive a macroeconomic slowdown, but also to thrive in the years ahead. And their dividend yields are currently larger than normal (they’ve mathematically risen as the share prices have fallen). If you are a long-term income-focused investor, now is an excellent time to own select REIT opportunities, such as those described in this report, within your prudently-diversified, long-term, income-focused investment portfolio.

Get instant access to 100% of Blue Harbinger’s member-only content:

For reference, you can view more REIT data below (sorted first by industry and then by market cap).