If you’re looking for a source of income in your portfolio, but all of the dividend growth stocks you like seem expensive, then you may want to consider selling put options. It’s a way to collect some extra income now, and if the stock price falls far enough in the future then you get to buy the shares at the lower price. This strategy is absolutely not for everyone, but for those of you inclined, this article details five specific dividend-growth stocks (Bank of America, Gilead, IBM, Verizon and Goldman Sachs) that currently offer attractive put option premiums for income-focused investors.

Our View on Using Put Options

For starters, selling put options is a way to generate extra income, and the strategy is absolutely not for everyone. It involves unique risks and requires more active involvement than simply buying and holding. If you don’t know, a put option is a contract that gives the owner the right to sell a specific number of shares, of a specific stock, at specific price, by a predetermined date. The put seller receives a premium (income) in exchange for agreeing to buy the shares if the put owner decides to execute the put. A put is like an insurance contract where the contract holder can protect him or herself against a decline in stock price. The put seller is like the insurance company that makes money by collecting premiums.

For many standard brokerage accounts, if you’re going to sell put options (your account must be approved) then you must keep cash on hand in the account to buy the shares if they are put to you. As a long-term investor, keeping cash on hand (instead of owning stocks, for example) can detract from your long-term performance because it can cause you to miss out on the long-term gains of the stock market. However, in many cases, the annualized premium for selling puts can be greater than the annual gains for the stock market (with less volatility), and the income generated from selling the puts is thereby enough to satisfy the put seller. However, the risk is that the share price may fall dramatically, and you'll be forced to buy the shares. However, if you're attracted to the shares in the first place, you'll be happy to buy the shares at a lower price than when you wrote the put.

Alternatively, if you have a margin account (your broker must approve you), then you can sell the puts without keeping any extra cash in the account. This way you can stay fully invested (in the stock market, for example), thereby not missing out on any long-term stock market gains, plus any income you generate from selling the puts is like gravy on top of your investment portfolio. If the put option is executed, and the shares are put to you, then you’d buy them on margin (i.e. using borrowed money). Using leverage is a higher risk strategy that is not for suitable for everyone. However, recall that if you have a mortgage on your house or if you ever pay with a credit card, then you are using leverage. You may considering using leverage to sell put options if you want to stay close to fully invested in the market at all times (i.e. you don’t want to miss out on any long-term market gains) and generate extra income within your investment portfolio (again, this strategy is not for everyone).

Generally, this strategy (selling puts) offers higher premiums (more income) when volatility is high, which unfortunately is not the case right now (volatility is near historical lows). However, there are still pockets of high volatility in the market (based on fear and false narratives), and that’s where we’re seeing the best opportunities to pick up extra income by selling puts. And to get a better idea of how to generate income with this strategy, we have highlighted five specific dividend growth stocks that we believe currently offer attractive premiums (income) for selling put options.

1. Bank of America (BAC). Yield: 1.3% (and growing)

The premium for selling put options on Bank of America is attractive, in our view. For example, the following table shows that by selling the July 21st puts with a strike price of $22 (5.3% below the current market price), you can generate $0.38 per contract. That comes out to roughly 10.4% on an annualized basis ((0.38/22) x (12/2) months). So if you execute this strategy every 2 months, and the shares never get put to you, then you’d have made over 10% annually (minus transaction costs).

And if the shares do get put to you, we like that too because Bank of America is attractive for a variety of reasons (such as the four described below), especially at the lower price and over the next two months.

First, the fear that the Trump rally is ending is overblown. Yes, financial stocks (big banks in particular) did experience large gains after Trump won the election, and yes the rate of gains for financials has slowed more recently, as shown in the following chart.

However, Trump is still fighting to reduce regulations to unleash growth (even though large parts of the fiduciary rule are still scheduled to go live on June 9th), and GDP did beat expectations in the first quarter and is expected to grow in Q2. And this growth is despite the relentless efforts by the main stream media to make Trump look as bad as possible. And it is actually the media’s laser focus on Trump that may be causing markets to overlook several very big (potentially very positive) things going on with the big banks, including Bank of America.

Second, the media hasn’t been saying much about the Fed’s annual Comprehensive Capital Analysis and Review (“CCAR’) which is expected by June 30th, and will announce whether big banks are allowed to increase dividends and share buybacks. Let’s not forget, the big banks have come a very long way since the financial crisis. They are now financially strong (US banks are passing stress tests), and are taking much more reasonable risks. If the CCAR allows banks to increase dividends (which would be nice for shareholders), it could easily put bank stocks on an upward trajectory.

Third, the fed is widely expected to raise interest rates again on June 14th as shown in the following CME FedWatch graph, and this also supports healthy growth for the big banks including Bank of America.

Remember, banks make money on the net interest margin (the spread between what they pay on deposits and what they charge on loans, and higher interest rates helps increase net interest margin and ultimately bank profits). When the Fed raises rates again, it will enable bank growth to continue, despite the negative media narrative.

And fourth, earnings season is approaching. Big banks will announce earnings in mid-July (just before options expiration), and positive earnings could give a positive boost to the banks. And considering big bank price gains have slowed recently, but the benefits of higher interest rates should be flowing through to bottom lines, we could see some positive earnings announcement reactions.

2. Gilead (GILD), Yield: 3.2%

Gilead is another attractive stock upon which to write puts, in our view, for the following reasons. First, market sentiment is very negative on Gilead. The share price has been steadily declining for many months now as patents will soon expire, competition is growing, and frustrated investors continue to dump the shares.

Not only has this created an attractive contrarian investment opportunity, but it has also caused the premium for selling puts to be higher (fear, uncertainty, and volatility drive up premiums on options). For example, the following table shows the current premiums available for selling Gilead puts.

We like the June 16th $62.50 strike price, and may open a position soon. We like it because with less than three weeks to expiration the annualized premium is nearly 12% (($0.42/$62.5) x (52-weeks / 3-weeks), and even if the shares get put to us we like them from a contrarian standpoint (plus we’d be buying them at lower price than the current market price), and Gilead pays a big (and growing) 3.2% dividend yield. We wrote about the attractiveness of healthcare and drug-maker stocks back in April, at which time we did not like Gilead (read that article here). However, since that time, Gilead’s price has fallen nearly 13%, its dividend yield has continued to rise, and it’s getting harder to ignore.

3. International Business Machines (IBM), Yield: 3.9%

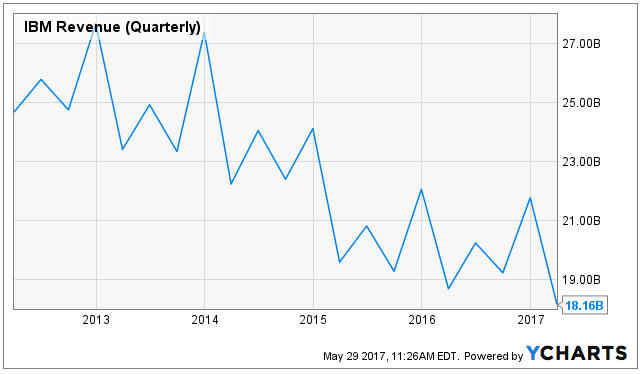

IBM is a hated stock, but it also pays a big dividend and it is a hugely profitable company. The narrative against IBM is that it’s a technology dinosaur and its quarterly revenues keep declining year over year (which is true, they do, as shown in the following chart).

However, the reason revenues are shrinking is because IBM’s enormous backlog of legacy business (nearly $120 billion in contracts) is slowly rolling off the books over many years. It’d be better if this business was growing not shrinking, but it’s still profitable business, and there is still a lot of it. Plus the legacy business gives IBM important customer relationships and insights to help it grow its newer businesses such as dynamic enterprise technology consulting, a developer network (built around Watson) and its hybrid cloud solutions. IBM isn’t a flashy tech company like Amazon, Google and Facebook, it’s a steady blue chip that has many years of profits (and big dividends) ahead. Additionally, the premium for selling IBM puts is attractive, in our view, as shown in the following table.

Specifically, we like the July 21st puts with a $145 strike price. If the shares get put to us then we own a big dividend blue chip at a lower price. And if the shares don’t get put to us before the option expires then we’re happy to keep the $1.46 in options premium. For reference, we wrote about IBM the last time we thought it looked cheap (19 months ago), and you can read that write-up here: Stop Hating IBM, It’s Enormously Profitable.

4. Verizon Communications (VZ), Yield: 5.1%

Verizon has faced a variety of challenges lately ranging from the troubled Yahoo acquisition, to the constant battle to feed its dividend, to dividend stocks simply falling out of favor following the Trump election.

However, despite the challenges, we believe Verizon’s dividend remains very safe, and the shares are trading at an attractive price. For example, consider our recent articles:

Nonetheless, if you’re still not comfortable buying shares at this price, you may want to consider selling put options. For example, the July 21st, $44.00 strike is worth considering, as shown in the following table.

Specifically, these puts will pay you $0.60 now, and if the shares get put to you before expiration, then you get to buy a very high quality big-dividend stock at an even lower price. You keep the $0.60 in premium income regardless.

5. Goldman Sachs (GS), Yield : 1.3% (and growing)

The banking industry has come a long way since the financial crisis, and there are catalysts on the near horizon that could drive earnings and multiples higher (e.g. another interest rate hike, positive CCAR results, continued GDP growth, and positive earnings announcements), but there is still also uncertainty in the air related to all of those catalysts, and for these reasons investors may want to consider selling puts. For example, the $2.52 premium available for selling July 21 $210 strike puts (as shown in the following table) is interesting.

Considering the string of significant financial announcements and catalysts coming up over the next two months, it wouldn’t be surprising to see volatility pick up, and the shares may actually trade down to $210 (or lower). However, given the strength of the economy and the banking system since the financial crisis, we believe it’s more likely for the shares to keep rising in the future. Selling puts gives investors the chance to own the shares at a lower price, and if the options never get executed then the seller can simply keep the $2.52 per contract which annualizes to around 7.2% per year, not bad for a dividend growth stock, in our view. And worth noting, the market may actually start to assign a higher valuation multiple in the coming months considering the target on Goldman Sach’s back since the financial crisis may finally lifting considering it’s improved operational strength and more reasonable risk exposures.

Conclusion:

As we mentioned more than once in this article, selling puts is not for everyone. If you’d like more ideas on how to implement this strategy, consider our members-only article, An Attractive High-Income Dividend Growth Options Trade. And if you are simply a dividend growth investor, we believe all five of the stocks mentioned in this article are worth considering based on their discounted prices, and steady growing dividends. Further, if you’re looking for more attractive high yield stocks, consider our recent article: 10 Attractive High Yield-Blue Chips for Contrarians. There are some attractive long ideas (and options opportunities) on that list as well.