Carl Icahn has a reputation as a corporate raider, and he is currently the chairman of the board at big-dividend (10.2% yield) holding company, CVR Energy (CVI). CVI is engaged in petroleum refining and nitrogen fertilizer manufacturing through its holdings in CVR Refining (CVRR) and CVR Partners (UAN), respectively. It is tempting to bet against UAN and bet in favor of CVRR considering President Trump's lack of enthusiasm for Environmental Protection Agency regulations and his friendship with renewable energy short-seller Carl Icahn.

However, we believe it's better to more fully align your interests with Carl Icahn by owning CVI (instead of CVRR or UAN) because even though Icahn is the puppet-master for all three, he'll keep pulling strings in favor of CVI because that's the big-dividend entity through which he profits most directly.

About CVI

As a holding company, CVI's profits are largely derived from an amalgamation of its interests in CVRR and UAN. For starters, the following chart shows the organizational ownership structure of CVI relative to CVRR and UAN.

As the chart shows, Icahn Enterprises owns 82% of CVI. And through related operational entities, CVI owns 53% of UAN and 66% of CVRR. This is important because it means Icahn directly owns most of all three publicly traded entities, but has the largest and most direct ownership of CVI. This is also important because if there are conflicts of interest between the three, Icahn has incentive to favor CVI because that organization most directly benefits him.

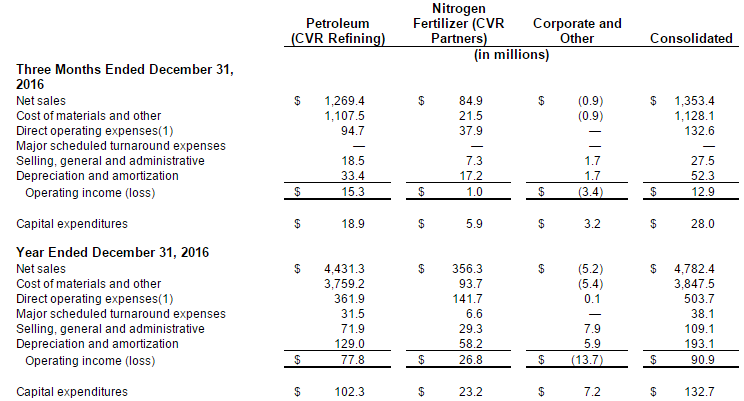

For perspective, the following financial table shows that CVI's profits are essentially a consolidation of its ownership in CVRR and UAN.

(Image source: CVR Earnings Release)

Conflicts of Interest

The CVI ownership structure creates conflicts of interest between Icahn and some of the shareholders of CVRR and UAN. For example, CVI pays a huge dividend now, but UAN and CVRR's dividends were cut to zero. And this makes sense considering Icahn benefits most directly from CVI. Specifically, why would Icahn want to pay a dividend to UAN or CVRR considering more of the money goes to him if he pays a dividend only through CVI. For example, the public owns 47% of UAN and 30% of CVRR, but only 18% of CVI. So by paying dividends only through CVI, more of the money goes directly to his Icahn Enterprises, which owns 82% of CVI.

Similarly, CVI has zero debt, but UAN and CVRR have debt (Note: The debt shown on CVI's balance sheet is simply a consolidation of UAN and CVRR debt as required by GAAP, but CVI has zero direct debt of its own). And this makes sense because why wouldn't Icahn make those two entities pay the debt considering they have a higher public, non-Icahn ownership than CVI.

Similarly, if the stuff hits the fan, Icahn can take one of those two entities into bankruptcy, but not before structuring deals that benefit CVI or even transfer assets to CVI and liabilities to whichever scapegoat he decides to bankrupt. (For example, in the 80s, Icahn profited via a hostile takeover and asset stripping of American Airlines' TWA).

RIN Credits

Renewable Identification Number (RIN) credits are another potential conflict of interest, although in this case, the conflict is based on Icahn's relationship with President Trump (Icahn is a special advisor to the president thereby providing input on regulation). CVI is required by environmental regulation to purchase RIN credits when it produces gasoline. (RINs are basically used to mandate a certain percentage of gasoline in the US is composed of corn-based ethanol). However, Icahn has been speculating in the RIN market, while he's also been lobbying Trump to make changes to the market that would benefit CVI. For example, According to Bloomberg:

"Icahn's campaign got a boost when Trump won the election last year, causing RIN prices to decline. They also dropped when Trump, with input from Icahn, selected Scott Pruitt to lead the EPA, and again when the president-elect announced Icahn's special adviser role. Yet another decline came on Feb. 28, after Icahn conveyed a proposal to the White House to change the point of obligation and helped persuade an ethanol group to drop its opposition."

This is important because according to the same article:

"CVR Energy took the rare step of selling large quantities of the [RIN] credits on two occasions last year. The first took place in August, around the time Icahn wrote to the EPA demanding a change in the regulations, the service reported. Another came in December, when Pruitt's selection was announced."

And in the meantime, Icahn has been delaying his required purchase of credits (he has up to a year to purchase them), a move that essentially means he is shorting the RIN market. Icahn is either betting RIN prices will go down, or, if the regulation he is lobbying for goes through, he won't have to buy RINs at all because the point of purchase obligation will be shifted by regulation from CVI to companies that actually blend the fuel (i.e. CVI will benefit because this large volatile expense will be moved completely off their books to another unrelated entity altogether).

About UAN

Worth noting, CVR Partners, the nitrogen fertilizer business, actually benefits from the Environmental Protection Agency's ethanol gasoline requirements. Demand for nitrogen fertilizers (used to fertilize corn) increases when demand for corn increases, and demand for corn increases as regulations requiring ethanol in gasoline increases. To some extent, this is a natural hedge on CVI's two-pronged business (refining and fertilizer). However, the refining business is much larger than the fertilizer business, therefore, refining is the much larger driver of CVI's success.

Also worth noting, UAN enjoys a distinct competitive advantage in that an alternative and reliable source of input for nitrogen fertilizer is a coke byproduct produced at a nearby CVRR refining facility.

Also worth considering, the company's most recent earnings release noted positive market conditions as follows.

"Nitrogen-based fertilizers remain solidly in demand, driven by a growing world population, changes in dietary habits and an expanded use of corn for the production of ethanol. Supply is affected by available capacity and operating rates, raw material costs, government policies and global trade. A decrease in nitrogen fertilizer prices would have a material adverse effect on the nitrogen fertilizer business' results of operations, financial condition and cash flows."

Conclusion

Before investing in any of the CVR entities, it makes sense to consider the potential conflicts of interest. In particular, it makes sense to align your interests with Icahn's considering he's the one pulling the strings at all three companies but benefiting most directly from CVI. It also makes sense to consider the current regulatory environment under President Trump, as well as Icahn's relationship with Trump.