It’s no surprise that Verizon is still willing to acquire Yahoo (albeit at a $300 million lower price following the relatively recent revelation that Yahoo’s data breach was dramatically more widespread than originally announced) because Verizon Still Needs Yahoo. Specifically, Verizon’s dividend payout ratio has continued to climb higher, and without the cash flows that Yahoo will provide, Verizon will likely be forced to sell more assets to maintain its big dividend payments. Either way, Verizon’s share price has come down, the dividend is safe, and Verizon is a decent place to have your money, especially considering the current historically low levels of market volatility likely won’t last forever.

Dividend Payout Ratio

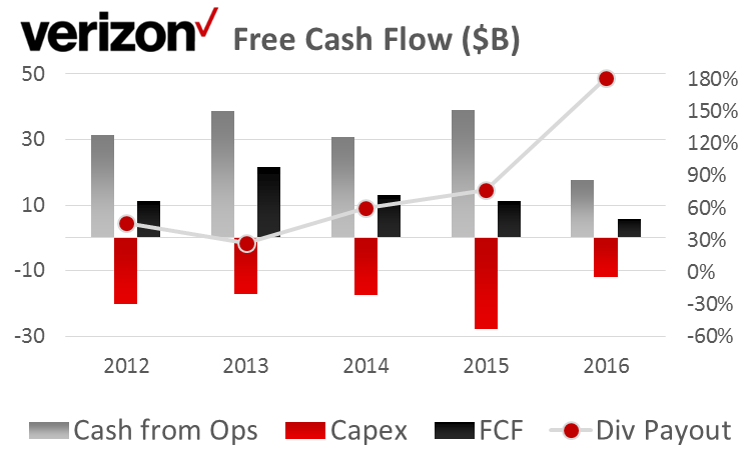

For some perspective, the following chart shows Verizon’s dividend payout ratio through the end of 2016.

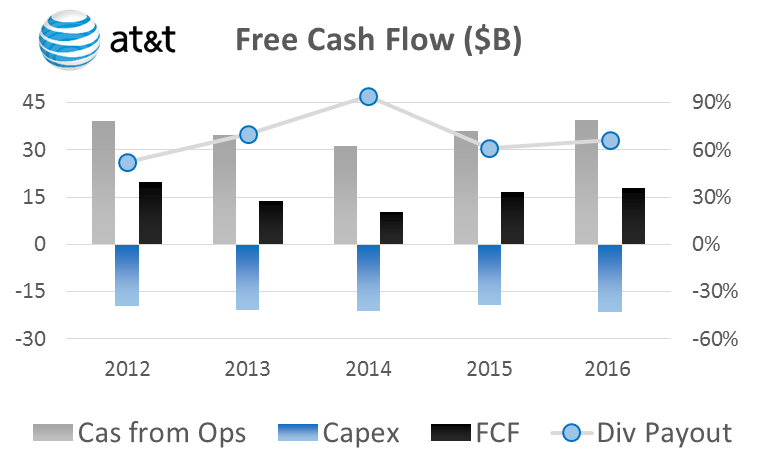

The key takeaway is that the payout ratio (Dividend / Free Cash Flow) has recently climbed to an unsustainable level as industry competition has intensified and the overall industry is changing. For perspective, here is the same chart for AT&T

Unlike Verizon, AT&T was able to address its precipitously rising dividend payout ratio several years ago with its DirectTV acquisition (this acquisition helped AT&T better cover its dividend payments, and adapt to the changing industry/market conditions).

The expectation is that Verizon’s Yahoo acquisition will address its growing payout ratio in much the same way DirectTV helped address it for AT&T. But even if the Yahoo acquisition doesn’t go through (we believe it will) then Verizon can continue to support its big dividend by selling assets. For example, Verizon helped support its big dividend payments in 2016 by selling some of its telecom properties to Frontier Communications (FTR) for $3.3 billion in cash and $5.2 billion in Frontier stock, and Verizon also raised over $5 billion in cash in 2016 by selling tower assets to American Tower Corp. (AMT). Either way, we believe Verizon’s dividend is safe.

Price, Yield and Forward P/E

If you are an income-focused investor, and you agree Verizon’s dividend is safe, then now might be a decent time to consider purchasing shares. For starters, Verizon’s share price has recently come down and its dividend yield has increased as shown in the following chart.

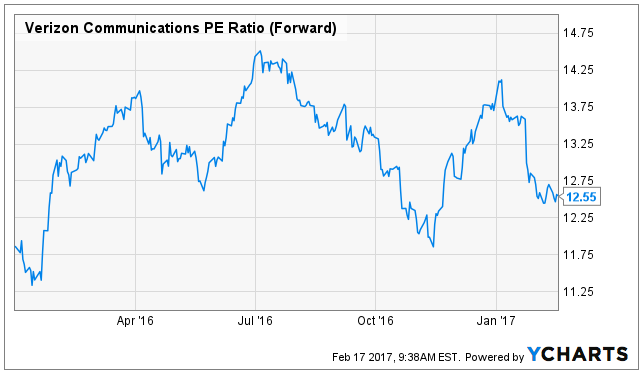

Further, Verizon’s forward price-to-earnings ratio is not unattractive as shown in the following chart.

Aside from uncertainty about the Yahoo deal, Verizon, AT&T and other low volatility big-divided payers have come down recently as it’s been a “risk on” market environment (i.e. safe haven stocks like Verizon are out of favor).

Market Volatility

The following chart shows current and historical market volatility as measured by the market “fear index,” otherwise known as the “VIX.”

And considering the VIX is near historically low levels, now may be a good contrarian opportunity to consider “safe haven” stocks such as Verizon. Specifically, if and when “fear” returns to the market (which we believe it will), stocks like Verizon will likely hold up better than other higher risk investments, and Verizon will continue to pay its big safe dividends.

Conclusion:

Verizon’s price is low because of uncertainty (and a general uneasiness) about the Yahoo deal, and because lower volatility safe-haven stocks are out of favor. We believe this type of contrarian special-situation can create some of the best investment opportunities, and we’ve highlighted a few more of them here: Six Special Situations Worth Considering. And if you’re simply a lower-risk, income-focused investor, now is a decent time to consider adding shares of Verizon.