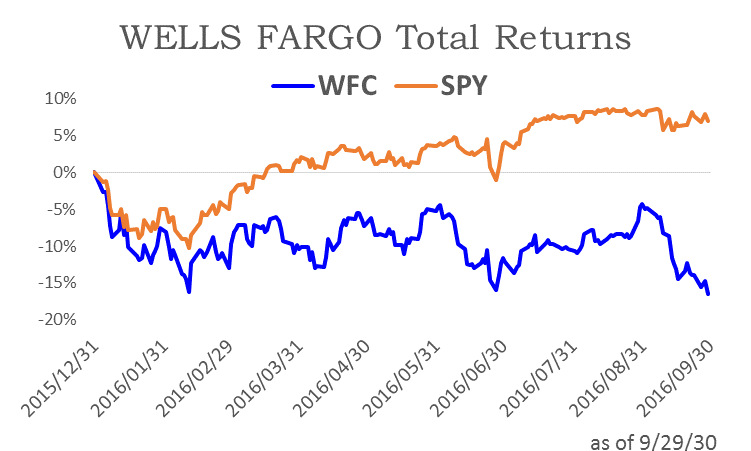

If you are a long-term income-focused investor, Wells Fargo continues to pay a big attractive dividend (3.4%). And the contrarian in you may even be considering buying more shares after it took another beating from Congress yesterday for its fake-account-opening scandal (it’s now down 12.7% this month versus down 0.7% for the S&P 500 on a total returns basis). But what you may not have considered is the sharp jump in premium for writing Wells Fargo covered calls, and how this is a relatively low-risk options strategy for long-term investors to increase their income.

About Wells Fargo

Wells Fargo is one of the systemically important big banks, it pays a big dividend, and until recently it was a Main Street darling because of its limited Wall Street exposure, its passing stress test marks, and its highly admired large shareholder- Warren Buffett. However, that all changed this month as news of the fake-account-opening scandal broke, and our US Congress men and women more recently have turned it into a punching bag of one-upmanship to see who can say more horrible things about Wells Fargo and its executives. So just when investors thought it was finally safe to invest in Wells Fargo (e.g. the financial crisis was far enough in the rear view mirror, and interest rates were about to rise), it got hammered, and the full repercussions of the latest scandal are still unknown (e.g. the $41 million CEO bonus clawback isn’t enough, and if Hillary Clinton gets to carry on the Barack Obama Justice Department torch there will surely be enormous multi-billion dollar fines coming down the pike).

Wells Fargo Covered Calls

For those of you with no intention of selling Wells Fargo (as well as those of you contrarians considering buying shares now that the price has fallen), we believe the dividend is still safe (because it generates lots of cash from operations to cover the dividend, and unlike other big-banks Wells Fargo generates a return on capital that exceeds its cost of capital), and a Wells Fargo covered calls strategy just got much more attractive, in our view.

If you don’t know, a covered call strategy involves collecting extra income by selling a call option on a stock you already own. If the price of the stock climbs above the call price, it will be taken off your hands (called) at the pre-determined call price (you keep the premium and get the cash from the sale). If the call option expires unexecuted, then you keep the stock as well as the premium you received for selling the call.

For reference, this table shows the premium for selling Wells Fargo call options seven weeks before they expired back at the end of June versus the premium for selling Wells Fargo call options now with seven weeks until expiration as of this morning.

What stands out to us is that Wells Fargo call options pay significantly higher premiums now than they did back at the end of June (even after considering the upcoming 10/14 earnings release- Wells Fargo tends not to have big earnings surprises). And for income-focused investors, the higher premiums mean higher income for writing the calls.

In a nutshell, we believe Wells Fargo remains an attractive long-term investment for income-focused investors, and we consider a covered calls strategy particularly attractive now that volatility has jumped. Specifically, if you own the stock and write the $47 strike, then you make 6.8% income (($47-44.37+0.39)/44.37) over the next seven weeks if it gets called (not including the upcoming dividend payment), and if it doesn’t get called then you get to keep the premium and a very attractive long-term dividend stock, Wells Fargo.

What are the Risks?

Of course there are risks to owning Wells Fargo and writing covered calls. For starters, the strategy forfeits some of the upside potential in exchange for income. For example, if Wells Fargo stock rises dramatically (say 20%) over the next seven weeks then you’d only gain 6.8% (see calculation above), (plus you possibly get to keep the dividend payment, depending on when the stock gets called). However, the chance for this kind of upside seems unlikely considering the latest scandal isn’t going to just disappear, and the fed isn’t likely to dramatically raise interest rates during this period (even a 25 basis point increase wouldn’t cause a 20% price jump).

Another risk is that there is still another shoe to drop, the price of Wells Fargo continues to decline dramatically, and you’re left holding a stock that is worth far less than its current price. In the short-term, this is certainly possible. Further, even though Wells Fargo is already making efforts to clawback $41 million in CEO stock awards, and the company is ending its aggressive retail sales goals (which created the misaligned incentives that caused the scandal in the first place), there could be more significant short-term pain from regulators and lawmakers. However, in the long-term it seems Wells Fargo simply has far too much profitable business that will prevent the price from staying low forever (remember Wells Fargo’s return on capital exceeds its cost of capital, plus it is the second largest bank in the world). We continue to believe Wells Fargo is an attractive long-term investment, and if you are a long-term owner then the short-term volatility shouldn’t bother you (especially considering the big steady dividend payments, plus the potential for extra income via covered call premiums).

Additional risks for Wells Fargo include the possibility that interest rates never rise, the yield curve gets even flatter (thus further pressuring net interest margins), more scandals break, and new regulations and DOJ lawsuits destroy the bank’s profitability altogether. In this case, you’d still get the premium for selling the calls, but it could be more than offset by declines in the stock’s price.

Conclusion

We believe Well Fargo presents an attractive long-term opportunity for income-focused investors because of its highly-profitable business and its big dividend payments. In the short-term, uncertainty remains higher than usual, and for this reason the premium on Wells Fargo call options is also higher than usual. We view this as an opportunity for long-term Wells Fargo owners to pick up extra income by writing relatively low-risk covered call options. Additional information about our views on Wells Fargo and on current option trading opportunities is available in our recent article: Conservative Options Opportunities and Wells Fargo.