In this report, we review a manufacturer of advanced lithium-ion batteries. This early-stage public company is well-positioned to benefit from growing demand, including mobile, Internet of Things (IoT) and electric vehicles. Key differentiators include its energy density advantage (achieved through design and architecture choices) and silicon anode technology. It also addresses key safety concerns. We analyze the business model, market opportunity, financials, valuation and risks. We conclude with our opinion on investing.

(Note: you can access a pdf version of this report here).

Overview

Founded in 2007, Enovix Corporation (ENVX) is engaged in designing, developing, manufacturing, and commercializing advanced Lithium-ion batteries. It has developed a proprietary three-dimensional ("3D") cell architecture that allows higher energy density, longer cycle life, and superior safety compared to conventional wound lithium-ion cell battery architectures. Enovix's unique approach involves using a 100% active Silicon Anode, which is a significant departure from the historical practice of combining only a modest amount of silicon with graphite at the anode. This approach enables the company to produce smaller, cheaper, and more efficient lithium-ion batteries at scale, making them a compelling alternative to current battery options.

Enovix has primarily focused on researching, developing, and selling its silicon-anode lithium-ion battery technology. It has secured contracts with established companies in the consumer electronics industry for the provision of engineering and proof-of-concept samples. These companies produce devices such as smartwatches, augmented reality/virtual reality devices, smartphones, fire/life/safety radios, and laptops. Additionally, the company is exploring new market opportunities beyond consumer electronics, including the potential of its battery technology in the Electric Vehicle (EV) market.

Enovix operates its business in a single segment, and generates revenue from two primary sources: "Product Revenue" and "Service Revenue." Product Revenue is derived from the sale of silicon-anode lithium-ion batteries and battery pack products, while Service Revenue is obtained from executing engineering contracts for the development of silicon-anode lithium-ion battery technology. The company began generating revenue from product sales in Q2 2022 and as a result the contribution of Product Revenue to the overall revenue remained miniscule in Q1 2023. The majority of the company's revenue in Q1 2023 was generated from providing engineering services for battery technology development.

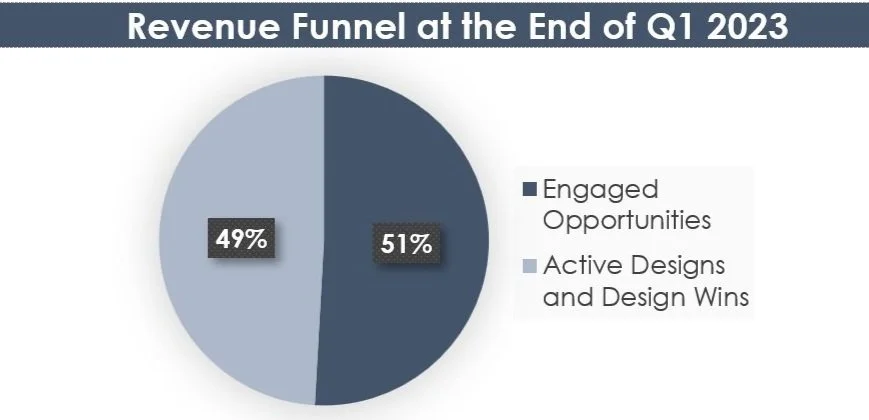

At the end of Q1 2023, the company's “revenue funnel” was $1.5B, consisting of $744M in Engaged Opportunities and $718M in Active Designs and Design Wins. The “Engaged Opportunities” metric refers to customers currently evaluating the company's battery technology, while the “Active Designs and Design Wins” metric includes customers who have completed evaluation, identified the end-product, and started design work or are in the process of qualifying one of the company's standard batteries for a formally approved product.

Source: Company’s 10-Q

Leveraging Innovative 3D Silicon Lithium-Ion Battery Architecture for Better Performance and Safety

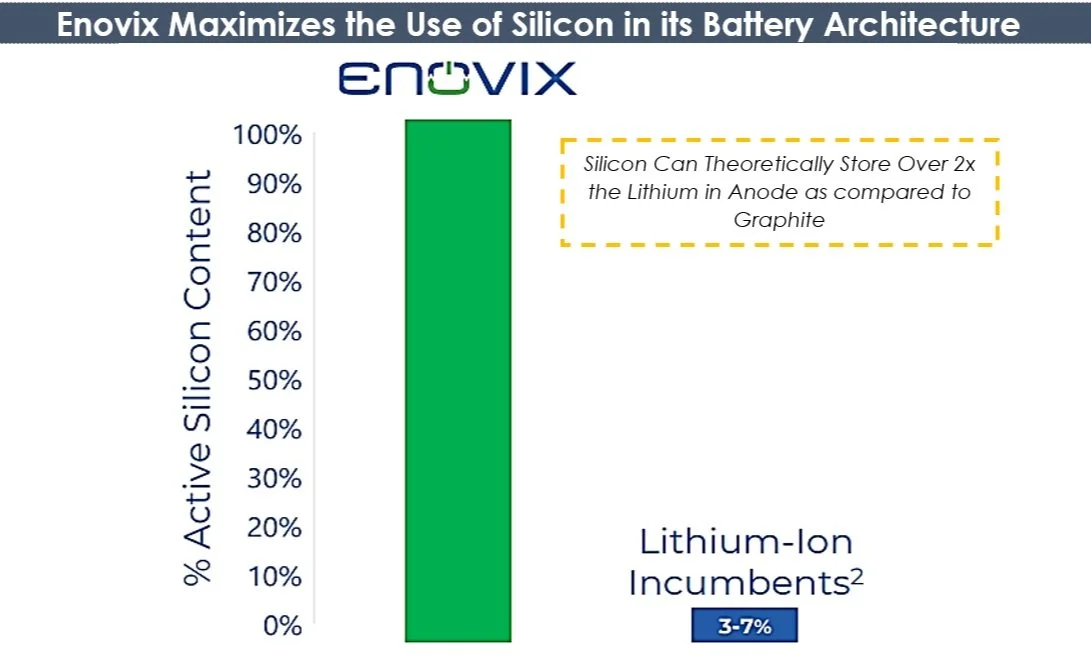

Enovix has developed a revolutionary 3D Silicon Lithium-ion battery design that leverages the potential of silicon to significantly enhance battery performance. Unlike traditional graphite anodes, silicon anodes have the ability to store over double the amount of lithium, leading to a 36% increase in battery capacity and improved energy density.

"Silicon anodes can store ten times as much charge in a given volume than graphite anodes - a whole order of magnitude higher in terms of energy density. The problem is, as the lithium ions move into the anode, the volume change is huge, up to around 400%, which causes the electrode to fracture and break." - Dr. Marta Haro, a former researcher at Okinawa Institute of Science and Technology (OIST)

Although Silicon has the potential to improve battery performance, its use has been historically muted due to swelling and cracking issues during charging and discharging. Moreover, compared to graphite anodes, silicon anodes have a lower formation efficiency in the first cycle, which limits their adoption in conventional battery cell architectures. However, Enovix has developed a 3D cell architecture that overcomes these challenges. The company’s pre-lithiation process effectively addresses the limitations of conventional designs, resulting in durable battery cells that can endure up to 500 cycles. Enovix aims to further extend the cycle life of its 3D Silicon Lithium-ion battery to 1,000 cycles or beyond.

Source: Investors Presentation

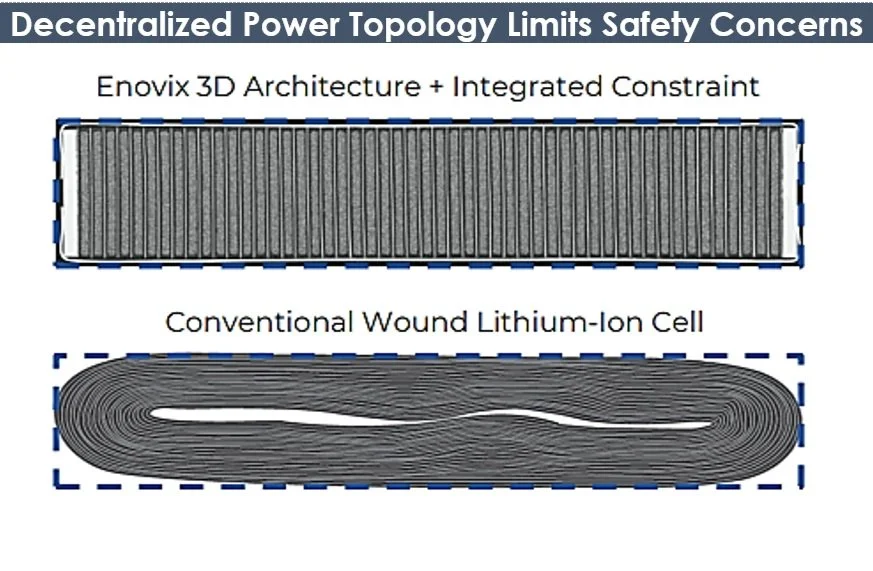

In addition to performance issues, the use of a 100% active silicon anode has historically raised safety concerns pertaining to overheating and explosions. Enovix, however, has addressed these concerns as well with its proprietary BrakeFlow technology, which effectively mitigates excessive heating and explosion hazards. This is achieved through the integration of a resistor at the potential short circuit location and by evenly distributing voltage. Enovix's innovative architecture, which is similar to Enphase's (ENPH) approach to revolutionizing the solar energy market by incorporating micro-inverters at the panel level, adds exceptional tolerance against thermal runaway.

“Not only does our architecture enable a 100 percent active silicon anode, which notably increases energy density, but also enables us to launch new innovations like BrakeFlow, which by design, reduces the temperature rise at a short location, adding exceptional tolerance against thermal runaway.” - Ashok Lahiri, Co-Founder and CTO

Source: Investors Presentation

Large, Fast-Growing Total Addressable Market (TAM)

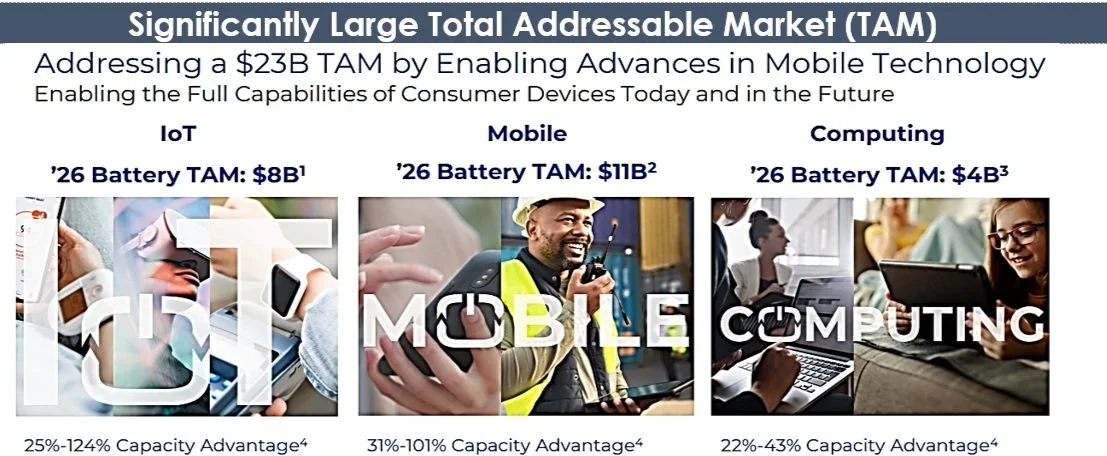

Enovix is targeting the mobile computing market, which it projects will grow to $23B by 2026. This market is divided into three subcategories: IoT ($8B), mobile ($11B), and computing ($4B). With a $1.5B revenue funnel as of Q1 2023, Enovix currently has a market penetration of 6%. The company's management team believes that its battery offers a significant capacity advantage over existing batteries in select products in these subcategories. Specifically, Enovix estimates that its battery can offer a 25% - 124% capacity advantage in the IoT market, 31% - 101% advantage in the mobile market, and 22% - 43% advantage in the computing market, relative to existing batteries.

Source: Investors Presentation

Enovix is currently focused on the high-margin consumer electronics market, where its innovative battery technology allows it to command higher prices. However, the company also has plans to foray into the Electric Vehicle (EV) market in the long term. The company projects the global EV market to register a strong CAGR of 17% from $20B in 2020 to reach $523B in 2040, giving Enovix ample headroom for incremental growth.

Source: Investors Presentation

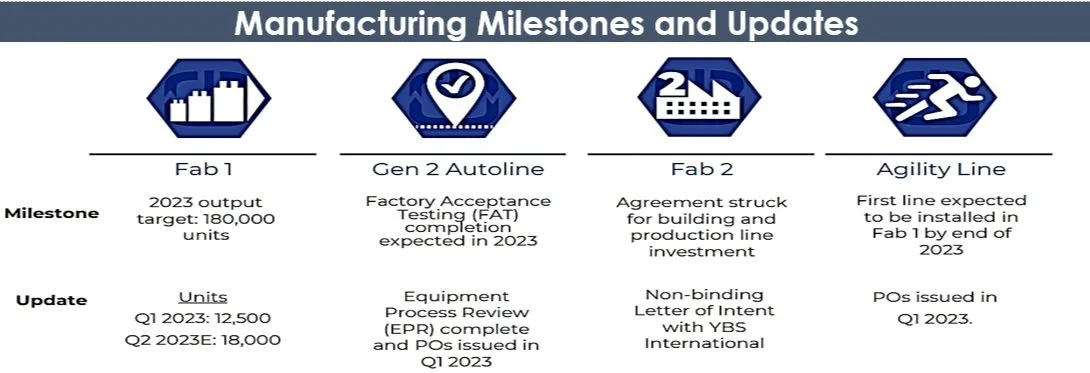

Driving High Volume Production By Adding More Facilities and Improving Manufacturing Yield in Existing Facilities

Enovix has developed advanced battery technologies through partnerships and investments from the solar and semiconductor industries. The company has received positive feedback from customers on its sample batteries since 2018. It achieved its first production revenue from Fab 1, located in Fremont, CA in Q2 2022, manufacturing standard battery cells for wearable and IoT devices. Enovix plans to manufacture battery cells for mobile devices in early 2023 and establish an "Agility Line" for custom cell development by the end of the year.

Source: Investors Presentation

Evonix is also setting up high-volume manufacturing infrastructure in Malaysia, having established Enovix Malaysia and hired a VP of Operations and 25 engineers. The company's Fab 2 has the potential to produce 38M to 75M batteries annually, depending on cell size. The company signed a non-binding Letter of Intent (LOI) with YBS International Berhad, an investment-holding publicly traded company to locate its first Gen 2 auto line in an existing YBS building at the Penang Science Park in Malaysia. Enovix is currently collaborating with YBS to work with local banks and government authorities to secure at least $70M in financing to fund its Gen 2 Line 1 production.

Revenue Generation Commences, Yet Production Expansion Investments Weighing on Profits

Given it is still in nascent stages of commercialization, the company has only recently begun its journey in terms of revenue ramp-up in Q2 2022. In Q1 2023, the company generated revenue of only $21K and in FY2022, the company's total revenue was $6.2M, solely consisting of service revenues. These service revenues were earned by fulfilling all obligations and delivering pilot cells and battery packs to two customers under service revenue contracts. In Q1 2023, Enovix surpassed its initial estimate of 9,000 units by producing 12,500 wearable-size cells, which was a significant increase of 2.8x compared to the 4,442 units shipped in Q4 2022. This was possible due to enhanced production in Fab 1. In the near future, the company’s revenue will be lumpy given the early stage nature of its evolution.

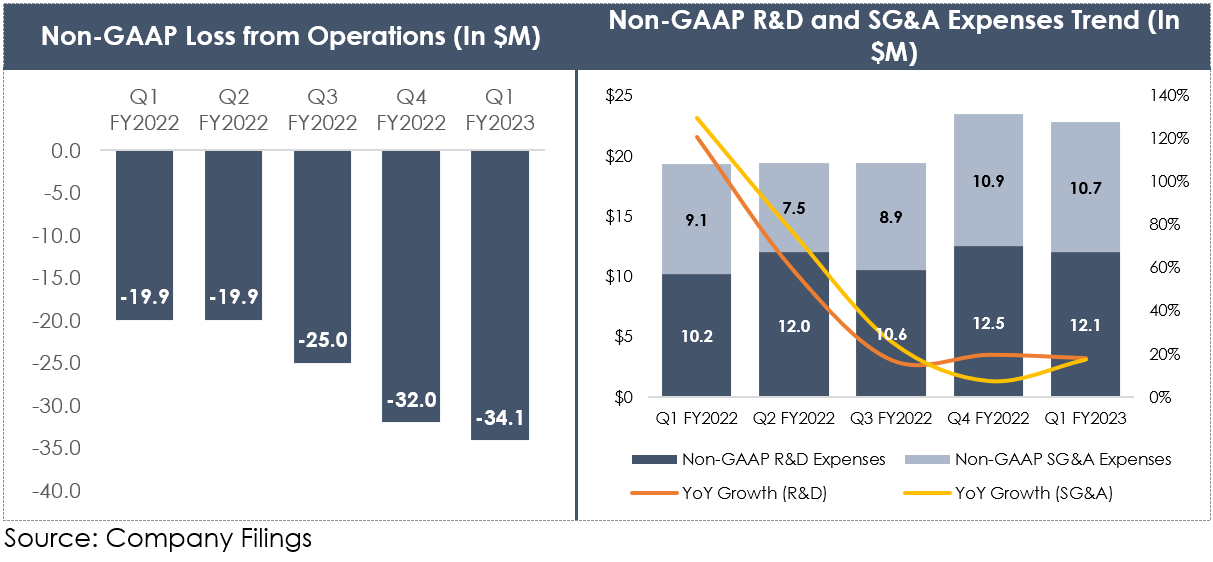

In terms of profitability, the company recorded a non-GAAP gross loss of $11.3M in Q1 2023, compared to a non-GAAP gross loss of $0.5M in Q1 2022. This increase in loss can be attributed to elevated material, labor, and other expenses pertaining to production ramp up. In Q1 2023, the company recorded a non-GAAP operating loss of $34.1M versus a non-GAAP operating loss of $19.9M in Q1 2022. This significant increase in loss was primarily attributed to a substantial rise in Research and Development (R&D) expenses (up 18% YoY) and Selling, General, and Administrative (SG&A) expenses (up 17% YoY) on a non-GAAP basis. Enovix anticipates that its overhead expenses will continue to rise over the next 12 months as it expands its manufacturing facilities and operations, necessitating the recruitment of additional personnel to provide support and maintenance.

Strong Financial Position Amidst Pressured Cash Flow from Manufacturing Expansion

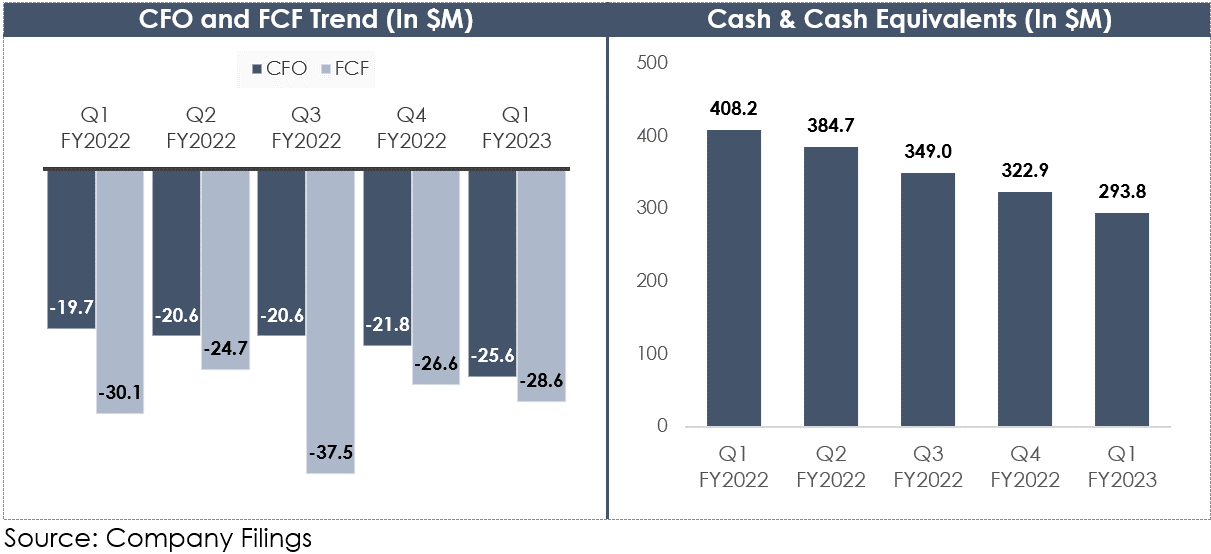

Enovix ended Q1 2023 with $293.8M in cash and cash equivalents, and following the recent convertible debenture offering, the company secured $148.4M in net proceeds, resulting in a pro-forma cash balance of over $440M, excluding the $70M Malaysian funding in the negotiation stage. The management team forecasts capital expenditures and operating cash expenditures of $120M each for 2023. With a current cash balance of over $440M and forecast expenditures of $240M, the company seems to have sufficient cash to fund its operations and capital expenditures for at least a year.

In Q1 2023, Enovix experienced a cash outflow of $25.6M from operating activities versus $19.7M in Q1 2022. It expects this outflow to increase significantly until it generates substantial inflows from battery manufacturing and sales. It incurred capex of $3.0M in Q1 2023, lower than the $10.4M spent in Q1 2022, resulting in a Free Cash Outflow of $28.6M in Q1 2023, compared to $30.1M in Q1 2022. As the company completes its battery manufacturing facility, it foresees higher costs associated with acquiring property and equipment in the near future.

Valuation:

Over the past one year, Enovix's shares have experienced significant appreciation of approximately 48% due to the commencement of production and the introduction of new product lines. Enovix possesses the potential to attain strong top and bottom-line growth in the long-term, driven by its innovative offering and anticipated growth of the battery market over the next decade, particularly in relation to the surge in EVs and other battery-powered devices.

Having said that, the company cannot be valued based on traditional market multiple methods as it is still in the early stages in its evolution. Despite that, given the size of the addressable market, we believe that Enovix’s current valuation of $2B has room to go significantly higher as it achieves progressive milestones in terms of client wins and production.

Risks:

Intense Competition: The Li-ion battery supplier market is fiercely competitive, featuring established and new players. Notable suppliers such as Panasonic Corporation, Samsung SDI, Contemporary Amperex Technology Co. Ltd., and LG Energy Solution Ltd. offer conventional Li-ion batteries while exploring silicon anode Li-ion battery development. Moreover, newer companies like Sila Technologies, offering a drop-in replacement for lithium-ion battery production similar to Enovix, pose notable threats. Success depends on factors including competitive pricing, cost management, energy density improvement, safety assurance, and cycle life extension. To stay competitive, Enovix must focus on product performance, cost-efficiency, reliability, product roadmap, customer relationships, and manufacturing scalability.

Conclusion:

Enovix distinguishes itself from other battery companies through its higher energy density, early leadership position, and progress in commercialization. The company has a commendable track record, and its team holds the potential to achieve significant outperformance in the long run if it meets key milestones. However, as is the case with many emerging technologies, the success of Enovix is not a given and hinges on its ability to effectively scale up and compete against established and newer players in high-volume markets such as smartphones, laptops, and automotive. Despite this inherent risk, we like the risk/reward opportunity for investors here focused on growth, given the size of the market potential and the important breakthroughs Enovix has already achieved. We view Enovix as a favorable opportunity for patient investors with a long-term outlook.