The Reaves Utility Income Fund (UTG) offers a big, steadily-growing, monthly-paid, tax-advantaged distribution (currently yielding 8.2%). And this closed-end fund (CEF) does so by owning utility-sector stocks (known for lower volatility and steady dividend payments). In this report, we review the fund (overview, philosophy, investment process), its advantages (tax favorability, monetary policy impacts and datacenter AI tailwinds) as well as risks (expenses, leverage, price premium). We conclude with our strong opinion on who might want to consider investing.

Overview:

The objective of this fund is to provide a high level of after-tax inome and returns. According to Reaves:

“The Fund’s investment objective is to provide a high level of after-tax income and total return consisting primarily of tax-advantaged dividend income and capital appreciation. The Fund pursues this objective by investing at least 80% of its total assets in dividend-paying common and preferred stocks and debt instruments of companies within the utility industry. Up to 20% of the Fund may be invested in the securities of companies in other industries.”

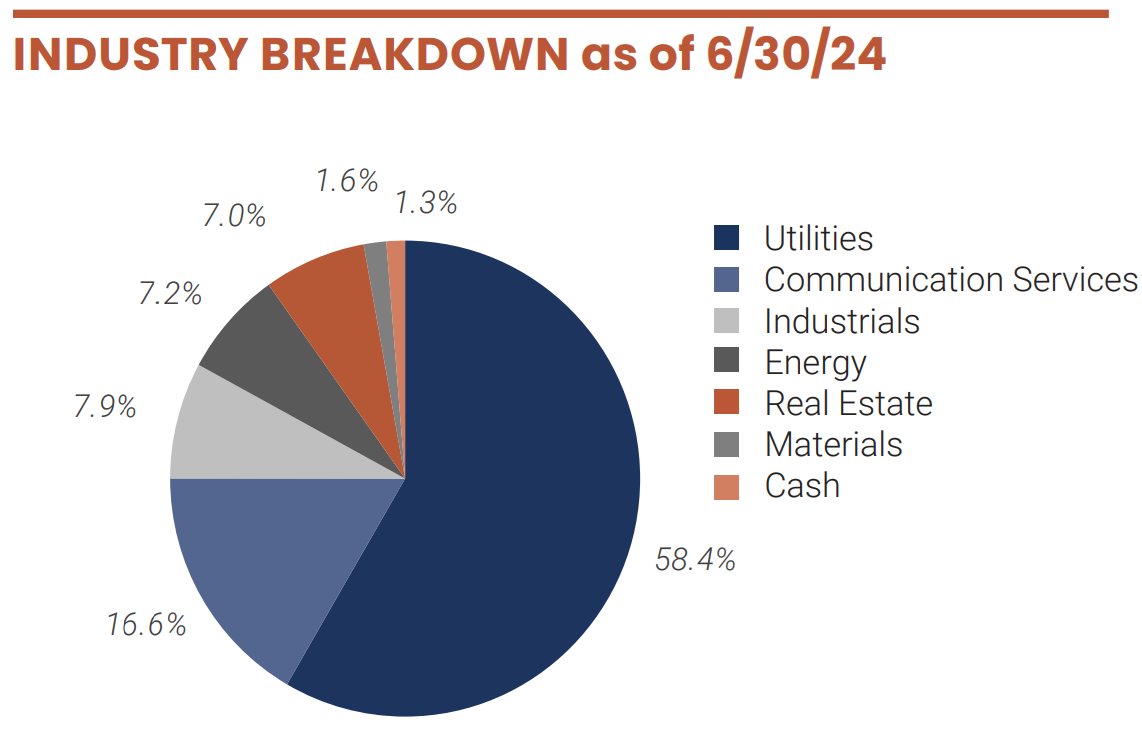

Apparently, the fund has a liberal definition of its own 80/20 rule regarding utility sector allocations (which is fine), as you can see in the following graph taken from UTG’s fund fact sheet.

We did submit an inquiry to UTG about the utilities sector allocation, and received a nice voicemail in return that explained:

"Hey, [Blue Harbinger]... calling from Reaves Asset Management, we're the advisor of the Reaves Utility Income Fund. Appreciated your question on utility allocations... We use a utility definition that is a little looser for the bulk of the assets as described in the prospectus."

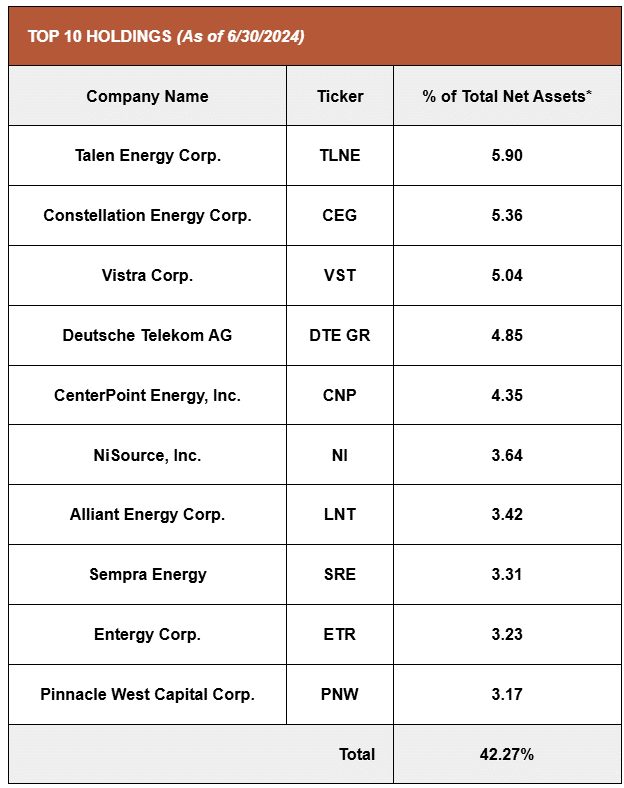

And for a little more perspective, the fund recently held 64 positions, including the following top 10 holdings:

Tax-Advantaged Income:

If you are wondering, the fund’s objective with regards to “after-tax income” is a reference to the fund’s preference for:

Qualified Dividends: which are typically taxed at 15%, which is lower than the ordinary income tax rate for most investors, and

Long-Term Capitgal Gains: which are also typically taxed at the lower long-term capital gains tax rate of 15% (again, lower than the short-term capital gains tax rate—which is taxed as ordinary income).

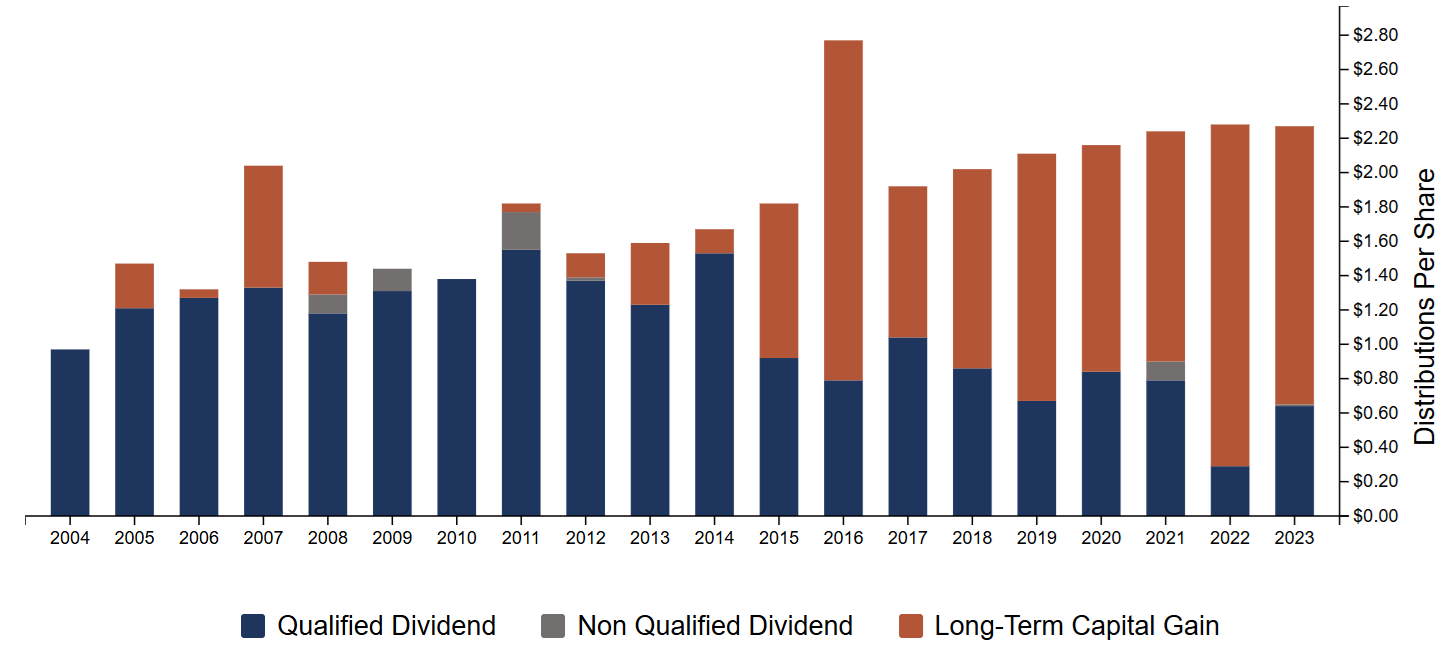

And UTG has been very successful in accomplishing these “tax-advantaged” objectives, as you can see in the following chart.

Specifically, most of UTG’s distributions are taxed at a lower rate (good if you own it in a taxable account), plus this give UTG an advantage ove many other high-income investments (whose distributions are often taxed at the higher ordinary-income tax rate).

Investment Philosophy and Strategy

UTG is actively managed (i.e. it’s not a passive index fund, the UTG team is actually picking stocks to hold in the fund). And the selection process is based on the fund’s invesment philosophy:

“Reaves Asset Management believes that companies’ characteristics drive their investment outcomes. Reaves favors companies which possess some, or all, of the following characteristics:

Operate in businesses with high barriers to entry

Face limited competition / higher regulatory scrutiny

Consistent, sustainable cash flow generation

Profitable in both up and down economic cycles

Dividends viewed as an important component of capital allocation”

And the fund team implements this philosophy through a thorough process involving qualitative assessments, valuation analyses and internally debating analyst recommendations, as described below:

“The Reaves research process begins with a thorough qualitative assessment of business fundamentals, including market and regulatory structures, competitive environments, and barriers to entry. Analysis is focused on identifying high quality assets with the ability to generate durable and growing cash flow streams. Companies that fit these investment criteria are then scrutinized by management quality, capital allocation, and governance. Valuation analyses are performed in the context of industry, market, and idiosyncratic factors. Individual analyst recommendations are thoroughly vetted for merits and risk via internal peer review. Ultimately, after vigorous internal debate, the firm’s portfolio managers strive for a consensus-driven approach to security selection.”

Historical Performance:

You can see the fund’s long-term performance (since inception in 2004) in the following chart. Specifically, we compare the performance of UTG to the utilities sector ETF ((XLU), which is a low-cost passive strategy) and the S&P 500 (SPY).

Source: Ycharts. Note: the chart utilizes total returns (which include price appreciation, plus distributions as if they were reinvested).

Interestingly, you can see the fund has underperformed the S&P 500, but it has also displayed less volatility than the overall market (SPY) in periods of high volatility (such as following the Great Financial Crisis of 2008-2009, and when the “pandemic bubble” burst in 2022).

Future Performance:

Obviously, no one has a working crystal ball, but monetary policy and growing demand on utility companies (related to AI energy needs) may impact the future performance of this fund.

Monetary Policy Vs. Utilities Stocks

As you can see in the performance chart above, UTG outperformed the market for an extended period of time (from ~2009-2020), but began underperforming when the US got aggressive with its pandemic stimulus measures (such as near-zero interest rates and extensive fiscal stimulus—which generally helped growth stocks more than utilities (value) stocks).

However, as we now may be entering a more “normal” phase of monetary policy (for example, interest rates are no longer 0% and they are dramatically less volatile than they were), we may see resumed strength from the Utilities sector as compared to more aggressive growth stocks (again, because the stimulus measures (that fueled a growth stock rally) have arguably been significantly reduced, and value stocks (like Utilities) may be significantly undervalued as compared to growth stocks (which many argue are overvalued based on the fact that a few top growth stocks (like Nvidia (NVDA), Microsoft (MSFT), Amazon (AMZN), Apple (AAPL) and Meta (META) now make up such a large portion of the US stock market’s total market capitalization)).

Increasing Energy Demand from AI:

Additionally, we may see new demand for energy related to the growing use of artificial intelligence "(“AI”) in data centers (which ultimately could be good for utilities stocks). For example, Reuters suggests that:

“U.S. electric utilities predict a tidal wave of new demand from data centers powering technology like generative AI, with some power companies projecting electricity sales growth several times higher than estimates just months earlier.

Nine of the top 10 U.S. electric utilities said data centers were a main source of customer growth, leading many to revise up capital expenditure plans and demand forecasts, according to a Reuters analysis of company earnings reports from the first three months of the year.”

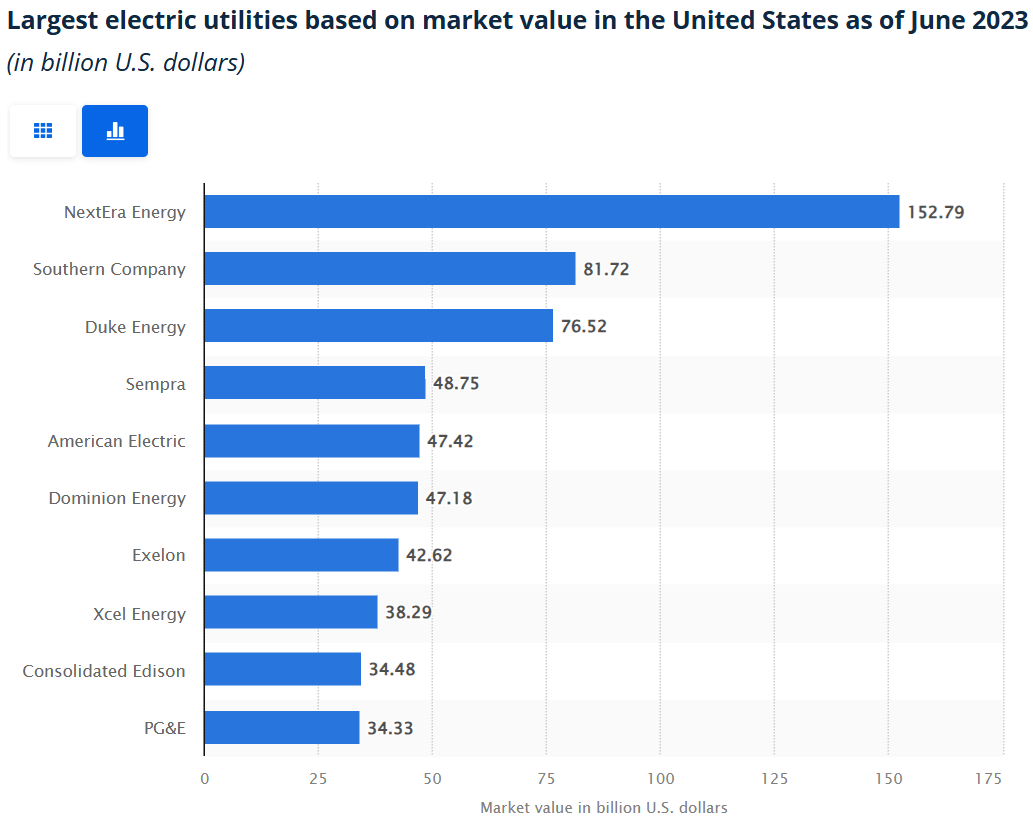

And for reference, here are the 10 largest US electric utilities companies (mentioned in the quote above). Importantly UTG currently holds 7 of them (and may be set to benefit).

source: Statista

For example, UTG's largest holding, Talen Energy (TLN) has recently signed a long-term deal (stability) with Amazon:

According to Talen Energy’s investor presentation, it will supply fixed-price nuclear power to Amazon’s new data center as it’s built. Amazon has minimum contractual power commitments that ramp up in 120 MW increments over several years. The cloud service giant has a one-time option to cap commitments at 480 MW and two 10-year extension options tied to nuclear license renewals.

And UTG's third largest holding Vistra Corp (VST) is also a big beneficiary, for example.

Additional Closed-End Fund Considerations:

As mentioned, UTG is a closed-end fund which comes with its own unique nuances versus other investment types. For example, you can see some important things to consider (in the following graphic) before investing in any closed-end fund.

source: Blue Harbinger Investment Research

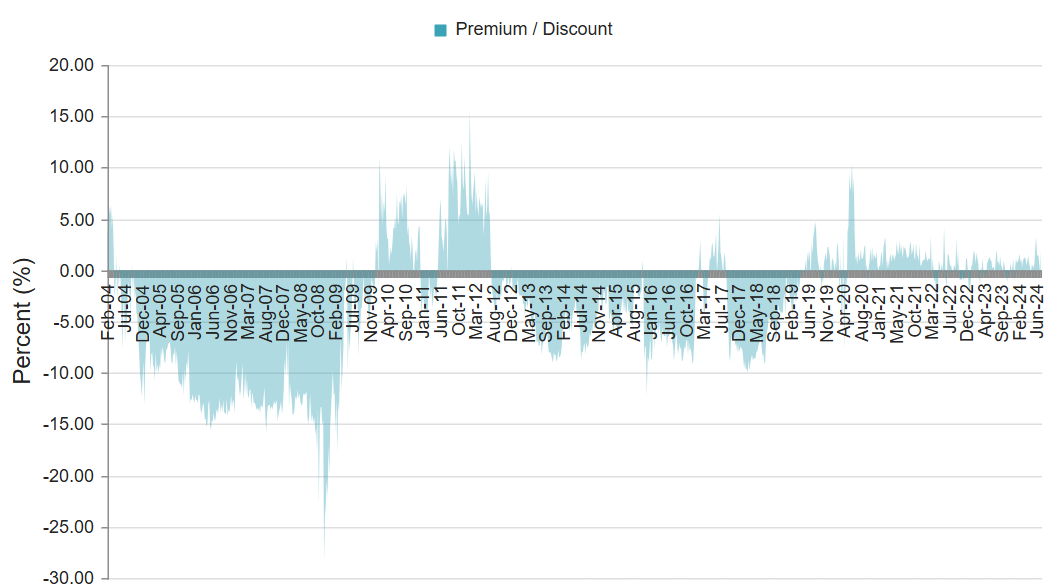

Price Premium

One important consideration is that CEFs do not continuously issue shares for sale (like a typical mutual fund), and as such CEF shares trade in the secondary market based on supply and demand. This also means CEFs can trade at market prices significantly different than the net asset value (“NAV”) of their underlying holdings.

As you can see in the chart above, UTG currently trades at a small premium to NAV. This premium is fairly reasonable compared to history, but it also creates a risk factor investors should keep in mind (i.e. there is no gaurantee that the fund will, or will not, move to a larger or smaller premium or discount in the future (which will impact investor returns).

Expense Ratio

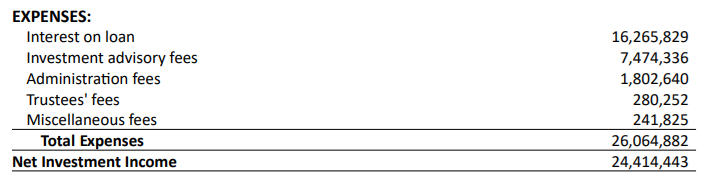

According to CEFConnect, UTG recently had a total expense ratio of 2.32%, which is significant. The expenses consist of management fees of 0.72%, other expenses of 0.21% and interest expense of 1.39% (this is the cost of borrowed money/leverage). Here is another breakdown according to the fund’s semiannual report.

We saw earlier the type of total returns this fund was able to post, and those were net of all these expenses. Not bad considering the fund also delivers big, steadily-growing distribution payments to investors each month, but still something for investors to consider.

Leverage

Like many CEFs, UTG uses borrowed money (leverage). This can magnify returns and income in the good times, but it can also magnify losses in the bad times. Based on this fund’s utility-focused strategy (utilities are typically less volatile than other market sectors) we view the fund’s recent leverage ratio of ~19.6% to be prudent and attractive. Just know this is part of the reason UTG is able to pay such large distributions (it magnifies income) but it is also a risk factor that should be monitored.

The Bottom Line

If you can get comfortable with the unique nuances of this particular CEF, UTG is worth considering for your income-focused taxable account. Not only does it have an impecable distribution track record, but it is poised for more gains ahead. Overall, disciplined, goal-focused, long-term investing continues to be a winning strategy.