Despite all the gloom and doom in the market, and despite the big reasons to stay bearish (as we will review in this report), the market will eventually recover and go much higher. We don’t know if the majority of the selling is over, or if things will continue to get worse in the short-term (no one does). But we do know that over the long-term we expect the market to eventually recover and go much higher. In this report, we review the terrible market environment, including data on 150 top growth stocks that have sold off hard, and then rank our top 10 long-term growth stocks from the list, counting down from number 10 and finishing with our top ideas.

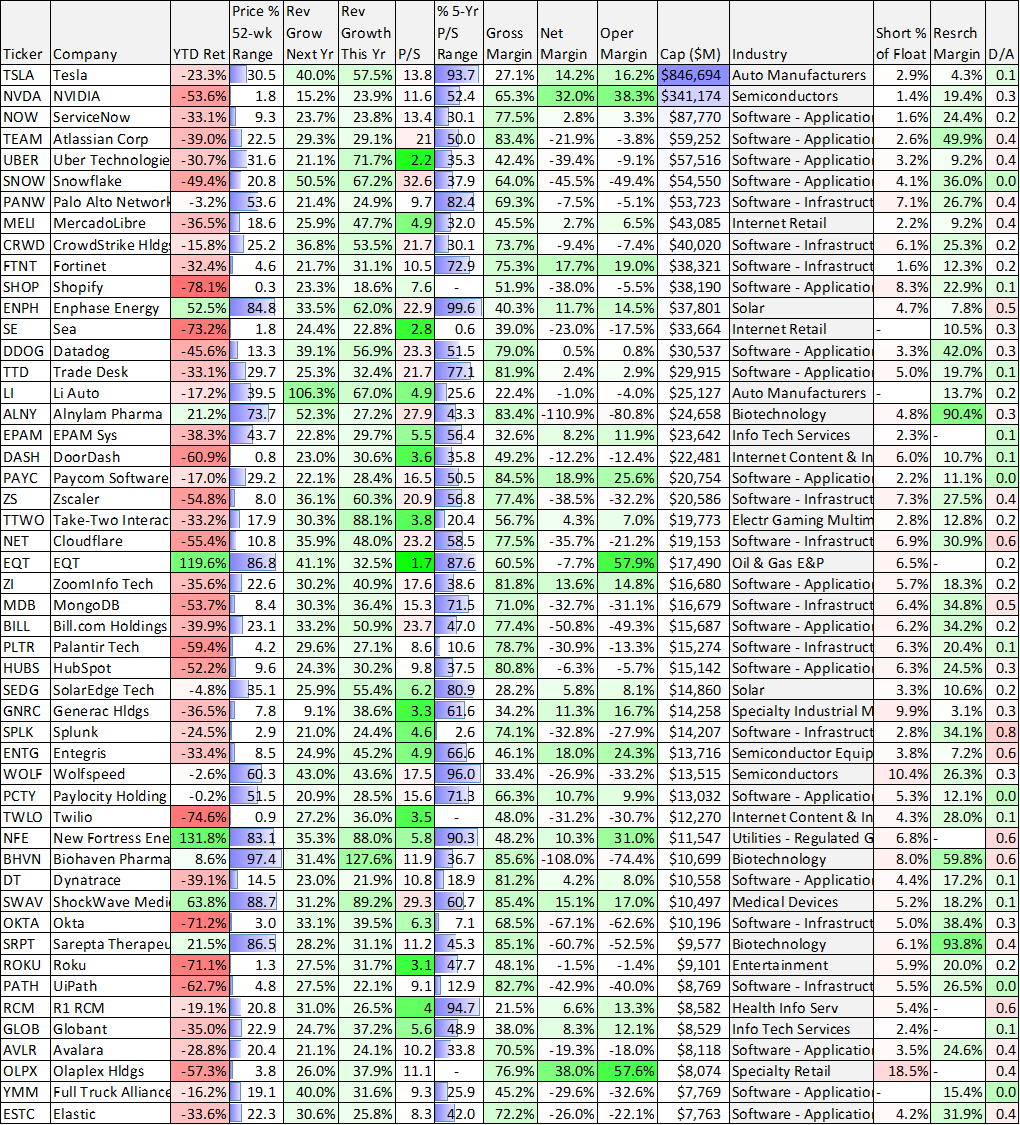

150 Top-Growth Stocks, Down Big

After the initial pandemic shock in 2020, certain high-growth stocks performed well. Extremely well. Bolstered by extraordinarily low interest rates and a new crowd of “work-from-homers” (with newfound time to “invest”) it seemed the sky was the limit. Until it wasn’t. Flash forward to now, the market has fallen sharply this year (especially high-growth stocks), and there is no short supply of reasons to stay bearish. Very bearish (as we will cover momentarily).

Before we get into the ranking and countdown, here is some high-level market information worth considering, starting with a list of 150 high-growth stocks (from across a variety of industries) that have fallen very hard this year. The table is sorted by market cap, and you likely see at least a few names that you are very familiar with.

A lot of conservative value-oriented investors take a lot of satisfaction seeing the sharp declines this year. They warned (often loudly) that valuations were absurdly high considering many of these pandemic darlings have never even generated a profit. What’s more, there are a lot of very compelling reasons to stay bearish on these stocks in the short term (such as high inflation, rising interest rates, lingering pandemic supply chain issues, a war in Europe and indications that corporate profit estimates are still too high based on the federal budget deficit). We will cover these near-term challenges in the following section, before getting into our long-term views and our top 10 ranking.

Challenging Macroeconomic Environment:

There is a wide variety of large macroeconomic challenges that give many investors a lot of reasons to stay very bearish on the market. For example, inflation is sky high (very bad for the economy), the fed keeps raising rates to fight inflation (but this has the side affect of slowing the economy), there are lingering pandemic supply chain issues, a terrible war in Europe and economists remain very pessimistic (as you can see in the following chart).

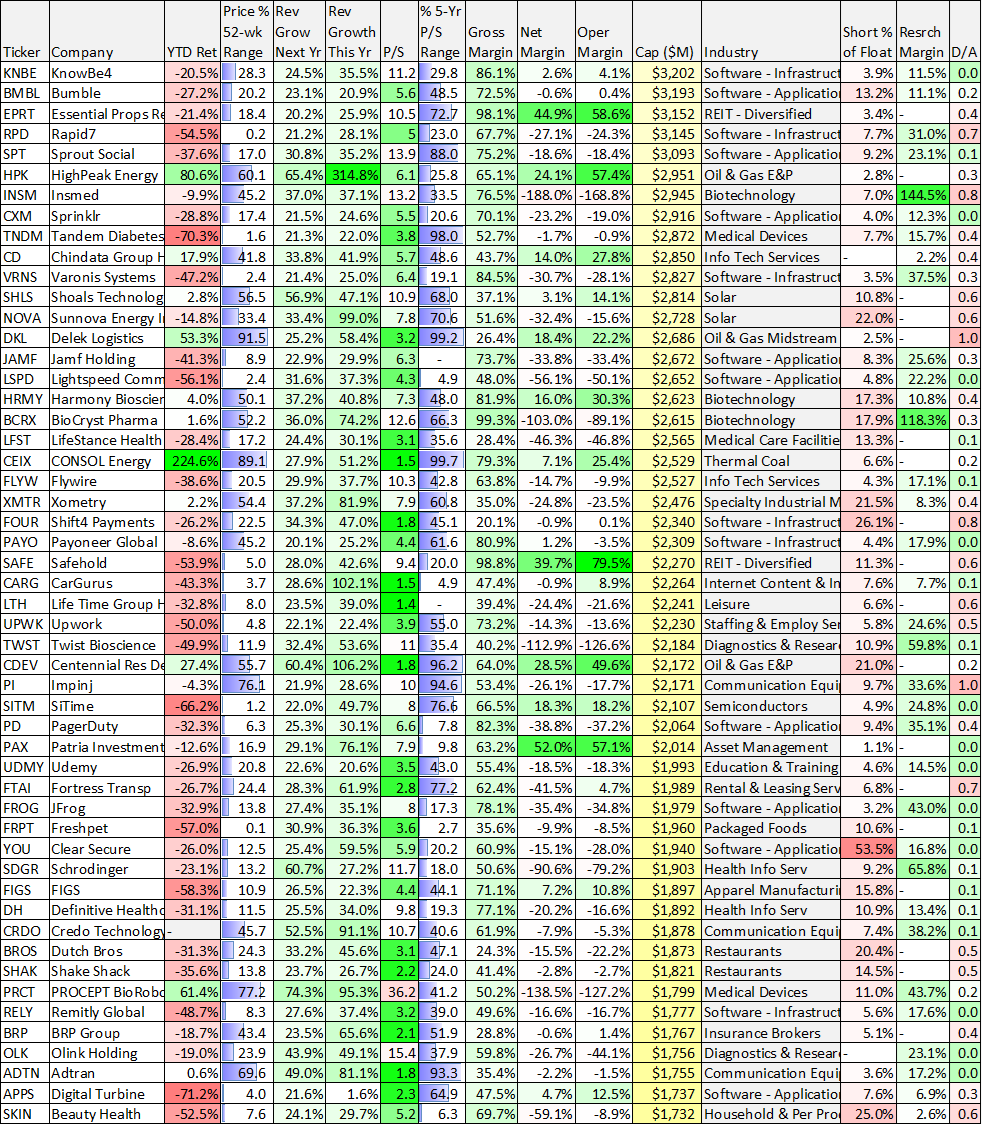

Further the federal budget deficit is about to create another big drag on the economy (for reference, the federal budget deficit is the difference between government revenues (i.e. taxes) and government spending). And while years of government deficit spending can create enormous long-term economic problems, the short-term deficit fluctuations can exacerbate near-term challenges.

Counterintuitive to some, when the economy is strong, the government should reduce spending (build a rainy-day fund), and when the economy is struggling, extra government spending can actually help end the funk. Unfortunately, the economy is struggling big time this year, yet the government has dramatically reduced deficit spending, as you can see in the following chart.

And according to GMO Capital’s Jeremy Grantham, this reduced government deficit may be about to cause corporate profit margins and earnings take a hit, due to the Kalecki equation (basically, reduced government deficit spending will cause a hit to corporate earnings, and this is not yet reflected in stock prices).

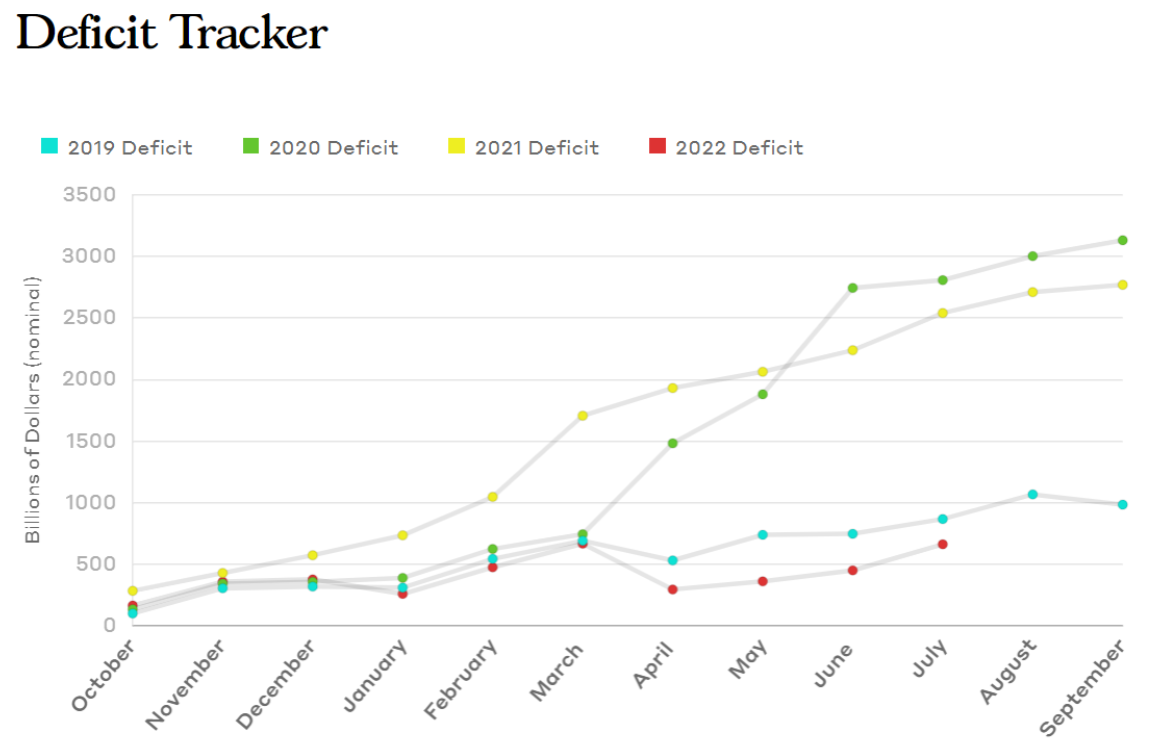

And of course we can make a strong case that growth stocks in particular (such as those in our earlier table) are still greatly overvalued (versus value stocks) based on historical levels, such as this chart (below).

Notice the divergence (in the chart above) becomes most pronounced around the time the US implemented and accelerated quantitative easing following the Great Financial Crisis (2008-2009) and the pandemic bubble (2020-2021), and right before the tech bubble bust (2000). Here is another chart on growth versus value, for your consideration.

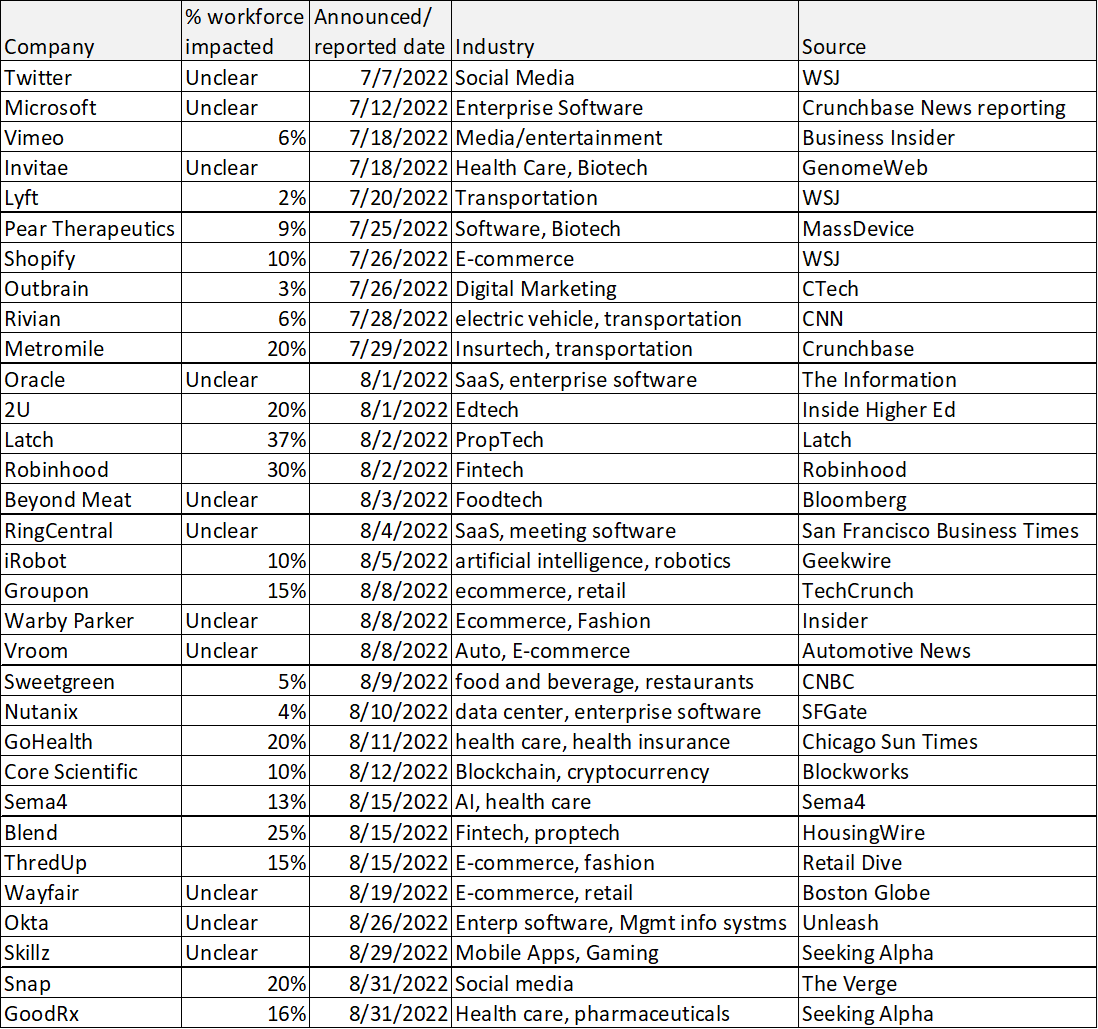

Further, a slew of recent layoff announcements by technology companies (see table below) suggest growth stocks in particular are just now finally bracing for the challenging markets ahead.

And with all the negative things going on in the market right now, it makes many investors want to stay as far away from stocks as possible. However, we are of the belief that over the long-term the market will get better. And from a contrarian standpoint, the best time to buy is usually when the market is down and everyone is very pessimistic (“buy when there is blood in the streets,” as the saying goes).

Of course things can still get worse, but trying to exactly bottom tick the bottom of the market is a fool’s errand (no one can do this exactly). However, the market is down a lot already, thereby making for a much more attractive entry point for disciplined long-term investors.

Top 10 Growth Stocks:

If you are a long-term investor, with the discipline, patience and ability (financial wherewithal) to hang on to your stocks through high volatility, then growth stocks are particularly attractive, from a long-term standpoint, right now. Over the long-term, stock market investing is one of the most powerful wealth generators know to man—thanks to long-term compound growth (the eighth wonder of the world). And with that backdrop in mind, and especially considering that growth stocks are now dramatically lower than they were, let’s get into our top 10 ranking, starting with number 10 and counting down to our top ideas.

10. Datadog (DDOG)

If you don’t know, Datadog is a performance monitoring and cloud security platform, and its shares are more than 50% below their 52-week high as the valuation has taken an extreme hit as the pandemic bubble bursts.

However, Datadog continues to benefit from three important growth stock characteristics (that will be a theme in this report), including very high revenue growth (see table below), a large Total Addressable Market or “TAM” (so it can keep growing) and the company is founder led (Current CEO Olivier Pomel cofounded the company along with CTO Alexis Lê-Quôc, in 2010).

You can see the high revenue growth trajectory above and the large TAM opportunity below.

Also important, Datadog was named a leader in the 2022 Gartner Magic Quadrant for Application Performance Monitoring and Observability (see below). Being an industry leader is another very good thing for continuing growth (especially when the industry is so large—thanks to the massive ongoing secular cloud transition and digital revolution).

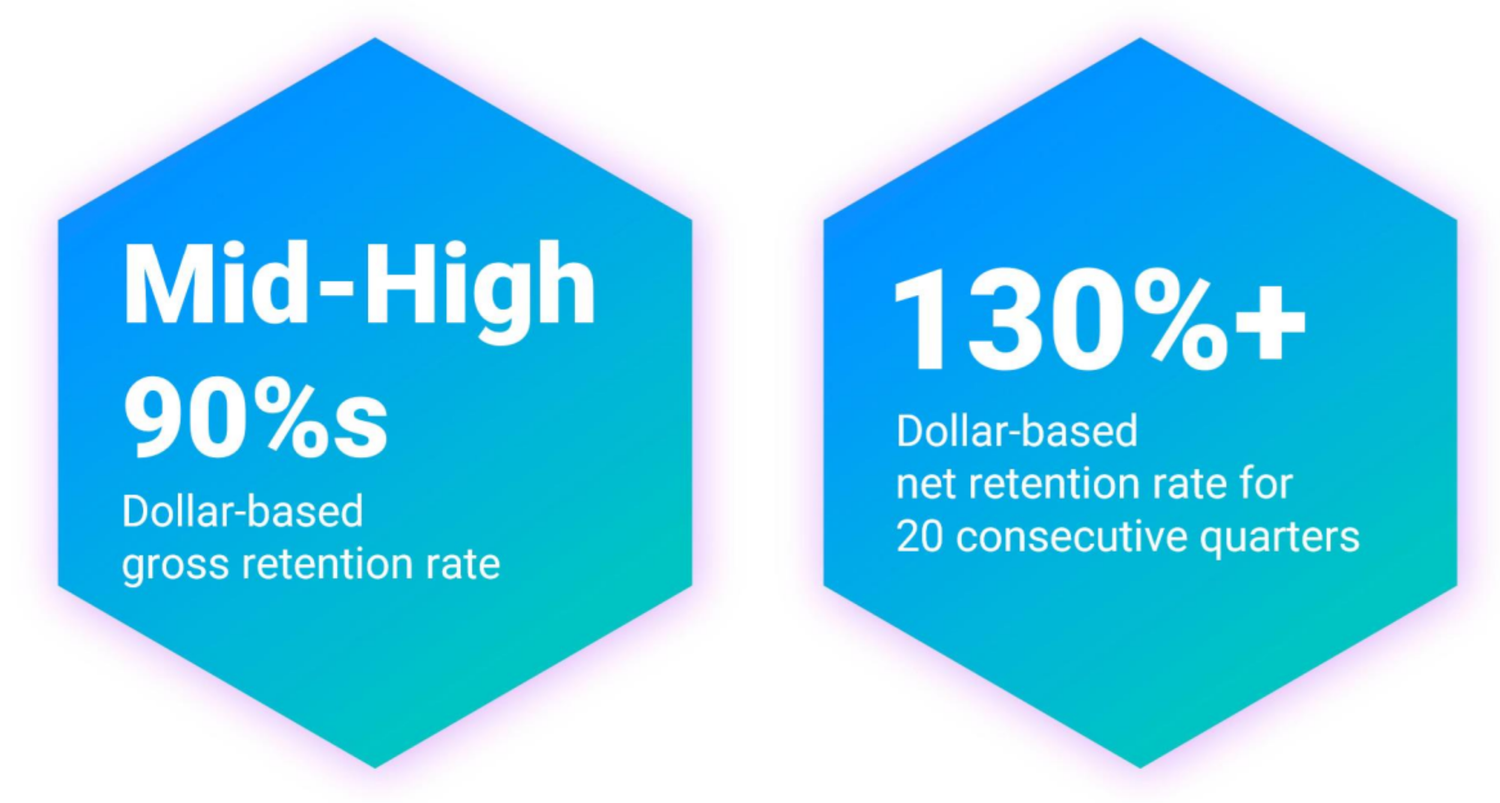

Also, Datadog has has high customer retention rates (also very good for continuing growth, see below).

And again, its valuation has come way down over the last year (for example, both its price and price-to-sales ratios are significantly below their 52-week highs, as you can see in our earlier table), but its high revenue growth remains intact as it moves closer to GAAP profitability in the near future (another very good thing). We recently wrote up Datadog in more detail, and members can view that note here (we don’t currently own shares of Datadog, but it is high on our watchlist).

9. Palantir (PLTR)

Palantir is basically a data-mining software company that has strangely generated a cult internet following since its September 2020 IPO, despite the fact that it has existed since 2003. Perhaps it’s the company’s secret government contracts that had so many investors mystified, or its expansion into the non-government Software-as-Service business at exactly the time when those types of stocks were being most hyped (because artificially low interest rates by the Fed dramatically magnified the present value of “possible” future earnings for those types of stocks) or maybe even its unusual name (it’s named after a mystical, all-powerful seeing stone in "Lord of the Rings"). Whatever the case may be, Palantir shares soared to very high valuations (for example, see how its current price-to-sales multiple compares to its 5-year (technically 2-year) range in our earlier table above).

Palantir Positives:

Before getting into the very negative company-specifics for Palantir below (and that’s in addition to the very challenging macroeconomic environment as described earlier), let’s first consider a few of the good things the company has going for it.

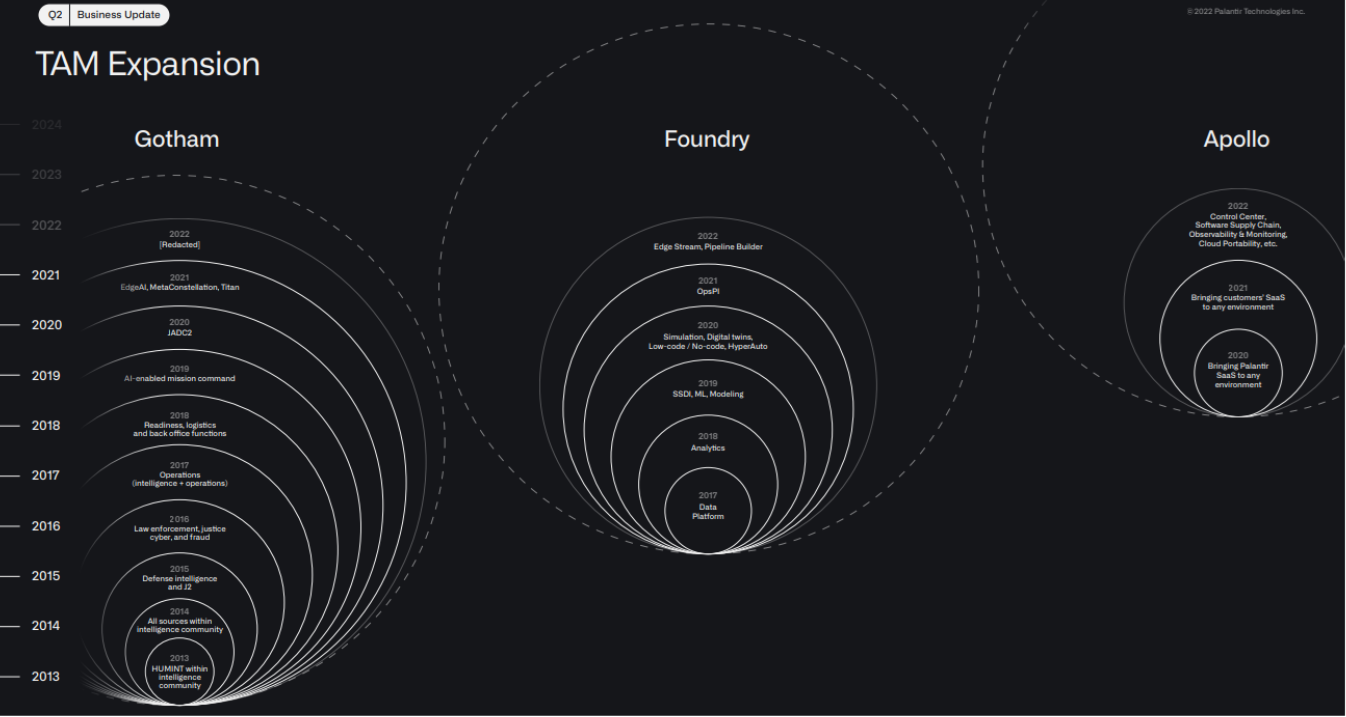

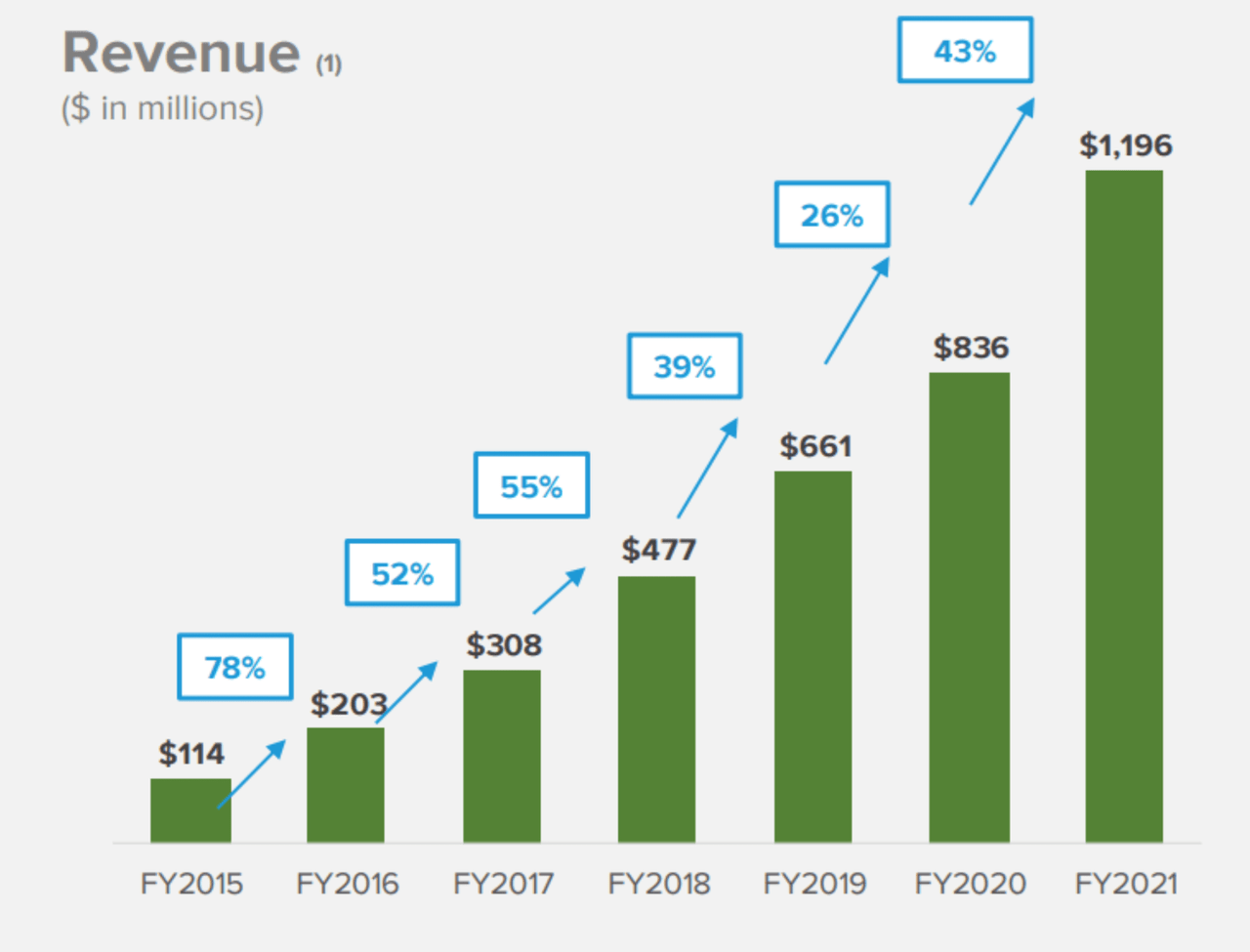

For starters, three big things many long-term growth investors look for in a stock are are a founder CEO (check: CEO Alex Karp cofounded Palantir), a very high revenue growth rate (check: Palantir revenue has been growing rapidly and is expected to keep growing rapidly, per our earlier table) and a very large Total Addressable Market (check: see the “TAM” graphic below from Palantir’s latest investor presentation).

Specifically, as you can see in the chart above, each of Palantir’s major businesses have continued to grow rapidly over time and continue to have large growth potential (dotted line). For reference:

Palantir Gotham is a software platform that enables users to identify patterns hidden deep within datasets, ranging from signals intelligence sources to reports from confidential informants, as well as facilitates the handoff between analysts and operational users, helping operators plan and execute real-world responses to threats that have been identified within the platform.

Palantir Foundry is a platform that transforms the ways organizations operate by creating a central operating system for their data; and allows individual users to integrate and analyze the data they need in one place.

Apollo is a software that enables customers to deploy their own software virtually in any environment.

To add to these positives, Palantir continues to grow its clients (which have a very high retention rate—Palantir ended Q2 2022 with net dollar retention rate of 119%—high retention is often typical for the very attractive Software-as-a Service (SaaS) business), very high gross margins (see our earlier table), strong innovation (as per its high research margin and strong expansion into non-government clients) and its losses are shrinking (it’s moving towards profitability). And of course, its valuation multiples are dramatically lower than they were and relatively attractive as compared to peers and as compared to its high revenue growth and large TAM.

Palantir Negatives:

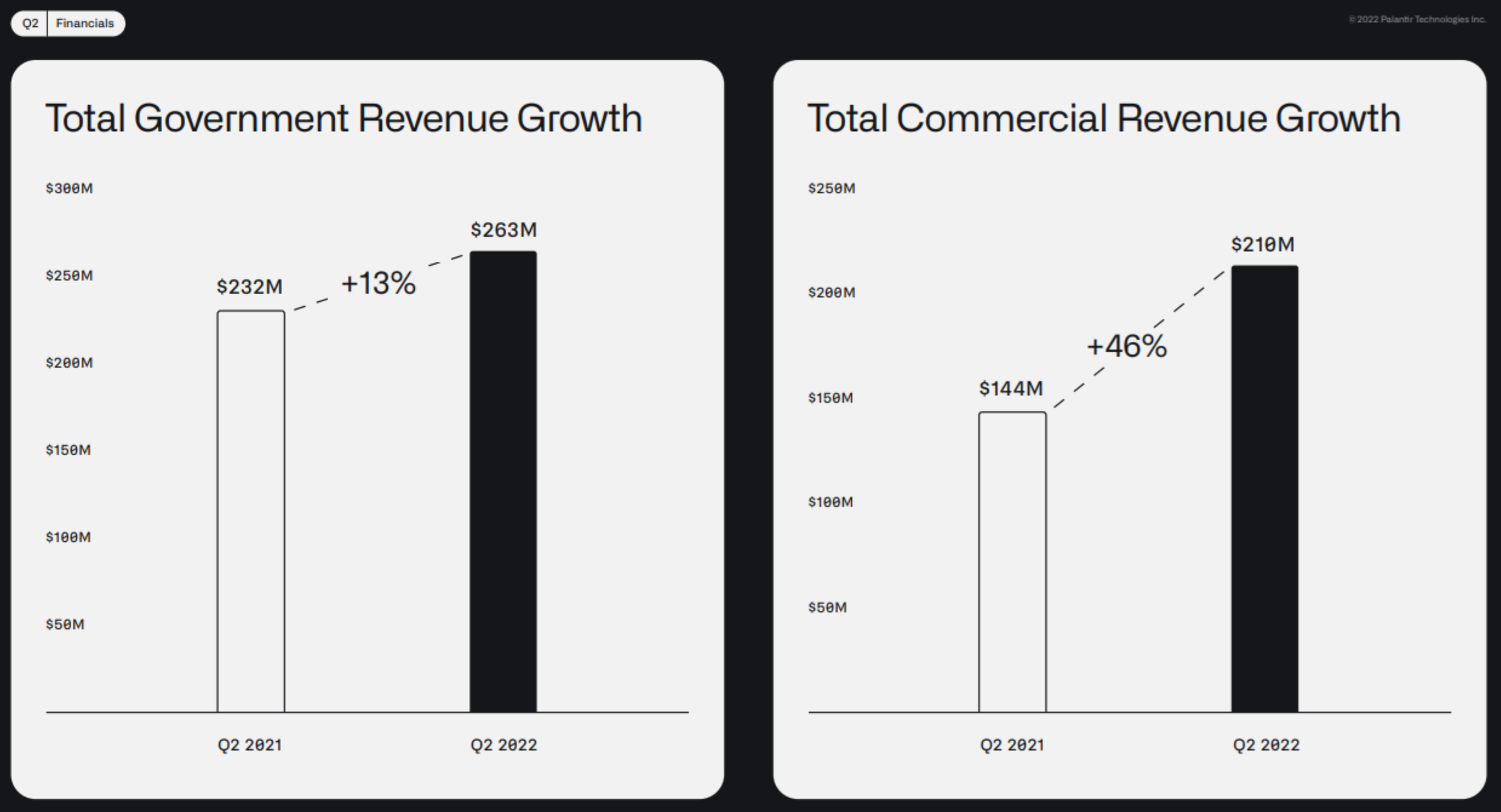

Of course there are a lot of negative things (challenges) Palantir currently faces. For example (and in addition to the negative macroeconomics described earlier), Palantir’s latest earnings announcement reveals that its government revenue (supposedly its “bread and butter”) is slowing.

According to a research note from Brad Zelnick at Deutsche Bank (Zelnick rates Palantir a “sell”):

"While we've always been more skeptical of Palantir's commercial opportunity, our thesis was rooted in what we saw as a uniquely strong position in Public Sector… Now with the Gov't business further decelerating off of easier compares and with diminished confidence/visibility ahead, we are left with very little to support our thesis."

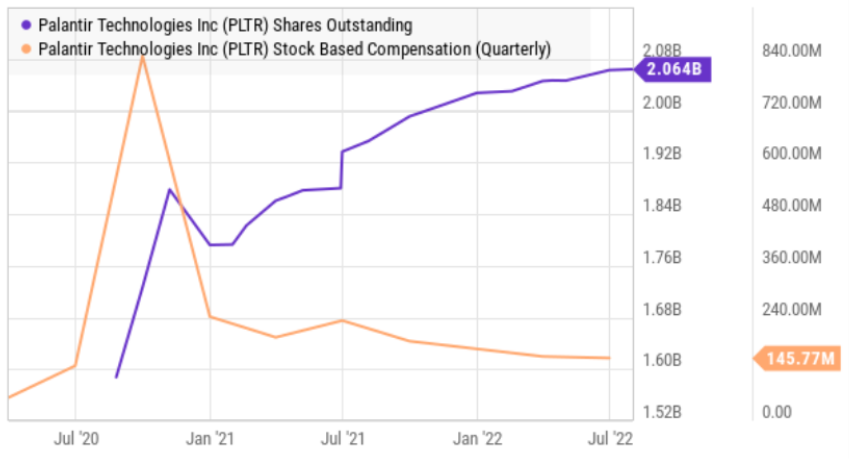

Another chronic qualm with Palantir has been its heavy stock based compensation and shareholder dilution.

Yet despite all the negatives Palantir has against it, it is still an attractive long-term investment considering the business has continued to grow rapidly while the market has sold off this year (thereby creating an increasingly attractive entry point) and when the current macroeconomic challenges slow (they will—eventually) Palantir has tons of long-term upside (for those with the discipline and patience to hold for the long-term—i.e. many years into the future).

We currently own a small position in Palantir in our prudently concentrated Disciplined Growth Portfolio.

8. Digital Turbine (APPS)

Digital Turbine thinks of itself as a “one-stop-shop growth & monetization platform.” It basically works with wireless carriers and device original equipment manufacturers (“OEMs”) to pre-install apps on new devices. And it has been expanding its offerings through acquisitions, including Appreciate, Fyber and AdColony. A few things make Digital Turbine special: (1) its business model gives it access to unique data that is highly valuable to advertisers (and the total addressable market opportunity (“TAM”) is massive, (2) it’s actually a profitable business (unlike a lot of other growth stocks in our earlier table), and (3) the valuation has come down dramatically making it interesting as a standalone investment and as a potential acquisition target. We recently wrote up Digital Turbine in more detail, and members can access that note here. We currently own a small position in Digital Turbine in our prudently concentrated Disciplined Growth Portfolio.

7. The Trade Desk (TTD)

The Trade Desk is another high-growth stock that has recently sold off very hard (it’s down more than 30% this year).

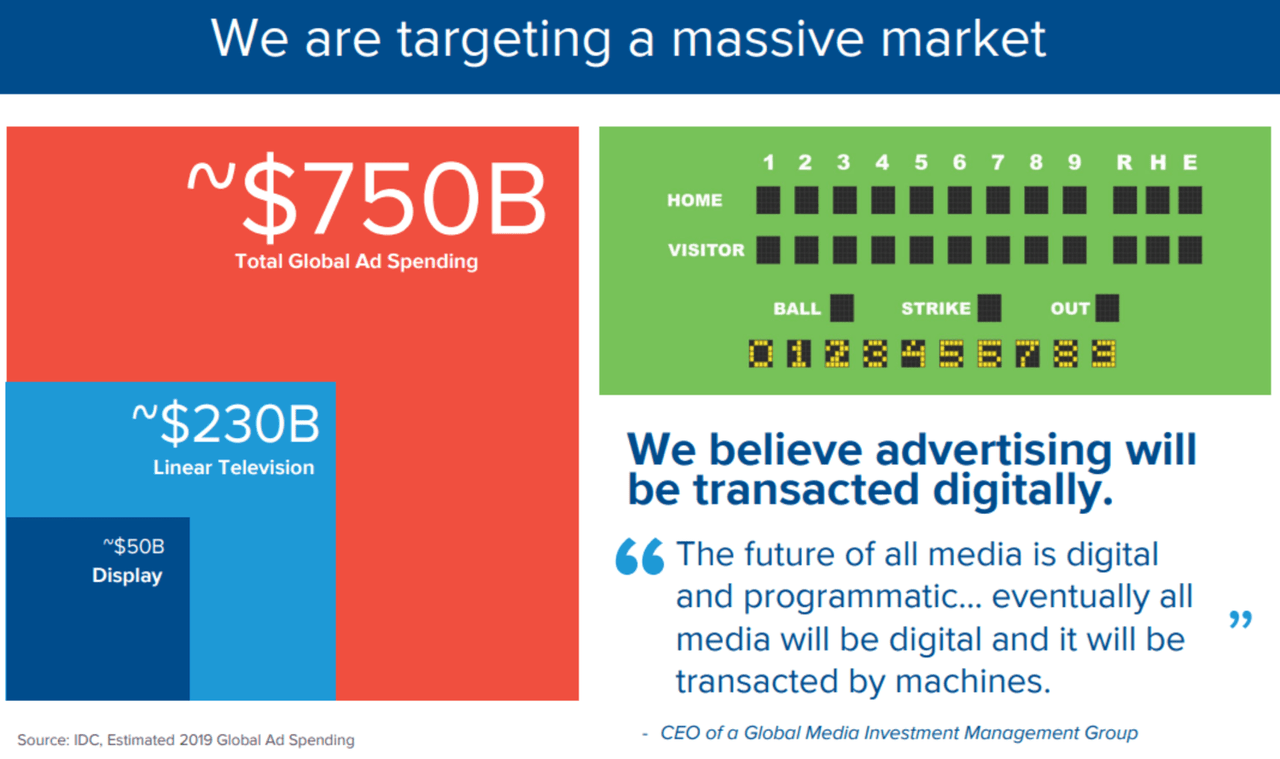

And like other growth stocks we have highlighted in this report, it is an attractive founder-led business (Jeff Green is co-founder and current CEO), with very high revenue growth (see graphic above), and a very large TAM (see the graphic below).

If you don’t know, The Trade Desk is basically a self-service omni-channel advertising platform that allows ad buyers to pick from over 500 billion digital ad opportunities a day (including targeted ads across connected TV, mobile, video, audio, display, social, and native). We recently wrote about The Trade Desk in detail last month (where we correctly predicted that it would resume its steep share price declines in the short term), however over the long-term The Trade Desk has a ton of upside and the shares have recently sold off thereby making an increasingly attractive entry point for disciplined long-term investors. We currently own shares of The Trade Desk in our prudently concentrated Disciplined Growth Portfolio.

6. Paylocity (PCTY)

Paylocity is an attractive payroll and human-capital-management Software-as-a-Service (“SaaS”) company. Its comprehensive product suite delivers a unified platform for professionals to make strategic decisions in the areas of benefits, core HR, payroll, talent, and workforce management, while cultivating a modern workplace and improving employee engagement.

We first purchased shares of Paylocity in our Disciplined Growth Portfolio in 2015 (when the share price was under $30 and the market cap was around $1.4 billion). It just recently another quarter of strong earnings, and the shares now trade at around $260 (and the market cap is over $14 billion) (we still own shares). What’s more, we continue to like its exceptionally strong growth trajectory going forward (the shares have a lot more upside ahead—they’re still well below their 52-week high. We recently wrote up Paylocity in more detail for members, and you can access that report here.

The Top 5:

Our top 5 growth stocks are reserved for members only, and they can be accessed here. The top 5 includes several technology sector stocks, as well as an industrial sector stock and a consumer staples stock. They all have tremendous compound growth opportunities, and we currently own all of them within our prudently concentrated Disciplined Growth Portfolio.

Conclusion:

Long-term growth investing takes discipline and patience. For example, you have to have a long enough expected holding period to be comfortable continuing to hold when shares sell off hard (like the examples in this report have recently) because you realize the long-term growth and investment thesis remains intact (as Warren Buffett says, if you’re not comfortable owning a stock if the market shuts down for 10 years, then don’t even think about owning it for 10 seconds). In fact, this year’s very hard sell off has made for some very attractive long-term entry points.

Of course things can still get worse before the get better, but in the long-term we believe the market will eventually get better and the companies covered in this report will continue to be high-growth leaders that can compound their growth (and compound the value of your account) dramatically in the years ahead.

For reference, you can view all of the current holdings in our long-term Disciplined Growth Portfolio here. While many of holdings are down this year as the market has sold off, some are actually up a lot, and we believe all of them have a lot more long-term compound growth in the years ahead, and collectively (from a prudently diversified and concentrated portfolio standpoint) the holdings comprise a very attractive long-term risk-reward profile. We are very excited about the long-term opportunities, and at some point down the road, we’ll be looking back at 2022 and thinking—wow—that was a great long-term buying opportunity.

Note: If you are not entirely growth focused, and prefer to consider some less-volatile income securities too, the holdings for our Income Equity Portfolio are available here. Every investor should invest according to their own individual needs and situation.