Chip stocks have sold off dramatically this year, and it’s not just because the fed’s draconian rate hikes are stymying future growth. This report focuses on Intel (INTC), including its last-ditch highly-political foray into foundry in an effort to get in on the digital revolution growth opportunities that are increasingly going to more innovative peers like Nvidia (NVDA) and Advanced Micro Devices (AMD) and then also to downstream supply-chain foundry-king Taiwan Semiconductor (who announced fantastic earnings on Thursday, by the way) in what appears to be an increasing national security risk. However, as less experienced “growth investors” are increasingly aware of this year, valuation isn’t just about revenue growth rates, and long-term profit margins matter, a metric where Intel is every bit as competitive as peers, even if the shares aren’t being given proper credit. We conclude with our opinion on investing.

About Intel:

Intel is the leader in PC and server chips. However, its growth rate has diminished dramatically in recent years as it has failed to keep up with the ongoing digital revolution, particularly with regards to the ever growing demands of smart phones and data centers. Nonetheless, the business continues to maintain high margins and healthy profits, as you can see in the following chart comparing Intel, Nvidia, AMD and Micron (MU).

Intel has been able to grow over the years through a large R&D budget and timely acquisitions, but as you can see in the graph above—its future revenue growth rate looks bleak as compared to other chip stocks, particularly AMD and Nvidia. In particular, Nvidia and AMD continue to lead through innovation, while Intel’s claim to fame is largely its legacy stronghold on PC and server markets, combined with its foundry Hail Mary pass whereby Intel is basically hoping the US government mandates more domestic chip manufacturing through the CHIPS for America Act which could dramatically boost its growing foray into low cost foundry manufacturing (more on this later). And in case you don’t know, a foundry is:

A semiconductor manufacturer that makes chips for other companies. Also called "fabs," semiconductor foundries make most of the chips in the world for hundreds of "fabless" companies that design but do not manufacture, including some of the largest and well-known tech leaders such as Qualcomm, NVIDIA and Apple. However, a large company that designs and makes its own chips may sell excess manufacturing capacity and function as a foundry from time to time.

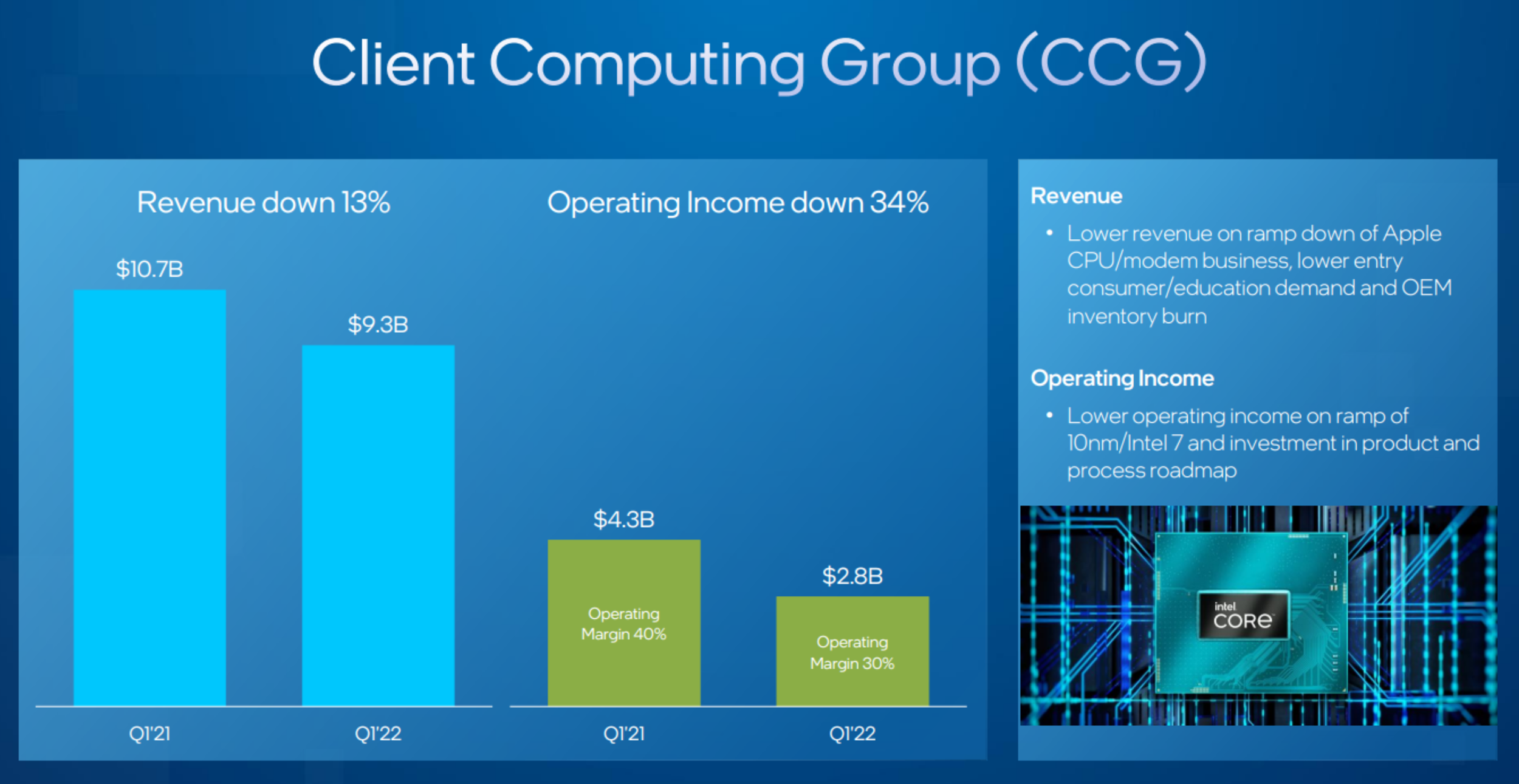

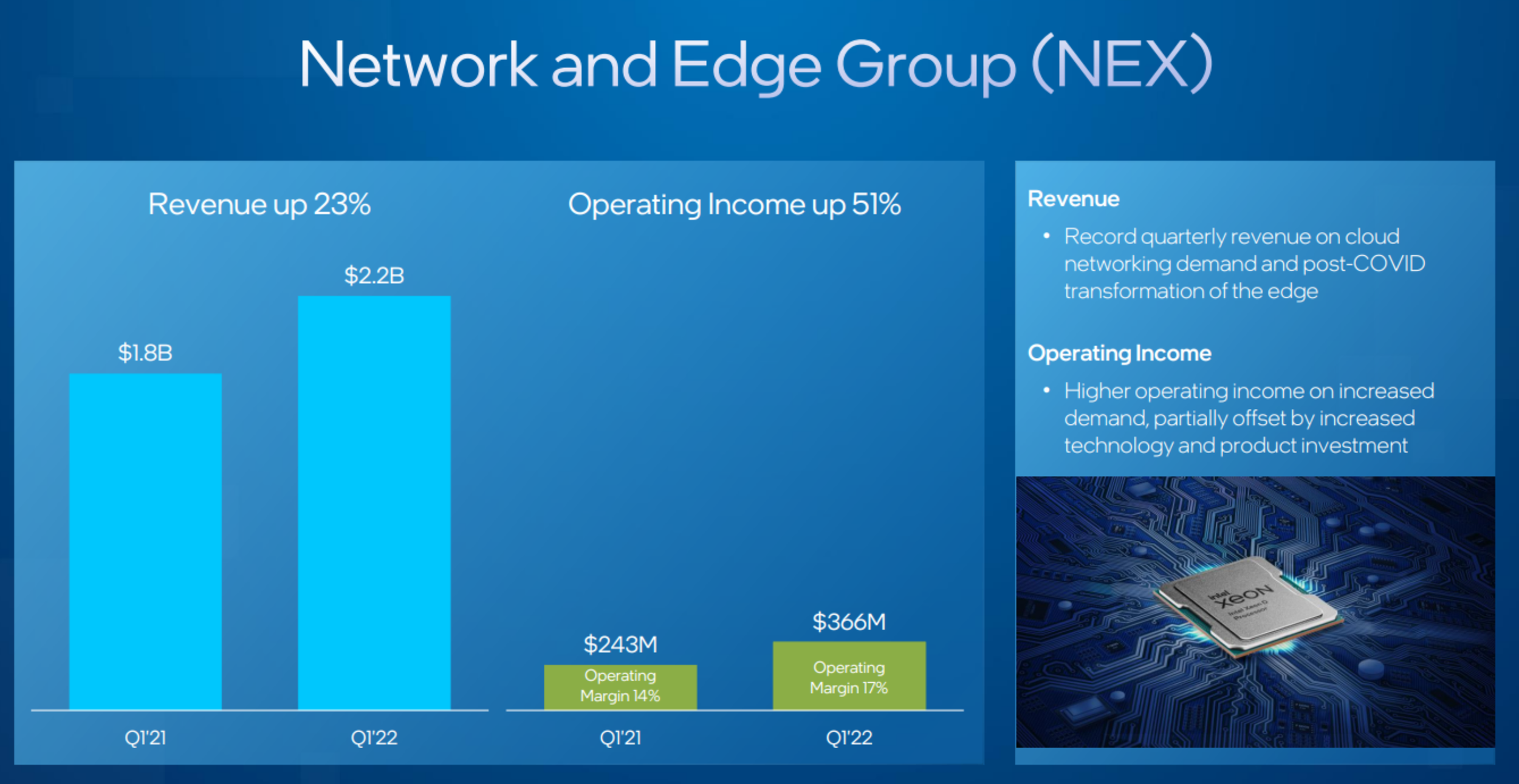

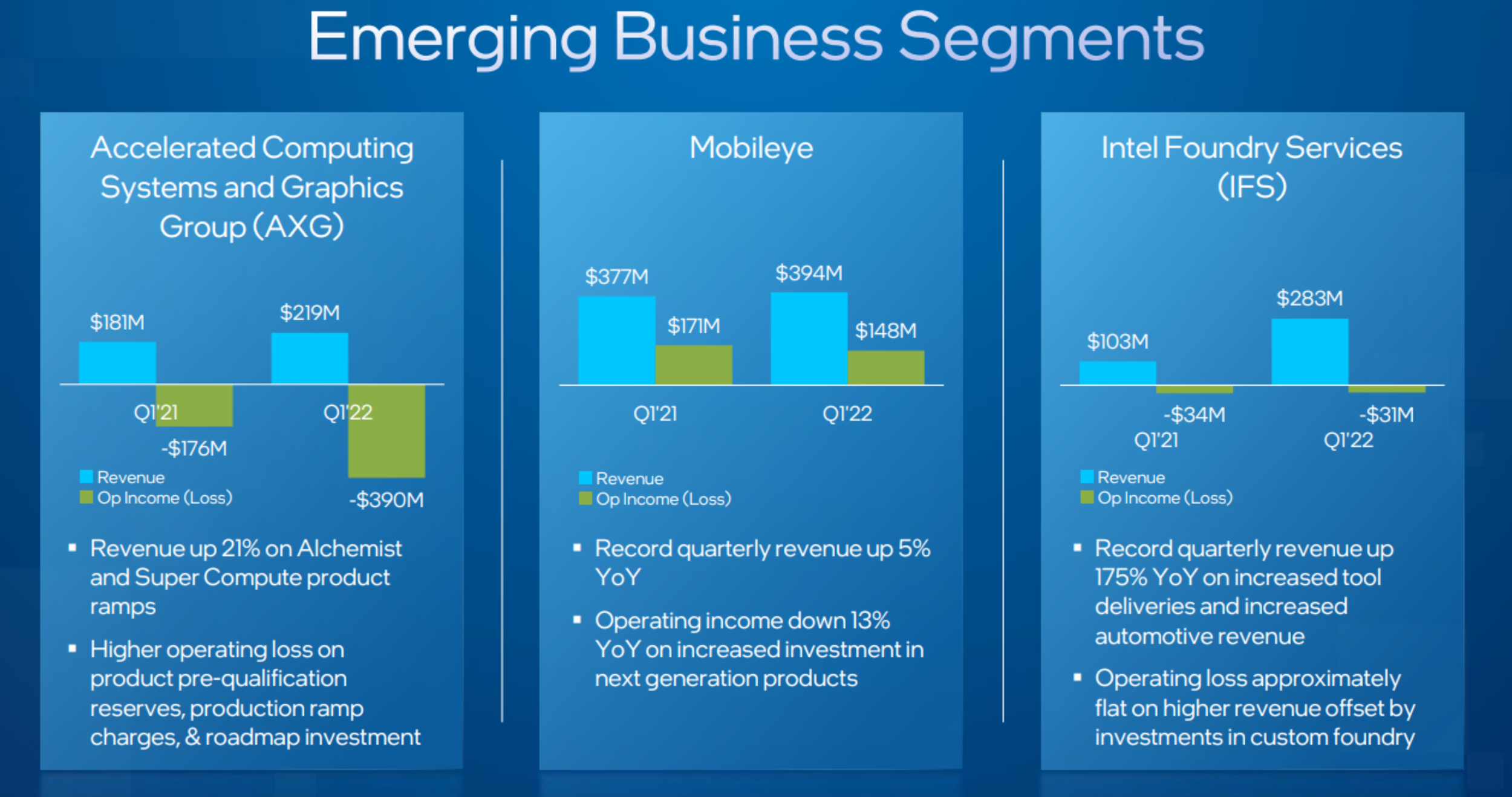

Just to give you some perspective on the size and scope of Intel’s business segments, here is a look at the company’s growth trajectory by business segment (below). And as you can see, the legacy Client Computing Group is the largest but slowing (this is a secular trend), and the Emerging Business Segments Group shows just how tiny Intel’s foundry business is so far.

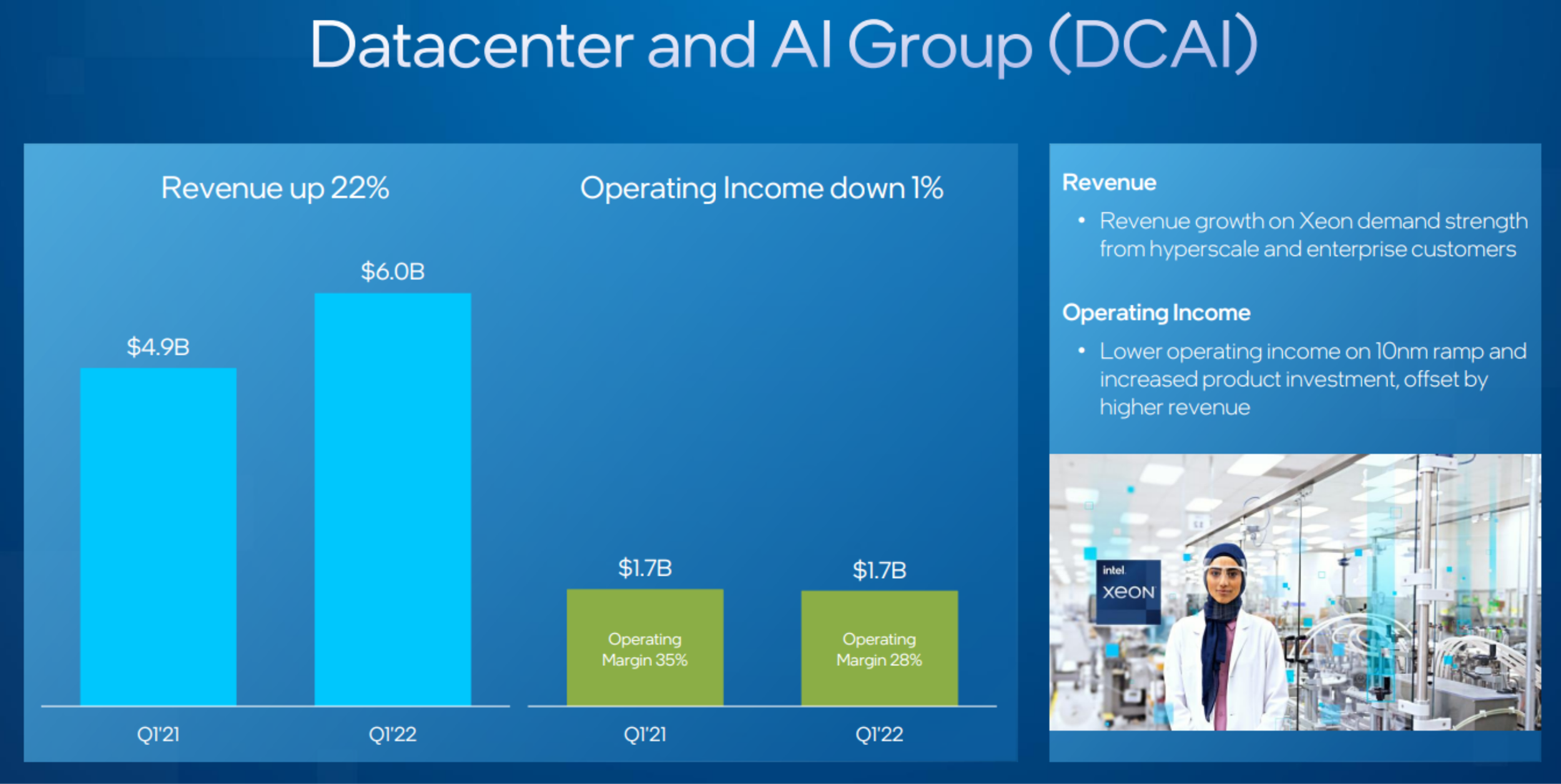

Worth mentioning, Intel is posting strong growth in its data center and AI unit, but this is not Intel’s largest segment, and the growth numbers are novice compared to Nvidia and AMD.

Intel’s Foray Into Foundry:

If you’ve tried to buy or sell a car in the last year, you’ve likely been shocked by the elevated prices, which are the direct result of chip shortages. The chip shortages are caused by pandemic-related supply chain issues, but they also reveal a significant security risk for the US, considering chips are a necessity for so much of the economy (including defense), and because chips are increasingly produced outside the US and thereby out of our control.

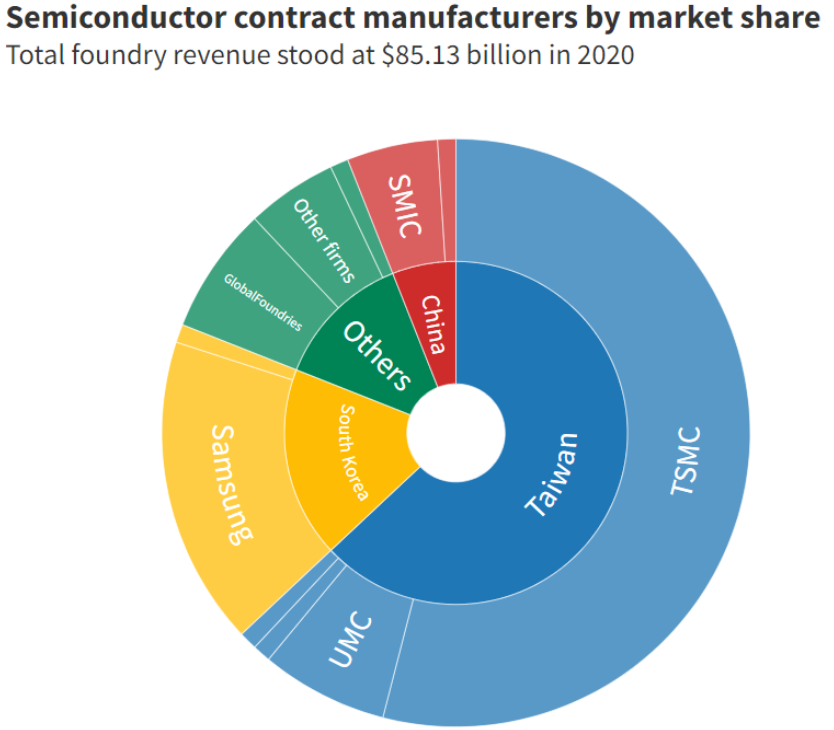

The following graphic shows recent chip manufacturing by geography (inner circle) and company (outer circle), and as you can see—the US is at the mercy of other countries.

source: CNBC

This risk has been highlighted by the pandemic-related chip shortages, and it has resulted in the drafting (but not passage) of legislation to address it. Specifically, the CHIPS for America Act would provide income tax credits and establish a $52 billion+ trust fund to “support U.S. semiconductor manufacturing, research and development, and supply chain security.”

And the CHIPS for America Act has recently regained publicity and impetus from a newly released letter from over 100 frustrated chip-maker CEOs, including Google (GOOGL), Intel, AMD, Amazon (AMZN) and others.

And the passage of the CHIPS for America Act would be particularly helpful to Intel considering it gains its competitive advantage versus peers based on its cost advantages is designing and manufacturing chips. According to Morningstar sector strategist, Abhinav Davuluri:

“We believe Intel’s wide moat emanates from its superior cost advantages realized in the design and manufacturing of its cutting-edge microprocessors and intangible assets related to its x86 instruction set architecture license and chip design expertise. While the firm has endured significant delays in deploying its latest 10-nanometer process technology, which has allowed foundry Taiwan Semiconductor Manufacturing (TSMC) to leapfrog Intel and AMD to become more competitive via TSMC’s 7-nm process, Intel’s manufacturing advantage over virtually every other chip designer and manufacturer is still intact and durable.”

And even though foundry is only a very small percentage of Intel’s business now, it creates a significant opportunity (albeit highly uncertain) for growth if the CHIPS for America Act is passed, considering the company has been working aggressively to expand its foundry capabilities based on the potential for future business. According to Intel CEO, Pat Gelsinger, on the last earnings call:

“Following our announcements in Arizona, New Mexico and Ohio, we recently announced a series of investments in Europe, spanning our existing operations as well as our new investments in France and Germany, the Silicon Junction. These investments position Intel to meet the future growth and represent a significant step toward our moonshot goal of having half the world’s semiconductor manufacturing located in the U.S. and Europe.”

And as a reminder of just just how lofty that goal is, see our earlier chart on recent/current chip-manufacturing geographies (i.e. the US and Europe are currently very small).

Of course, why wouldn’t Intel and other chip companies want the CHIPS for America Act passed (it’s basically free money for them). Worth mentioning, signatures from Apple’s (AAPL) Tim Cook and Nvidia’s Jensen Huang were noticeably missing from the letter mentioned earlier, in perhaps a hat tip to just how challenging foundry chip manufacturing really is (i.e. throwing money and tax breaks at US companies won’t magically elevate their technology operations to make them competitive with Taiwan Semiconductor, for example).

However, from Intel’s standpoint (as the US leader in designing and manufacturing chips), the CHIPS for America Act could be a windfall. And the success of Intel’s entire foundry foray hinges largely on recent supply chain issues pressuring Congress to act.

Valuation:

Our course, when valuing a business, high growth is not the end goal—high earnings is. And even in the absence of high growth, Intel already does have healthy high earnings (from its existing businesses). Let’s have a look at some Intel valuation metrics to get an idea if the current high earnings are being appropriately valued by the market, or if the fearmongering “no-growth” narrative has caused the shares to trade too cheaply (i.e. is there a “buy low” opportunity here?).

Here is another look at our earlier valuation graph (below), and as you can see, Intel trades at a lower valuation multiple than peers in terms of price-to-earnings ratio and price-to-sales ratio. Specifically, Intel trades at around 6.2 times earnings (very low) and 10.2 times forward earnings (higher because earnings growth is temporarily bumpy), and it trades at only around 2 times sales. These are not only low compared to peers, but low by Intel’s historical standards (especially considering the company will likely return to some revenue and earnings growth in the longer-term, as per the market cycle and the company’s competitive advantages).

And taking into consideration Intel’s low-cost advantages, strong earnings and projected return to some growth, the current valuation is compelling. For example, if the forward price-to-earnings multiple were to expand to only 15 times (not unreasonable by historical standards, and still quite conservative) the shares have nearly 50% upside from here (for reference, Intel shares are currently about 35% off their 52-week high).

Intel’s Dividend:

You may have noticed that Intel’s share price has fallen less than the competitors listed above. Part of the reason for that is because Intel’s is the only one that pays a significant dividend. In fact, Intel currently offers a 3.8% dividend yield, which has mathematically increased as the shares have fallen, and it’s higher than the historical norm (perhaps a signaling indication from management that they believe the long-term share price should be higher).

Another indication of strength, the dividend has been paid for 29 years in a row, and it has grown in each of the last eight. Plus the company generates plenty of free cash flow to cover the dividend (i.e. dividend safety) and research & development (a good sign). Further, Intel has a higher credit rating (“A+” per Fitch) than peer Nvidia (“A”) and AMD (“A-” per S&P).

Intel Versus Nvidia and AMD:

We’ve already seen the stark differences in valuation multiples and growth expectations for these companies, but it is worth briefly considering the businesses.

For starters, Nvidia and AMD garner a lot of attention for their high growth rates. Their chips are correctly seen as more innovative and more cutting edge, and this will enable them to remain at the forefront of the ongoing massive digital revolution which includes the cloud (data centers) but also smart cars, virtual reality, artificial intelligence, smart homes, smart cities and virtually anything else that uses data. The total addressable market opportunity is truly massive.

In particular, for example, Nvidia is basically eating Intel’s lunch in the data center space, as Nvidia GPU chips are better suited for processing work loads faster, and this is not likely a trend that will abate soon. Also, AMD’s latest EPYC CPU chips have caught up with Intel thereby creating new competitive pressures. The cutting edge innovation of Nvidia and AMD have created dramatic headwinds for Intel in capturing newly available digital revolution market share. However, it’s also worth noting that AMD and Nvidia already trade at dramatically higher valuations than Intel.

Conclusions:

The semiconductor industry isn’t a fad. It isn’t going away. It’s going to continuing growing for a long time and there are massive opportunities for industry leaders to benefit. The question for investors is “if and where” are you going to place your investment dollars.

If you like steady higher income, Intel is currently attractive for its big dividend and lower share price (as compared to its powerful earnings). We don’t currently own shares of Intel, but we are considering adding it to our Income Equity portfolio in the near future (especially considering the foundry initiative ads an element of significant upside depending on the longer-term regulatory direction of the US government to address supply chain issues and the now conspicuous national security threat).

And if you are looking for a more volatile opportunity (more growth but without the bigger dividend), we like Nvidia. As we explained in our recent midday report (25 Top Chip Stocks Down Big):

“Nvidia and Intel have among the highest net profit margins among top chip stocks, but they also have widely different growth trajectories and valuations. And from a PEG ratio standpoint, the valuation gap narrows.”

We sold our Nvidia shares last year at around $270, but recently added them back to our Disciplined Growth Portfolio at a dramatically lower price.

At the end of the day, disciplined, goal-focused, long-term investing is a winning strategy. Markets have been ugly this year (especially for Intel, Nvidia and AMD), and that is often a much better time to buy.