Intel reminds me of IBM. It was a once great tech stock that completely missed a massive secular industry change, and is now on track to die slowly over time (unless it can find a good way to reinvent itself, which the company’s leadership team seems committed to not doing). The good news is, Intel is committed to its larger-than-average dividend. The bad news is, much like IBM over the last decade, we expect the big dividend to be mostly offset by steady long-term share price weakness. There are better investment opportunities than Intel, including the three specific chip stock opportunities we review in this report.

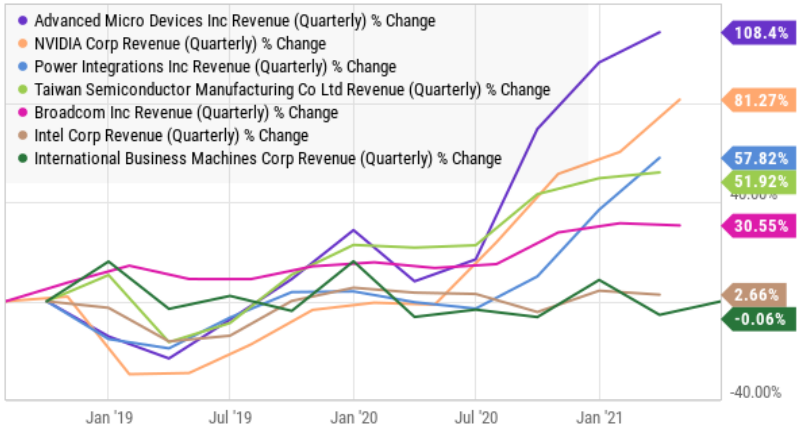

source: YCharts

Intel Missed the Boat

If you don’t know, Intel designs and manufactures products and technologies in the semiconductor (or “chip”) industry. And in our view, it’s a company that is completely missing the boat. Specifically, rather than being an innovator in the rapidly evolving semiconductor industry (forecast to grow 19.7% in 2021 and 8.8% in 2022), Intel basically rested on its laurels and is now paying the price, much like IBM (mentioned above). Specifically, Intel (and IBM) continues to suffer from stagnating revenue growth while the competition capitalizes on the digital transformation and Internet of Things (“IoT”)—in many cases posting eye-popping revenue growth numbers, as you can see in the chart above and the table below.

source: StockRover, data as of 7/22/21

Moreover, as you can see in the above table, Intel’s expected revenue growth numbers are very weak, and the company’s Thursday evening earnings release was not encouraging. Specifically, don’t be misled by Intel’s attempted positive spin on its 2% year-over-year revenue growth number because it includes the temporary bump in notebook and desktop demand due to students and employees working from home during the pandemic.

source: Intel Q2 Presentation

Furthermore, Intel is now forecasting only 1% revenue growth for 2021, at a time when many of its peers and the overall industry are achieving very big gains. Further still, Intel expects gross margins and earnings per share to get worse—a trend we expect to continue (more on this in a moment).

source: Intel Q2 Presentation

Foundry is not a good long-term solution

Compounding Intel’s festering long-term financial problems (i.e. stagnating/declining revenue growth), management has elected to pursue short-term opportunities (i.e. foundry) instead of addressing the company’s fundamental problems (i.e. abysmal growth because they’re not pursuing changing industry opportunities as aggressively as others).

A semiconductor foundry is a business that fabricates the designs of other companies, and it is a business direction Intel announced last quarter that it would increasingly pursue. The problem with this strategy is that it is short-term, lower margin and will result in Intel falling further behind. Specifically, it’s short-term because Intel is trying to address industry-wide chip shortages, which are expected to subside within less than 2-years. It’s lower margin, simply because it’s a strategy with little innovation therefore prices are pressured lower by competition. And it will cause Intel to fall further behind because they will continue to miss out on opportunities to capture the massive secular growth resulting from the Internet of Things and the Digital Transformation, which both still have a very long runway for growth (which Intel’s competition continues to capitalize on). Basically, Intel’s revenue growth will struggle mightily in the years ahead.

Management is committed to Intel’s big dividend (not a good thing!)

A you can see in our earlier table, Intel has one of the biggest dividends in the industry. And the company has plenty of cash flow (from high operating margins) to keep supporting the dividend. However, in Intel’s case, this is not a good thing. Specifically, much of Intel’s competition pays no dividends because they are focusing all their capital on capturing the massively attractive industry opportunities. On the other hand, Intel’s commitment to the dividend is a white flag from management that they don’t believe they have what it takes to capitalize on the industry growth opportunities.

As a counter example, Advanced Micro Devices’ (AMD) Lisa Su was promoted to CEO in 2014, and by 2015 she had boldly shifted the company’s long-term strategy to focus on “developing high-performance computing and graphics technologies for three growth areas: gaming, datacenter, and ‘immersive platforms’ markets.” And as a result, AMD’s revenue growth went from negative to extremely positive (and AMD still doesn’t pay a dividend). Lisa Su is a rock star, and unlike Intel she is not waiving the white flag of surrender. She is capitalizing big time on the massive industry opportunities.

Further, Intel management’s acknowledgement that “going forward, we expect to have lower stock repurchases” is another bad sign. Specifically, it means they believe the shares are fairly priced at best, and dramatically overpriced at worst. If Intel thought the shares were underpriced then they’d be buying them back more aggressively instead of reducing share repurchases.

Overall, we expect Intel’s strong dividend to attract yield chasers. And unfortunately, if Intel’s share price keeps falling, the dividend yield will mathematically continue to rise (and attract more yield chasers). For a little perspective, many income-focused yield chasers continue to pile into IBM for its powerful, long-term, growing dividend, but a look at its total returns (dividends plus share price appreciation) shows very poor long-term investment results—an ugly path upon which Intel may be embarking.

Selling Income-Generating Intel Put Options

A strategy we often write about for our members is selling out-of-the-money, income-generating, put options on dividend stocks. And in Intel’s case, this strategy is very tempting—especially on share price dips. Specifically, we generally like to go about 5% to 8% out-of-the-money on put sales with about 1-month to maturity—especially after a near-term price decline (because that’s usually when the premium income is higher).

image source: TD Ameritrade

The above table (grabbed from TD Ameritrade, afterhours Thursday) shows the reported premium income available for such a strategy. However, as we always remind readers, these premium amounts are moving constantly, and the prices will have moved significantly by the time the market opened on Friday (as the shares reacted to Thursday evening’s earnings announcement news).

Importantly, we generally only implement this strategy on stocks we’d be comfortable owning for the long-term (if the shares got put to us), and Intel doesn’t exactly meet this criteria. Members have access to many more examples of these types of trades, and readers can view a free example here.

Three Chip Stocks We Like More Than Intel

1. Qualcomm (QCOM)

If you like dividends, growth and value, Qualcomm is a more attractive long-term investment opportunity than Intel. These share are down this year, yet margins remain very high, growth remains very strong, and the valuation remains quite compelling (you can view all these metrics in our earlier table near the start of this report). And even though Qualcomm’s dividend yield is only 1.9%, the dividend has been increased 18 years in a row, and the “yield on cost” is truly impressive (the power of dividend growth is underrated).

In May, we released a detailed report on Qualcomm for our members, and here was our important takeaway from that report:

Overall, Qualcomm is attractive. The shares have recently sold-off as investors have concerns over chip shortages and customer concentration (i.e. Apple is attempting to develop its own chips). In our view, the fears are overblown, and investors would be better served to take the long view. Specifically, Qualcomm is an industry leader with a high growth rate, a large total addressable market opportunity, and tailwinds as we come out of covid and as chip shortages are expected to abate. It trades at an attractive valuation, and we expect healthy dividend to keep growing in the years ahead. We do not currently own shares of Qualcomm, but if you are looking for a unique combination of dividends, growth and value—Qualcomm is worth considering. It is high on our watchlist, and we may add shares in the relatively near future.

The shares have gained significantly since that report was released, and we believe they have dramatically more long-term upside in the years ahead.

Honorable Mention: Nvidia (NVDA)

We’re including Nvidia as an “honorable mention.” We like Nvidia because it is the opposite of Intel. Specifically, Nvidia is a bold innovator at the forefront of massive secular change (digital transformation and the Internet of Things), and Nvidia’s CEO Jensen Huang has enough vision to capture these massively attractive opportunities.

As our members know, we have owned shares of Nvidia since May 2019 (we’re sitting on an enormous gain), but we reduced our position significantly within the last month. Not because we don’t think Nvidia will continue to be a huge long-term winner—we believe the company will be—but because we wanted to free up capital for other attractive opportunities—which we share with our members.

As you can see in our earlier table (near the start of this report) Nvidia has high margins and high growth. And despite a valuation that seems high to some, the company is set to continue capitalizing on massive total addressable market opportunities ranging from gaming, to data centers, to autonomous vehicles and artificial intelligence, to name a few. Long Nvidia.

2. Enphase (ENPH)

Switching gears a bit, Enphase offers semiconductor-based microinverters used in solar-powered home energy solutions, and the business is very attractive. If you consider the margins (gross and operating), growth rates (for this year and next) and long-term total addressable market opportunities of all the names in the table at the beginning of this report, Enphase is easily one of the most impressive. There is so much potential here, that it is astounding. That’s not to say the price won’t be volatile (it will) and the naysayers won’t be loud (they will), but Enphase is flat out attractive as a long-term investment opportunity.

For more information, you can read our full report on Enphase here, and here is an important quote from that report:

Enphase Energy is one of the most attractive plays in solar space. Operating in the fast-growing sustainable energy solutions industry, the company has demonstrated strong top-line growth and expanding margins over the last few years. While the company’s valuation is at a bit of a premium, Enphase’s microinverter technology and its highly integrated grid agnostic solar deployment with storage and real-time remote monitoring presents a strong moat. We like the opportunity here for long-term oriented investors, especially on the recent price pullback.

Shares of Enphase are up significantly since we released that report back on May 6th, but this one still has a lot more long-term price appreciation potential in the years ahead. Long Enphase.

Honorable Mention: Power Integrations (POWI)

We released a report on Power Integrations back on September 17, 2015, and the shares of this semiconductor stock have dramatically outperformed the market since that time.

We are sharing the link to that report to remind investors that there are many different types of chip stocks, and different valuation techniques are required for different types of opportunities. For example, price-to-earnings ratios make little sense for high-growth stocks focused on revenue growth (while they defer earnings), and in the case of Power Integrations, we used a combination of discounted cash flow valuation techniques and a compelling valuation formula first published in the 1940s by Warren Buffett's mentor, Benjamin Graham: EPS x (8.5 + (2 x growth)).

3. Micron (MU)

If you are looking for a true bargain in the semiconductor space, Micron could be it. The company manufactures memory and storage products (based on technologies such as DRAM, NAND, 3D XPoint memory and NOR), and the shares are very inexpensive relative to the company’s high growth and strong margins (see the table near the start of this report for details). Some investors don’t like Micron because its technology is older. However, Micron has some distinct competitive advantages. For example, it is the only American player in the oligopolistic DRAM space where the top three players (Samsung, SK Hynix and Micron) control ~95% of the market. Micron also gains advantage from its continuous focus on building DRAM technology leadership over the past few years, its diversified manufacturing facilities spread across geographies, and its better access to the US market which accounts for a major portion of demand for memory and storage products).

We concluded our previous full report on Micron (from back in December) with this:

Micron has transitioned itself into an industry leader and is well positioned to benefit from visible growth. Specifically, the company will benefit from improving DRAM industry dynamics and NAND industry consolidation. Further the business is on strong financial footing, and the valuation is reasonable. For these reasons, we believe Micron presents an attractive opportunity (to benefit from both cyclicality and long-term growth)

And seeing as how the company has continued to deliver this year, yet the share price has remained flat, we’re starting to wonder why we don’t yet own shares.

Conclusion:

Once a chip industry leader, Intel will be increasingly challenged going forward as its competitors have lurched ahead in terms of capturing the massive secular change opportunities, including the digital transformation and the Internet of Things. Intel’s focus on foundry chips and its own dividend are an indication of surrender, in our opinion. And Thursday evening’s earnings announcement is more confirmation that revenue growth and margins will likely be weak going forward.

We believe there are a variety of chip industry stocks that are more attractive than Intel, including the specific ideas we reviewed in this report, as well as the many additional names on our current watchlist. Every investor has their own unique investment goals, but whether you are a growth investor, a value investor, or an income investor, there are better opportunities in the chip space, including Enphase (growth), Micron (value) and Qualcomm (dividends and growth), respectively. At the end of the day, you have to know your goals as an investor, and then select opportunities that are right for you. You can learn more about how a membership to Blue Harbinger can help you in this regard, here.