Alibaba (BABA), often referred to as “the Amazon (AMZN) of China,” is the country’s largest e-commerce, cloud, and digital advertising company. Its e-commerce business has been the growth and profit engine for years, but cloud computing is positioned to increasingly contribute meaningfully to high-margin growth in the future. The perception of weak corporate governance, combined with geopolitical tensions, are major risks, and November could be a big month considering the US election, the company’s upcoming earnings announcement, and Singles’ Day. In this article, we analyze Alibaba’s business model, its market opportunities, fundamentals, valuation, risks, and finally conclude with our opinion on whether the stock offers an attractive balance between risks and rewards.

(Note: for a pdf version of this document, click here).

Alibaba (BABA) Price Chart:

Overview:

Alibaba is a Chinese company that specializes in e-commerce, retail, entertainment, and technology. Founded in 1999 by Jack Ma while he was working as an English teacher in Hangzhou, Alibaba’s primary area of operations remains in China. However, it is now taking significant initiatives to expand its global presence. In its initial years, Alibaba raised $25 million from several investors and later went public in 2014 at a valuation of $25 billion which was then the largest IPO ever. The company now provides B2B, B2C, and C2C ecommerce services as well as electronic payment and cloud computing services. Besides, Alibaba has also made investments in several global companies across various business sectors including 33% equity interest in Fintech company Ant Group which is in the process of going public.

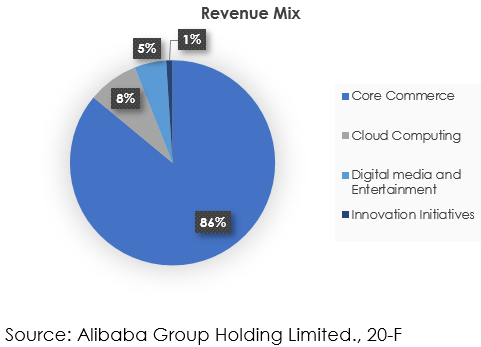

Alibaba conducts its business through four operating segments:

Core Commerce: This segment consists of the company’s various digital retail and wholesale online marketplaces including China focused ecommerce platforms such as Tmall, Taobao, Freshippo, 1688 etc. as well as cross border and global e-commerce platforms such as Aliexpress, Lazada and Alibaba.com. The segment also incorporates Alibaba’s logistics and local consumer services platforms. Revenue is generated in the form of commission charged on a percentage of sales basis from sellers for each sales transaction on its platform, Advertising fees charged to advertisers for online marketing on its websites, logistics fees charged for shipping of goods and other software services fee. This is Alibaba’s largest segment, and the company generates 86% of revenue from it with an operating margin of 38%. This segment is currently the only profit generating part of the company.

Cloud Computing: Through this segment, the company provides its public cloud computing services to enterprise customers. Its offerings include database, storage, management and application services, big data analytics and a machine-learning platform. Revenue is generated in the form of subscription fees based on period and specific usage of facilities. Although this segment contributes only 8% to the top-line of the company, it is Alibaba’s fastest growing segment. As the company is investing in expanding its cloud business, the segment is not yet profitable.

Digital media and Entertainment: In this segment, Alibaba operates Youku, the third largest online long-form video platform in China, as well as, Alibaba Pictures, one of the largest movie production houses in China. The segment contributes just 5% to the total revenue of the company and is currently loss making.

Innovation initiatives: Through this segment, Alibaba aims to innovate and develop new products and solutions for consumers. Previous innovations include, Amap, the largest provider of mobile digital maps in China, network communication app DingTalk and Tmall Genie smart speakers. This segment comprises of just1% of the total revenue of the company and is currently generating losses.

Consistently solidifying its leading market position in fast growing e-commerce markets

China has led the world in terms of Ecommerce sales for the last few years, and it continues to grow at a fast pace. As per Statista, Chinese e-commerce revenue stood at RMB 6.04 trillion in 2019 and is expected to increase to RMB 10.9 trillion by 2024, growing at a CAGR of over 12.5% over the next 5 years. The user penetration rate of the retail e-commerce market reached 59.3% in 2019 and is expected to expand to 79.2% by 2024. The strong growth is primarily attributable to technological advancements, growth in internet penetration in Chinese population, as well as consistent growth in middle/affluent class incomes in the country. Not only are more buyers moving to online retail from brick and mortar stores, existing ecommerce customers are spending more on shopping online. The average revenue per user was RMB 7,063 in 2019 and is expected to reach RMB 9,401 by 2024. This secular shift towards digitization was further accelerated because of the coronavirus pandemic as ‘stay at home’ orders were enforced globally including China. The same is also reflected in the charts below which show a sharp increase in ecommerce activity in 2020.

Riding this secular growth in e-commerce, Alibaba has consistently delivered impressive results since getting listed in 2014. In the last 12 months ending Q1 FY21, annual active customers on Alibaba’s China retail marketplace reached 742 million, which represents a YoY growth of 10% while average consumer spending on its platform reached RMB 9,000. The company’s customers are also sticky as evidenced by a high retention ratio of more than 96% for consumers who spend more than RMB 2,000.

Revenue generated from China retail marketplaces increased to RMB 358 billion during last 12 months ending June 2020 which represents a robust increase of 33% on a YoY basis. The primary drivers for this strong growth in revenue were increase in total Gross Merchandise Value (GMV) of products traded on its platform as it attracted more affluent and sticky customers as well as increase in take rate that includes commission and marketing fees charged from sellers. While China retail GMV during the last 12 months reached RMB 7.02 trillion growing by 23% YoY, take rate has expanded to 4% in Q1 FY21 as compared to 3.3% in 2017.

Alibaba enjoys a first mover advantage in the fast-growing Chinese e-commerce market. This has helped the company gain market share and become the largest online commerce company in China. Tmall, which is Alibaba owned online mall, was ranked the leading B2C retailer in China with a market share of 50%, almost double than that of its nearest competitor, JD.com (JD). Given it robust high-margin asset-light business model and strong financial position, Alibaba is well placed to further create a strong competitive moat around its business.

Alibaba Cloud all set to become the future growth driver of the company

Following the footsteps of Amazon, Alibaba also launched its cloud computing business in 2009, however unlike AWS which has a global presence, Alibaba primarily focuses on providing cloud computing services in Asia Pacific region. While globally, Alibaba Cloud ranks 4th behind AWS, Azure (MSFT) and Google Cloud (GOOGL) with a market share of just 5%, the company has been very successful in becoming the largest cloud computing service provider in its target market. China is the second largest public cloud computing market in the world after the US, however it is still 1/10th of the US public cloud market and therefore offers immense potential to expand in the near to medium term. As per Statista, the public cloud computing market in China stood at RMB 69 billion in 2019 and is expected to reach RMB 231 billion by 2023, growing at a CAGR of 35%. Currently, 4 local vendors account for almost 80% of the Chinese cloud market, with Alibaba leading the pack with a market share of over 40%, more than double its closest competitor, Huawei and Tencent (TCEHY) that hold 15% share each.

Although, Alibaba Cloud contributes just 8% of the total revenue, it is the fastest growing segment of the company. In Q1 FY21, cloud computing revenue stood at RMB 12.3 billion which reflects a YoY growth of 59%, significantly outperforming other segments. This impressive growth was achieved by increased customer usage of its public as well as hybrid cloud facilities fueled by the move towards business digitization. The company recently announced its plans to invest RMB 200 billion in the next 3 years to further expand its cloud infrastructure to capitalize on the growing market opportunity and the industry leading position it currently holds in the Asia Pacific region. We believe the cloud computing segment has the potential to become a major revenue driver for Alibaba in the next few years.

Robust fundamentals with enough liquidity to fund growth investment needs

In Q1 FY 21, the company reported total revenue of RMB 154 billion which represents a YoY growth of 34%. Strong growth was achieved across all segments. While the core commerce segment expanded by 34% on a yearly basis, cloud computing outperformed all others as discussed earlier by delivering a growth of 59% because of a sharp rise in demand. In the last 5 years, the company has consistently delivered an impressive top line increase by posting a CAGR of 50%.

On the profitability front, core commerce is the only profitable segment of the company as others are still in investment mode as Alibaba has been consistently re-investing all profits to expand its customer footprint and fuel further long-term growth. In Q1 FY21, Alibaba’s adjusted EBITDA increased by 30% on a YoY basis to RMB 51 billion. EBITDA margins declined from 34% in Q1 FY20 to 33% in Q1 FY21. This was because of a higher cost of revenue in the core commerce segment, primarily due to increased revenue contribution from its self-operated New Retail and direct sales business (Freshippo), which involves purchase of inventory and revenue being recorded on a gross basis and hence lower margins as compared to commission based revenue from its online marketplaces. Besides this, all other major segments reported an improvement in profitability. The Cloud Computing segment’s operating loss margin has now reduced to just -3% and the company expects to achieve operating profitability by the end of this fiscal year. Alibaba’s operating profits will continue to expand as it further solidifies its customer footprint in China in a fast-growing addressable market and achieves economies of scale along with higher operating leverage.

Alibaba’s primarily asset-light focused business model has helped the company generate strong free cash flow margins and internal capital to consistently invest in expanding its business without much outside funding. In Q1 FY 21, FCF increased by 39% to RMB 37 billion, from RMB 26 billion in the same quarter mainly because of rising sales and improving profits. It ended the recent quarter with liquidity of RMB 382 billion in the form of cash and short-term investments. With no major financial liabilities on the balance sheet, the current liquidity position provides enough firepower to meet growth and strategic investment needs in the near to medium term.

The company is using its FCF to fund several other growth initiatives apart from commerce and cloud. In the Digital media and entertainment segment, Alibaba operates its video streaming platform Youku which it acquired in 2016. In the quarter ended June 2020, Youku’s daily active subscriber base increased by more than 60% on a YoY basis following the release of local popular TV shows, whereas the number of paying subscribers increased by 52%. The company’s small but growing young businesses will benefit from its robust financial position and market reach.

Appealing valuation despite inherent risks involved

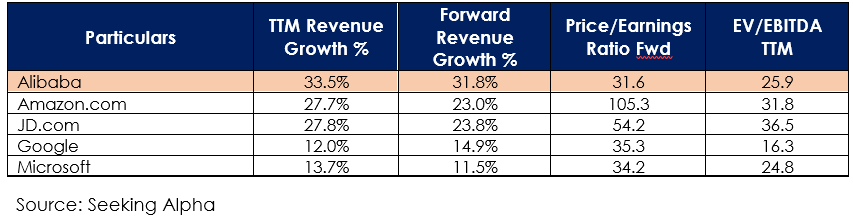

Alibaba’s stock price has risen by almost 40% in 2020 and currently trades at a forward price to earnings multiple of 31.6x which is below its global peers including Amazon.com despite superior growth rates. Apart from corporate governance risks that are inherent in China based companies, another reason for this discounted valuation is intensified scrutiny of US listed Chinese companies by the Trump administration. Adding to that is the ongoing trade war between China and the US. Given that geopolitics has suppressed multiples of Chinese names over the last few years, a potential Joe Biden win in next month’s elections could be a catalyst for Alibaba’s stock as well as other Chinese companies given his perceived less-hostile stand on globalization and China.

Finally, the upcoming IPO of Ant Group could act as a catalyst spurring the company’s valuation multiples. Ant group operates ‘Alipay’ which is China’s biggest digital payment app and is controlled by Jack Ma. Investors valuing Alibaba’s stake of 33% in Ant Financial post IPO would further magnify the current valuation discount.

Risks

In addition to uncertainty surrounding the upcoming Ant Group IPO (expected Nov 5th), BABA's earnings release (slated for November 5th) and Single's Day (on November 11th), Alibaba faces a couple more big risks to keep in mind.

Weak corporate governance: Several Chinese companies suffer from weak corporate governance structures primarily because of subpar regulatory oversight as well as allegedly significant interference of Government authorities in business activities. We believe the risk of a large-scale corporate governance failure in big tech in China is relatively low as compared to Chinese small and mid-caps.

Geopolitical tensions: China has been in the midst of consistent geopolitical tensions for the last 3 years. The trade war between the US and China followed by increased global scrutiny because of the coronavirus pandemic as well as the passing of Hong Kong national security law. These geopolitical conflicts may invite sanctions against China or China based companies. Given Alibaba’s revenue is concentrated in China and parts of Asia Pacific, we believe the company is, relatively speaking, well placed.

Conclusion

Alibaba is an e-commerce juggernaut. And it can extend its track record of very high growth by transitioning to the massive opportunity that exists in cloud computing. And despite the volatility risks that will be magnified in the next 2-weeks (by the US election, an earnings announcement, the Ant Group IPO and Singles Day), we have included Alibaba on our recent ranking of top 10 growth stocks because the valuation remains extremely compelling relative to its growth potential. We believe these shares go significantly higher in the long-term (despite the near-term volatility risks), and we are currently long Alibaba.