Exxon Mobil’s dividend yield is near a 25-year high. It is supported by a pristine balance sheet and an attractive growth strategy that give the shares significant upside. This article reviews the health of the business, cash flow position, balance sheet flexibility, valuation, risks, dividend safety, and concludes with an explanation of why we ranked XOM No. 7 on our list of Top 10 Big Safe Energy Sector Dividends.

Overview:

Exxon Mobil is the largest publicly traded oil & gas company which is involved in exploration, production and marketing of oil and natural gas. The company operates via three segments – 1) Upstream, which includes oil & gas exploration and production; 2) Downstream, includes refining and marketing; and 3) Manufactured chemicals, includes manufacturing and trading of petrochemicals such as olefins, aromatics, polyethylene, and polypropylene plastics. As of the end of Q319, XOM’s total production stood at 3.9 million oil equivalent barrels per day (Mboed).

Important to note, Upstream accounts for nearly 80% of XOM’s earnings making it by far the most important segment of the company. XOM is betting aggressively on further growing its Upstream assets and expects to spend a combined ~$46-$48 billion on its Upstream segment for 2019-2020.

Dividend Yield – Higher than Normal but Sustainable

ExxonMobil's dividend payments have grown at an average annual rate of 6.2% over the last 37 years. The current dividend yield of 5% is among the highest recorded in its operating history. The last time it touched or went above 5% was in the mid 1990’s, more than 25 years back. For perspective, the chart below provides a look at the historical dividend yield over the last 30 years.

(source: Macrotrends)

It is important to note that the rise in dividend yield is due to a sharp decline in share price over the past 6-8 months. The stock has declined nearly 17% from its high touched in April 2019. This has coincided with the drop in crude oil prices as seen in the charts below.

(source: ycharts)

Falling commodity prices have hurt Exxon’s share price. The company reported a 49% decline in its Q319 earnings. For 2019, XOM shares are down slightly, and all investor gains have come via the ~5% dividend yield. And in our view, the dividend looks extremely safe. Through Q319, XOM generated a healthy $23.4 billion in cash flow from operating activities, which was more than enough to cover nearly $11 billion it paid out in dividends.

The company is in the middle of an ambitious long-term growth program will put slight pressure on cash flow available for distribution, but XOM can afford it with plenty of liquidity to spare and plenty of cushion on the dividend. Noteworthy, XOM’s top-tier balance sheet and asset sale program is enough to easily bridge any shortfall. For example, Exxon has sold $4.8 billion in assets this year and is already ahead of its target sales of $15 billion of assets by 2021.

Exxon' high-yielding dividend appears extremely sustainable. Given cash flow growth, the healthy balance sheet and the asset sale program, we believe that Exxon will be able to easily continue increasing its dividend—an attractive quality for income-focused investors.

Peak Oil Theory Still Decades Away

One of the reasons XOM shares have lagged the market is fear and uncertainty related to the future of oil as alternative sources of energy gain attention. However, the world is extremely unlikely to transition dramatically to alternate sources of energy for decades. In fact, the International Energy Agency (“IEA”) estimates approximately $21 trillion of oil and natural gas investment will be needed by 2040. For example, the chart below indicates that oil & natural gas demand will continue to remain robust even in 2040. XOM’s oil business continues to be a cash cow and will remain so in the future as global demand persists. This will help fund massive dividends and buybacks. While we acknowledge headwinds for the industry are very real, the fear and sell off are dramatically overblown.

(source: Company Presentation)

Growth Prospects Supported by Strong Free Cash Flow

The business environment for oil & gas majors remains somewhat challenged in the near-term amid low crude oil prices (still down by nearly half from peak levels of 2014). This has not prevented Exxon from investing for the future. In fact, the company is projecting capital expenditure of ~$35 billion a year through 2025 on new oil and natural gas drilling projects as well as new processing plants. We are encouraged by the fact that the majority of the investing is done via internal accruals supported by strong free cash flow generation.

For example, the chart below highlights XOM’s annual free cash flow generation over the past several years. Cumulative free cash flow over this time period is well in excess of its cumulative dividend. This provides a strong basis to make value accretive investments.

(source: Company Presentation)

The company’s growth plans are progressing on schedule supported by long-term fundamentals. XOM Vice President Neil Hansen had this to say during the most recent earning call:

“Exploration success has continued this year with five significant deepwater discoveries, oil in Guyana and one in Cyprus. And we've reached final investment decisions for 10 major strategic projects this year, including projects from all three business lines.”

(source: Company Presentation)_

In the upstream segment, production is set to rise in the coming years driven by growth in the Permian Basin as well as key deepwater and LNG projects slated to come on stream over the next several years. XOM is projecting low-single digit production growth through 2025 (and this is fantastic when you consider the boost from the dividend and the potential for a return to significant share repurchases). XOM remains on track to meet the full-year outlook of producing 4 million oil equivalent barrels per day (Moebd) this year. Overall, between 2019-2025, it is targeting additional production of 2.5 Mboed.

(source: Company Presentation)

The production growth is expected to boost earnings as well. XOM expects earnings to increase 140% by 2025 (compared to 2017), assuming a $60/bbl flat oil price scenario. Additionally, XOM has tremendous leverage to oil prices as well (as shown in chart below). Even at $35/bbl, Exxon’s flagship Permian assets can earn double-digit return highlighting its strong operating characteristics.

(source: Company Presentation)

In the Downstream segment, the company is targeting earnings growth of 60% by 2020 and almost double by 2025 (relative to 2017). During the Q3 call, management highlighted that

“In the Downstream, three new projects are online and performing well, reporting increased production of cleaner, higher-value products. We've made final investment decisions this year for four additional projects, including the Beaumont light crude expansion and the Wink to Webster pipeline, both of which will support our integrated Permian strategy and growth plans.”

Enhancing Portfolio Competitiveness

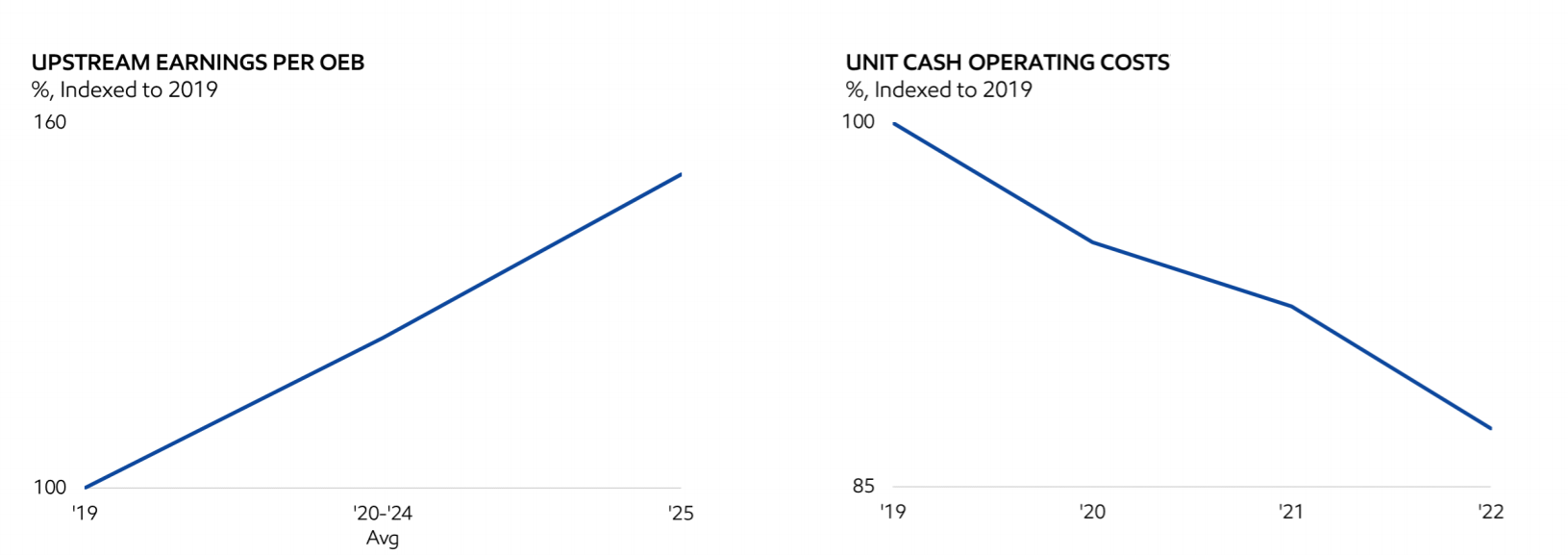

Across the three segments, XOM has made great strides in “high-grading” its portfolio. We note XOM’s prior annual 5 -year average has been ~$3.6 billion of asset sale proceeds primarily focused on high-grading its Downstream and Chemical segments. But going forward, for the period 2019-2021, the focus has shifted to Upstream segment. The company plans to simplify operations through the sale of assets that are non-core and lack growth potential. XOM estimates this will reduce the number of assets in its upstream portfolio by 20%. Overall, the plan is to sell $15 billion of assets by 2021. The program will free up capital, helping to boost free cash flow generation to support its expansion plans and dividend payments. Also, the high-grading is expected to result in lower costs and better margins for the upstream segment (as seen in chart below).

(source: Company Presentation)

Exxon Mobil's plan to sell billions of dollars in assets may pave the way for the company to return cash to stockholders through a long-awaited share buyback program, says Chairman and CEO Darren Woods. XOM recently forecast it could generate $15 billion in cash through 2025 by selling assets.

Valuation:

XOM is trading at ~8.9x EV/EBITDA, a warranted premium to some peers (see chart below). We believe the premium is justified given its larger size, higher ROCE and pristine balance sheet (debt to equity among the lowest). That said, there is scope for the premium to further increase if the company is successful is executing its long-term growth strategy, as described earlier. This means investors should expect share price gains when management delivers on its strategy. Historically speaking, XOM’s EV/EBITDA has ranged between 3.4 to 14.1over the past 13 years. And considering the company’s strategy, there is potential for attractive multiple expansion, in addition to the big safe dividend and potential for share repurchases.

(source: Thomson Reuters)

For a little perspective, “Exxon Mobil shares could surge nearly 50% as production ramps up and growth accelerates, according to BofA Merrill Lynch, which names the company its top U.S. oil major pick for 2020 and raises its stock price target to $100 from $68.”

Risks:

Commodity price risk: As noted earlier, XOM’s earnings and cash flows are highly dependent on crude oil and natural gas prices. When oil and gas prices fall, so does earnings for XOM. Important to note, however, management has done an exceptional job ensuring that dividends remain steady (and growing), despite volatility in energy prices.

Execution risk: The company is in the middle of an ambitious long-term growth program. This includes aggressive expansion plans across its three segments as well as high-grading its upstream portfolio via an asset sale program. XOM’s future cash flows are therefore dependent on the ability of management to execute. And based on historical accomplishments, we have confidence that management will deliver.

Conclusion:

Exxon Mobil is one of the best options in the energy sector for investors seeking big healthy growing dividend payments and attractive price appreciation potential. We believe a variety of factors (including those described in this report) have combined to create this attractive buying opportunity, and we've therefore ranked XOM No. 7 on our recent list of top 10 big safe energy sector dividends, ahead of BP (BP) which we wrote-up at No. 8, and behind Tsakos preferred shares (TNP.PE) which we wrote-up at No. 6. Overall, the negative narrative and very weak performance of the Energy Sector in 2019 have created some very attractive big-dividend buying opportunities, including Exxon Mobil.