If you are an income-focused value investor, there are plenty of attractive big-dividend contrarian opportunities available in the market right now. That may sound hard to believe considering the S&P 500 is having such a strong rebound this year (its up over 22%), but there are healthy big dividends trading at attractively discounted prices (i.e. they have significant price appreciation potential). In fact, many of the names on our top 10 list will likely perform very well on a relative basis even if the rest of the market turns south. Further, we expect them to keep paying you the steady big dividends you like, regardless of market conditions.

For a little perspective, before we start counting down our top 10 ranking, it’s worth highlighting what parts of the market have NOT been performing well because they’re ripe with contrarian opportunities as we will cover later in this report.

To be specific, several of the worst performing areas of the stock market this year (even though the overall market has been strong, as represented by the S&P 500) are:

Energy stocks (XLE): +6.6%

Healthcare stocks (XLV): +7.6

Small Cap stocks (IWM): 16.9%

Value stocks (IWD): 19.0%

Victim-of-False-Narratives stocks: (more on these in a moment)

S&P 500 (SPY): +22.4%

We’d never go out blindly buying stocks just because they’re in a sector or style that has performed poorly (as some less discriminating contrarians do), however these segments can be a good place to start looking for opportunities—and they have turned up a handful, considering all of the names on our Top 10 ranking come from the categories listed above.

To help you better understand how we view the opportunities on our list, we’ve broken them down into two broad categories:

Opportunistic High Income (“OHI”)

Steady High Income (“SHI”)

Hopefully, these names are somewhat self-explanatory, but the OHI opportunities generally offer higher dividend payments, but also somewhat higher volatility risk (the whole “risk-reward” trade-off thing—they’re still quite attractive on a risk-adjusted basis). Whereas the SHI opportunities offer lower yields (they’re still high yields, just less high than the OHI names), but they also are generally less volatile/risky. We break the names down into these categories to help you as you construct your own investment portfolios (and they are also, by the way, the categories we use within our own 25-stock “Income Equity” portfolio, which continues to perform very well).

Lastly, before we start counting down our rankings, be sure to click the “full report” link for each idea, if you are looking for a deeper dive into why we like that particular opportunity.

Without further ado, here are our Top 10 Big Dividends, counting down from #10 to #1…

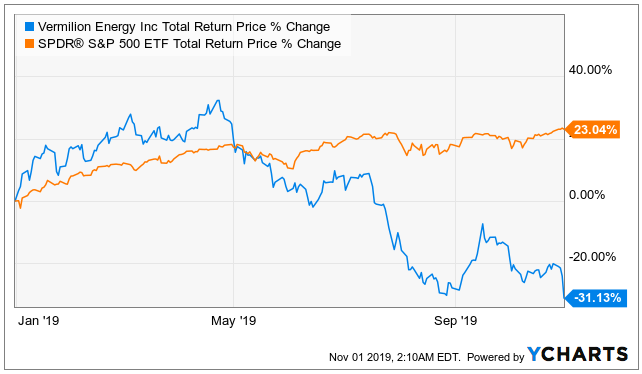

10. Vermilion Energy (VET) (“OHI”), Yield: 13.6%

Vermilion Energy is global oil and gas producer based out of Canada. It pays a big, healthy, monthly dividend, and the shares trade at an attractively discounted price, especially after this year’s sell-off (which accelerated after a disappointing earnings announcement this past week, whereby management announced they’d be reducing capex spending).

In our view, the sell-off has been inappropriate. Vermilion has a well diversified portfolio of oil and gas resources across North America, Europe and Australia; and we expect the company to deliver consistent mid-to-high single digit production growth. We also like the business’ large exposure to higher priced and margin Brent and European Gas sales. Further, the dividend yield of over 13% provides a very attractive entry point to lock in high dividend payments with a superior production growth profile. Here is a quote from management taken from this week’s earnings release:

“We would like to stress that Vermilion's dividend policy is not based on the market price of our shares. Our dividend policy is based on the fundamental economic sustainability and free cash flow generation of our business, which remains strong.”

We’ve categorized this one as “OHI,” and we believe it offers a very attractive-risk reward opportunity. You can read our full report on Vermilion here…

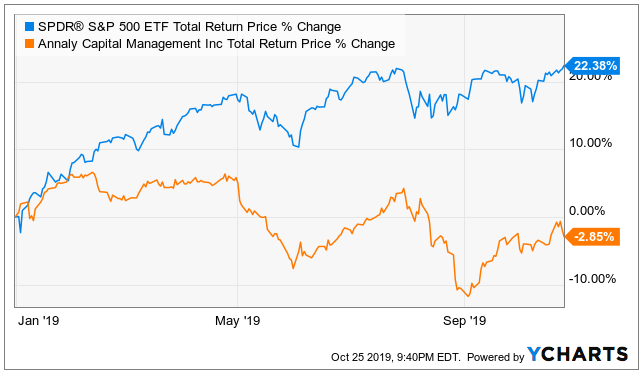

9. Annaly Capital (NLY) (“OHI”), Yield: 11.3%

Annaly Capital is a big-dividend MREIT (Mortgage, Real Estate Investment Trust). And its current valuation is appealing considering it trades at only 0.95x its tangible book value.

Annaly’s investment portfolio primarily consists of mortgage-based securities that are created out of a pool of similar types of mortgages from banks through the process of securitization. It’s the largest mortgage REIT with several times the market cap of the average listed mREIT, and this provides it with access to a broad set of funding sources. Further (and importantly) its core agency backed residential mortgage REIT business is set to benefit from declining interest rates. It’s basically a rare, counter-cyclical income-oriented company. We’ve put this one into our OHI category, and you can read our detailed full report below.

8. Simon Property Group (SPG), (“SHI”), Yield: 5.3%

Simon Property Group is an “A-Class” mall REIT that’s been caught up in the “false narrative” that the internet is going to kill all brick-and-mortar shopping facilities. And as a result, the shares have sold-off (inappropriately, in our view).

And while the changing retail langscrape (i.e. the Internet) is having a significant impact on many lower quality “B-Class” malls, Simon continues to grow its business, its funds from operations and its dividend. In our view, Simon is like a baby that’s been thrown out with the bathwater. Its dividend is very healthy and its price is too low. Because of these attractive factors, we put Simon into our “Steady High Income” category. Our recent write-up on Simon (see link below) explains a relatively low risk yet attractive high income-generating options trade strategy that we continue to have success with. You can read our Simon write-up here:

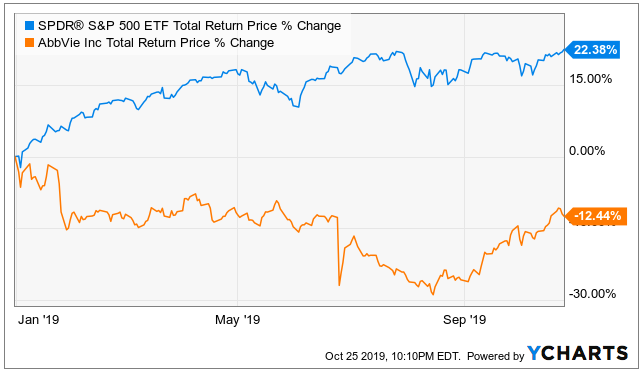

7. AbbVie (ABBV), (“SHI”), Yield: 5.6%

AbbVie is engaged in research, development and marketing of biotech drugs. And the stock price has tested investor patience over the last 12-15 months.

AbbVie’s stock has been under pressure as a result of the lack of visibility into long term earnings as the company’s blockbuster drug Humira which accounts for 61% of sales goes ex patent in 2023 in the US. However, the Allergan acquisition is a game changer, and AbbVie’s own drug pipeline should not be ignored. The company has a strong cash flow generation and income profile, and the current valuation is appealing. We’ve put this one in our “Steady High Income” category, and you can access our full AbbVie report here:

6. Adams Diversified Equity (ADX), (“SHI”), Yield: 12.9%

The Adams Diversified Equity fund is a closed-end fund, it trades at an attractive discount to its net asset value (“NAV”), and despite the small and misleading yield posted on most websites, ADX pays out at least 6% every year (it payed 12.9% is 2018, and will likely pay significantly more than 6% in 2019 as well because of the strong performance of the underlying holdings so far this year), and the fourth quarter distribution payment (just around the corner) is the big one each year (ADX pays three smaller quarterly dividends, followed by a larger Q4 payment).

And what makes ADX particularly attractive (besides the things already mentioned above) is that it is well-diversified and actively managed across diversified sectors that income-focused investors often ignore (this is why we’re considering it “contrarian” value—because it goes against the typical income-focused sectors of the market, yet still offers big income payments to investors). This makes the fund very attractive for risk-management and income reasons. Further, ADX has been paying a dividend for over 80 years! Here is a quote from our previous ADX report (below) or you can access all of our previous ADX reports using the link right after the quote:

Adam’s Diversified Equity Fund (ADX): Not only is this CEF heavy into technology and consumer discretionary stocks, but it offers a very big yield of at least 6% every year (last year it paid over 9%). And this particular CEF has been around and paying dividends for over 80 years (note: it pays three smaller dividends in the first three quarters of every year, followed by a big year-end Q4 dividend every year). It also trades at an attractive discount to its NAV, it uses zero leverage, it has a very low management fee for a CEF, a solid management team, and we own ADX in our Blue Harbinger Income Equity portfolio. You can view more details about ADX from {CEF Connect]… (such as the metrics we described above, and more, including top holdings)

We put this one in our “Steady High Income” category because of the attractive diversification and its long track record of steady high income.

The Top 5 Big Dividends

Our Top 5 Big Dividend ideas are reserved for members only. They offer yields ranging form 6% to over 9%, and we currently own all 5 of them.