If you are an income-focused value investor, there are plenty of attractive big-dividend contrarian opportunities available in the market right now. That may sound hard to believe considering the S&P 500 is having such a strong rebound this year (its up over 22%), but there are healthy big dividends trading at attractively discounted prices (i.e. they have significant price appreciation potential). In fact, many of the names on our top 10 list will likely perform very well on a relative basis even if the rest of the market turns south. Further, we expect them to keep paying you the steady big dividends you like, regardless of market conditions.

For a little perspective, before we start counting down our top 10 ranking, it’s worth highlighting what parts of the market have NOT been performing well because they’re ripe with contrarian opportunities as we will cover later in this report.

To be specific, several of the worst performing areas of the stock market this year (even though the overall market has been strong, as represented by the S&P 500) are:

Energy stocks (XLE): +6.6%

Healthcare stocks (XLV): +7.6

Small Cap stocks (IWM): 16.9%

Value stocks (IWD): 19.0%

Victim-of-False-Narratives stocks: (more on these in a moment)

S&P 500 (SPY): +22.4%

We’d never go out blindly buying stocks just because they’re in a sector or style that has performed poorly (as some less discriminating contrarians do), however these segments can be a good place to start looking for opportunities—and they have turned up a handful, considering all of the names on our Top 10 ranking come from the categories listed above.

To help you better understand how we view the opportunities on our list, we’ve broken them down into two broad categories:

Opportunistic High Income (“OHI”)

Steady High Income (“SHI”)

Hopefully, these names are somewhat self-explanatory, but the OHI opportunities generally offer higher dividend payments, but also somewhat higher volatility risk (the whole “risk-reward” trade-off thing—they’re still quite attractive on a risk-adjusted basis). Whereas the SHI opportunities offer lower yields (they’re still high yields, just less high than the OHI names), but they also are generally less volatile/risky. We break the names down into these categories to help you as you construct your own investment portfolios (and they are also, by the way, the categories we use within our own 25-stock “Income Equity” portfolio, which continues to perform very well).

Lastly, before we start counting down our rankings, be sure to click the “full report” link for each idea, if you are looking for a deeper dive into why we like that particular opportunity.

Without further ado, here are our Top 10 Big Dividends, counting down from #10 to #1…

10. Vermilion Energy (VET) (“OHI”), Yield: 13.6%

Vermilion Energy is global oil and gas producer based out of Canada. It pays a big, healthy, monthly dividend, and the shares trade at an attractively discounted price, especially after this year’s sell-off.

In our view, the sell-off has been inappropriate. Vermilion has a well diversified portfolio of oil and gas resources across North America, Europe and Australia; and we expect the company to deliver consistent mid-to-high single digit production growth. We also like the business’ large exposure to higher priced and margin Brent and European Gas sales. Further, the dividend yield of over 13% provides a very attractive entry point to lock in high dividend payments with a superior production growth profile. We’ve categorized this one as “OHI,” and we believe it offers a very attractive-risk reward opportunity. You can read our full report on Vermilion here…

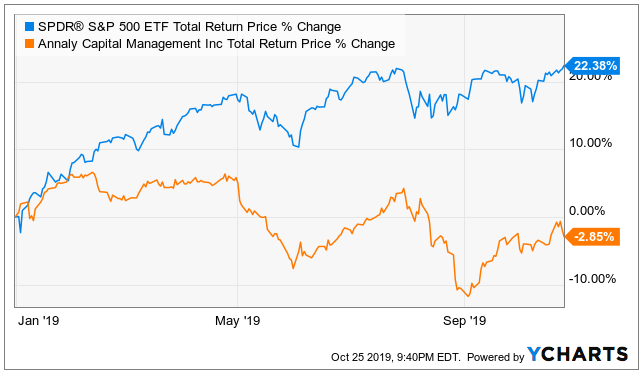

9. Annaly Capital (NLY) (“OHI”), Yield: 11.3%

Annaly Capital is a big-dividend MREIT (Mortgage, Real Estate Investment Trust). And its current valuation is appealing considering it trades at only 0.95x its tangible book value.

Annaly’s investment portfolio primarily consists of mortgage-based securities that are created out of a pool of similar types of mortgages from banks through the process of securitization. It’s the largest mortgage REIT with several times the market cap of the average listed mREIT, and this provides it with access to a broad set of funding sources. Further (and importantly) its core agency backed residential mortgage REIT business is set to benefit from declining interest rates. It’s basically a rare, counter-cyclical income-oriented company. We’ve put this one into our OHI category, and you can read our detailed full report below.

8. Simon Property Group (SPG), (“SHI”), Yield: 5.3%

Simon Property Group is an “A-Class” mall REIT that’s been caught up in the “false narrative” that the internet is going to kill all brick-and-mortar shopping facilities. And as a result, the shares have sold-off (inappropriately, in our view).

And while the changing retail langscrape (i.e. the Internet) is having a significant impact on many lower quality “B-Class” malls, Simon continues to grow its business, its funds from operations and its dividend. In our view, Simon is like a baby that’s been thrown out with the bathwater. Its dividend is very healthy and its price is too low. Because of these attractive factors, we put Simon into our “Steady High Income” category. Our recent write-up on Simon (see link below) explains a relatively low risk yet attractive high income-generating options trade strategy that we continue to have success with. You can read our Simon write-up here:

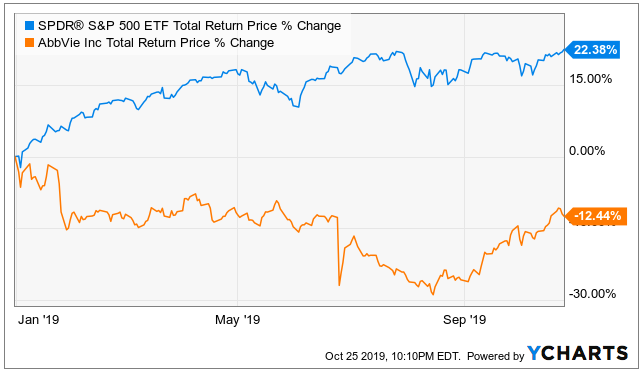

7. AbbVie (ABBV), (“SHI”), Yield: 5.6%

AbbVie is engaged in research, development and marketing of biotech drugs. And the stock price has tested investor patience over the last 12-15 months.

AbbVie’s stock has been under pressure as a result of the lack of visibility into long term earnings as the company’s blockbuster drug Humira which accounts for 61% of sales goes ex patent in 2023 in the US. However, the Allergan acquisition is a game changer, and AbbVie’s own drug pipeline should not be ignored. The company has a strong cash flow generation and income profile, and the current valuation is appealing. We’ve put this one in our “Steady High Income” category, and you can access our full AbbVie report here:

6. Adams Diversified Equity (ADX), (“SHI”), Yield: 12.9%

The Adams Diversified Equity fund is a closed-end fund, it trades at an attractive discount to its net asset value (“NAV”), and despite the small and misleading yield posted on most websites, ADX pays out at least 6% every year (it payed 12.9% is 2018, and will likely pay significantly more than 6% in 2019 as well because of the strong performance of the underlying holdings so far this year), and the fourth quarter distribution payment (just around the corner) is the big one each year (ADX pays three smaller quarterly dividends, followed by a larger Q4 payment).

And what makes ADX particularly attractive (besides the things already mentioned above) is that it is well-diversified and actively managed across diversified sectors that income-focused investors often ignore (this is why we’re considering it “contrarian” value—because it goes against the typical income-focused sectors of the market, yet still offers big income payments to investors). This makes the fund very attractive for risk-management and income reasons. Further, ADX has been paying a dividend for over 80 years! Here is a quote from our previous ADX report (below) or you can access all of our previous ADX reports using the link right after the quote:

Adam’s Diversified Equity Fund (ADX): Not only is this CEF heavy into technology and consumer discretionary stocks, but it offers a very big yield of at least 6% every year (last year it paid over 9%). And this particular CEF has been around and paying dividends for over 80 years (note: it pays three smaller dividends in the first three quarters of every year, followed by a big year-end Q4 dividend every year). It also trades at an attractive discount to its NAV, it uses zero leverage, it has a very low management fee for a CEF, a solid management team, and we own ADX in our Blue Harbinger Income Equity portfolio. You can view more details about ADX from {CEF Connect]… (such as the metrics we described above, and more, including top holdings)

We put this one in our “Steady High Income” category because of the attractive diversification and its long track record of steady high income.

5. Royce Micro Cap Trust (RMT), (“SHI”), Yield: 9.0%

The Royce Micro Cap Trust is another attractive income-focused CEF that made the list as a steady high income opportunity. And like ADX (mentioned above) we like RMT because it offers income payments from a portfolio of investments (small cap value stocks) that most income-focused investors often ignore.

Not only is this attractive but it’s smart because it can help you keep you income high and your risks lower (via valuable diversification). We like the Royce team, the strategy, the income it provides, and the discount to NAV, to name a few. Plus, small cap (micro cap) stocks have been underperfoming the overall market, and they are currently attractive from a contrarian standpoint. This fund is somewhat similar to the Royce Value Trust (RVT) (another small cap CEF that is managed by the same team, and that we also currently own), and you can view our full write-up here:

Honorable Metnion: Pfizer (PFE), (“SHI”), Yield: 4.0%

Pfizer is another attactive pharmaceutical stock. And not only has the pharmaceutical industry been out of favor (the whole healthcare sector has been, for that matter), but we like Pfizer even more than AbbVie (ranked #7 in this report) because Pfizer’s business is steadier, more attractively diversified, and overall healthier. We’re labeling this one as an “honorable mention” because the yield is a little lower than the others on this list, but when you combine the yield with the price appreciation potential, Pfizer is very attractive as a long-term investment opportunity.

Pfizer is basically a very attractive blue-chip business, trading at an attractive valuation and offering an attractive dividend payment to investors. You can read our full report on PFE using the link below:

4. Adams Natural Resources (PEO), (“SHI”), Yield: 6.0%

The Adams Diversified Equity Fund (ADX) made it onto our list at #6, but another Adams fund makes it to #4. The Adams Natural Resources fund (PEO) is a play on the weak performance of energy (as well as materials) stocks this year.

Not only does this Closed-End Fund trade at a very attractive discount to its NAV, but it also offers a big yield (at least 6% a year, with the biggest annual distribution in Q4, coming up soon). Further still, this is an attractive, actively-managed, contrarian play on energy (and other materials) thereby giving this fund some compelling price appreciation potential, especially considering the discounted prices of many of its underlying holdings (such as BP and RDS, which we’ve also recently written about in great detail). We put this one as a “Steady High Income” opportunity, and you can read our full report on PEO, here…

3. NuStar Energy (NS-C), (“SHI”), Yield: 9.1%

Even though these preferred shares trade at only a small discount (i.e. they’re priced just under $25, they have more upside than the price applies (they can easily trade at a premium—i.e. above $25) given the very high dividend payments and the increasing safety of the business. You can read our full write-up on NuStar preferred shares using the following link.

2. Teekay Offshore Preferred (TOO-B), Yield: 9.3%

We’ve received some good news about these shares over the last month. Specifically, Brookfield raised its bid for the common shares of Teekay Offshore, and Teekay accepted the offer, thereby sending both the common and preferred shares significantly higher.

Further, the acceptance of the bid takes a lot of uncertainty off the table about any potential games Brookfield could have taken at the expense of existing shareholders. Importantly, Teekay Offshore is a much much stronger company financially now that they’ve accepted the deal, and it seems these preferred shares can likely trade all the way back up to $25 (or higher) in the coming weeks and months. You can read our previous write-up on these preferred shares (written right BEFORE the offer from Brookfield and acceptance by Teekay within the last few weeks) here:

Honorable Mention:

Williams Companies (WMB), (“SHI”), Yield: 6.5%

These shares are quite attractive, but we’re listing them only as an “honorable mention here because we’ve already got a handful of energy sector names on this list, and the next name on our list is similarly attractive, but with a signficantly higher yield. You can read our recent full write-up on Williams Companies using the following link:

1. Energy Transfer (ET), (“SHI”), Yield: 9.8%

Energy Transfer (ET) is a stable, cash flow generative Master Limited Partnership (MLP) that operates energy oriented transportation, storage and midstream assets in major production basins in the United States. The business offers stable cash flows driven by volume rather than price driven energy contracts. And importantly, the company’s capex and debt levels are expected to fall further after peaking back in 2017. And very importantly for income-investors, Energy Transfer has solid distribution coverage of 2x, and a very appealing dividend (given the stability of the cash flows).

Energy Transfer trades at a compelling price, and you can read our full report, here:

Note: we currently own shares of SPG, ADX, RMT, NS-C, TOO-B, WMB, PEO, ET

Conclusion:

Just because something has sold-off doesn’t automatically mean it is a good contrarian investment opportunity. However, reviewing things that have sold-off can be a good place to search for attractive opportunities. In this report, we have identified and ranked attractive big-dividend opportunities, and all of them are ‘contrarian” one way or another, as explained in this report. And if you are looking for additional attractive high-income/big-dividend opportunities, you can view all of our current holdings (and performance) here: