Long-term investing is a proven strategy to build wealth, and it is a lot more powerful than many investors realize. However, whether you are brand new to investing or a seasoned pro, there are seven terrible mistakes (deadly sins) that can easily prevent you from achieving success.

Before getting into the details of the seven deadly sins, here is a fun analogy from famous value investor, Warren Buffett, about the benefits of long-term investing:

“Someone’s sitting in the shade today because someone planted a tree a long time ago.”

Without further ado, here are the seven deadly sins of long-term investing.

7. Cash Hoarding

Having too much cash in the bank...

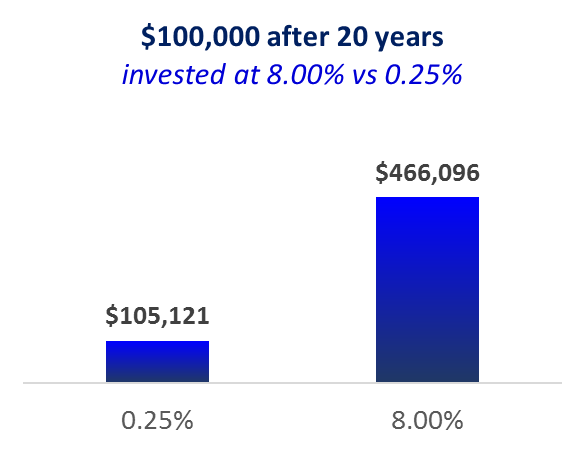

You might think you can NEVER have too much cash in the bank, but you sure can if it's not working for you. Considering interest rates are so low (thanks to the Fed, and because checking and savings accounts offer very low interest rates anyway), it is an incredibly dangerous practice to keep too much cash in your bank account. Specifically, it can ruin your chances for long-term success because of the extreme opportunity costs. For example, if you’d like to live comfortably in retirement someday, you’re probably going to need to move some of that money from cash into long-term investments. Don’t believe me? Here is a look at the value of $100,000 that sits in cash in your bank account for 20 years, versus the value of $100,000 in the stock market:

Assuming an 8% total return for stocks and the one quarter of 1% interest in a checking account (if you're lucky), twenty years from now, would you rather have $105,121 or $466,096? And remember, after inflation, you won’t be able to buy nearly as much with $100,000 in 20 years as you could today. If you ever want to live comfortably in retirement (or even get to retirement, for that matter), you’re probably going to need to move some of your cash into long-term investments. For example, a low-cost diversified portfolio of long-term stock investments is a lot less risky than cash over the long-term after you factor in inflation and the huge opportunity costs.

Still not convinced you can have too much cash? A common argument is that investors keep cash on hand to "buy, buy, buy" if the market crashes. Sounds like market timing to us. No one has a working crystal ball, and market timing is a proven strategy for failure. Your chances for success are far better off if you don't keep too much cash in your bank account.

6. Forced Selling

Ignoring your liquidity needs

It’s important to put your cash to work for you, but it’s also critically important to leave enough cash in your bank account so you have it when you need it. For example, if you need a down payment for a house next spring, or you want to pay your kid’s tuition in the fall, you’re better off not putting that money into long-term stocks because you need it in the near-term. The stock market goes up in the long-term, but it’s volatile in the short-term, and you don’t want to be forced to sell your long-term investments when the price is bad. For example, during the financial crisis from late 2007 through early 2009, the stock market lost half its value, but then regained it all (and a lot more) over the following years. If you’d have sold at the bottom then you’d have missed out on those great returns (and a lot of money) during the rebound. If you need your money in the near-term, don’t invest it for the long-term. Here is another colorful quote from Warren Buffett to explain:

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

5. Yield Chasing

At Blue Harbinger, we often focus on income-investing, however few things frustrate us more than when an investor assumes an investment with a higher yield must be better than an investment with a lower yield. We call this “yield chasing” and it is a bad idea.

Investments with very high yields are often a red flag, and an indication of a company in distress. It can signal a dividend cut on the horizon and potentially even a bankruptcy for the company. Rather than chasing the highest yields, investors should focus on the best yields. For example, we like companies with safe, well-covered yields, and the potential to increase the dividend in the future. Also, critically important, not all income needs to be generated from dividend or interest payments. Prudently selling some of your investment to generate income can dramatically reduce risks, and it can lead to better investment and tax decisions (more on taxes in the next section).

4. Disrespecting Uncle Sam

Ignoring Tax Consequences...

Aside from the obvious (like going to jail for not paying your taxes) there are huge tax mistakes that long-term investors often make that can prevent them for achieving the success they want. For your reference, we’ve listed and described several big tax mistakes that many long-term investors often make.

Choosing a Roth account when you’re better off in a traditional account. The government has set up tax qualified accounts to make saving for retirement easier. However, if you select the wrong type, you are hurting yourself significantly over the long-term. For example, a traditional IRA (individual retirement account) allows you to save for retirement on a pre-tax basis. This way, you’re money will grow faster, and you won’t pay taxes until you retire. On the other hand, a Roth IRA lets you pay taxes up front instead of during retirement. A mistake some investors make is to contribute to a Roth IRA now (instead of a traditional IRA) when they are in the highest tax bracket, and they’ll likely be in a lower tax bracket during retirement. You’re effectively paying more tax dollars than you need to by selecting the wrong type of IRA.

Generating short-term gains without considering the tax consequences is another terrible mistake. Often times investors trade in and out of positions on a short-term basis, and then brag at the end of the year that it was worthwhile because they beat the S&P 500 by a few percentage points. However, short-term gains are usually taxed at a higher rate than long-term gains, and after factoring in taxes, the investor would have been significantly better off with a buy and hold strategy.

Failing to recognize the difference between qualified and non-qualified dividends is another tax mistake. Income from qualified dividends is taxed at a lower tax rate than non-qualified. Investors that don’t pay attention may actually be earning less income then they think, after factoring in taxes.

There are a variety of additional tax-related mistakes that investors often make, and not paying attention to the tax consequences is one of the seven deadly sins of long-term investing.

3. Gullibility

Having unrealistic expectations...

There is an old saying that if something looks too good to be true then it probably is. The terrible mistake and deadly sin that many investor make is to believe things that are just not reasonable. This comes in many different shapes and forms. For example, if your advisor tells you he’s going to outperform the S&P 500 by 10% every year forever, that’s just not realistic. In reality, most investors do not beat the market as measured by the S&P 500 (usually due to unnecessary mistakes and expenses, more on expenses later).

Another unrealistic expectation is to believe your long-term returns won’t be “lumpy.” The market is volatile, and returns come in ebbs and flows. The key is to understand that the market has down years (and so too will your investment account), but you need NOT sell after a down year, but rather stick to your long-term plan. Selling after a market decline is a terrible mistake for long-term investors, and often times it is the exact wrong thing to do.

Being overconfident in your investment skills (or the skills of someone else) is another mistake. And over the long-term, investors that take unrealistic risks will be humbled by the market. The key is to build an appropriately diversified long-term investment portfolio and to have realistic expectations about your returns. And if you are going to work on your investments with someone else, make sure you work with someone you trust.

As an investor, it's very important to have a healthy sense of skepticism. Ask questions often.

2. Concentrating Risks

Poor Diversification...

As we have mentioned before, building an appropriately diversified investment portfolio is a proven strategy for long-term success. That means don’t put your life savings into some small biotech company because your neighbor told you it’s a sure things. And perhaps less obvious, don’t put all your investments in only one industry or sector of the market. For example, many investors make the mistake of chasing after only high-dividend stocks. Others invest in only aggressive growth technology stocks. Both strategies are a mistake because investors can lower their risks by investing across a variety of sectors while still selecting attractive opportunities.

A common diversification mistake is when long-term employees have accumulated a significant amount of their company’s stock through an automatic stock purchase plan. It’s not uncommon to see situations where 25% or even 50% or more of an investor’s wealth is tied up in the stock of one company, and if that company gets taken down by a lawsuit or goes bankrupt then 25% or 50% or more of that person’s life savings is wiped out. Diversification is extremely important, and poor diversification is one of the seven deadly sins of long-term investing.

1. Paying Too Much

Overpaying for your investments is a terrible mistake, and it comes in many different shapes and sizes. For example, investors often pay way too much in trading costs (e.g. commissions, bid-ask spreads, short-term capital gains taxes). These all detract from your long-term investment performance, and if you’re not careful they’ll prevent you from ever achieving your goals. Stop lining the pockets of Wall Street by paying too much in trading costs.

Another example of paying too much is when you have someone unscrupulous manage your money. Many advisors charge very high fees and hidden trading costs, plus they’re often pressured to push you towards certain products that are not necessarily in your best interest. If you are inclined, many investors can do better by investing on their own. However, if you are going to work with a professional then consider working with a fiduciary (the highest standard) instead of a salesperson (someone that gets paid commissions).

Finally, another terrible mistake is simply to ignore valuation when you purchase an investment. Too many investors chase after what has been performing the best lately, and they end up buying right before it crashes. The bursting of the “tech bubble” in the early 2000’s is an example of this danger. There are smart ways to avoid all of these costs and to make your money work harder for you. It’s very important to do your homework so you don’t end up paying too much for your investments.

Conclusion:

At the end of the day, there is hope. Long-term investing is a proven strategy for success. And the power of long-term compound growth is usually not fully appreciated by most investors. If you want to be a successful long-term investor, it’s very important to select the right type of investments, but it can be even more important to avoid mistakes such as the seven deadly sins of long-term investing, as described in this article. Be smart.