Fear is high that a Frontier dividend cut is coming. It's price is down, it's yield (12.4%) seems unsustainably high, and short-interest is among the highest in the S&P 500. However, to a large extent, Frontier does have the ability to control its cash flows and sustain its dividend in the near- and mid-term. The real challenge is that Frontier’s business exists in an anemically eroding marketplace. And if you are attracted to Frontier because of its big dividend yield, then you may want to consider the bonds instead. Many of Frontier’s high-yield bonds offer big interest payments, and they’re far safer than the stock (plus the bonds might get a nice price bump if Frontier’s dividend actually does get cut).

Frontier faces challenges

Frontier faces big challenges. For starters, the company provides voice, video and data services to customers dispersed across the US, often in smaller rural markets where the big boys (Verizon and AT&T) are generally not interested.

The company’s financial wherewithal is being stretched increasingly thin considering the high costs of maintaining its dispersed and neglected networks, its balance sheet debt obligations, and its equity investor’s demands for dividends.

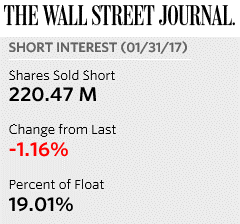

Also, potential increased competition from wireless service providers is threatening. And as further evidence of the challenges facing Frontier, short-interest has recently exceeded 19%, making it one of the most “bet against” stocks in the S&P 500.

Further still, the following chart shows the company’s free cash flows (the money from operations left over after capital expenditures) has recently been negative.

And considering all of these challenges, many investors are left wondering if the big dividend is safe, or if it is heading for a big dividend cut.

Frontier’s dividend is sustainable (for now)…

Frontier’s dividend is sustainable in the short- and mid-term, if the company wants to sustain it. For example, Frontier can skimp on network capital expenditures in the short- and mid-term at the expense of disgruntled customers (remember, Frontier is the only provider in many of the areas it serves). However, Frontier may likely be able to sustain the dividend without further sacrificing services and capital expenditures. As the following graphic shows, the company has plans to strengthen itself in the coming years via cost synergies.

Additionally, Frontier’s cash flows may not be as dire as a basic free cash flow calculation (see earlier FCF chart) suggests. In particular, adjusted free cash flow (and the dividend), as shown in the following chart, is much less stressed.

(For reference, Adjusted Free Cash Flow is defined as free cash flow, as described above and adding back interest expense on incremental debt and dividends paid, prior to the company’s ownership of the CTF operations, on debt incurred and preferred stock issued to finance the Verizon Acquisition).

Also worth noting, the government has a vested interest in supporting Frontier. In particular, the government wants Frontier to keep providing phone and data services in certain dispersed and underserved areas, and that’s why Frontier receives multiple government subsidies. For example, in 2015, $500 million, or 9%, of Frontier’s total revenues were derived from federal and state subsidies for rural and high-cost support, commonly referred to as USF (2015 10-K, p.22).

Frontier’s bonds are better than its stock

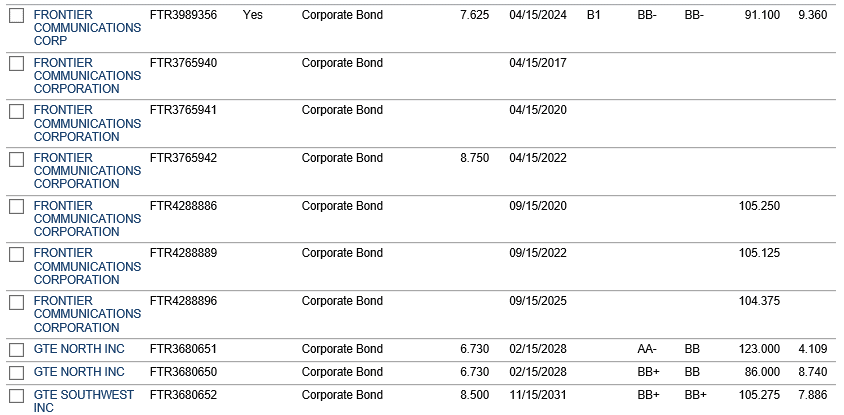

As the following table shows, Frontier currently has a variety of high yield bonds outstanding.

(Source: Finra-Markets Morningstar)

Specifically, many of these bonds offer big coupons and very attractive yields to maturity. And what makes them even more attractive to us is that many of them are far safer than the stock. For example, Frontier has some 2025 bonds that offer 11% interest payments (10.496% YTM). And not only does Frontier have the cash flow to keep paying these bonds now, they have the ability to cut the stock dividend in the future which will free up even more cash flow to pay the bonds if needed. And if Frontier does cut the dividend, the bonds will likely experience an immediate jump in price because the market will perceive the bonds as even safer (i.e. cutting the dividend frees up more cash flow thereby making the bonds safer).

Generally speaking, companies don’t stop paying interest on their debt unless they’re going into bankruptcy, and that’s not the case for Frontier (i.e. Frontier has plenty of business and cash flow to remain a going concern). And as we mentioned earlier, the government has a vested interest in NOT letting Frontier go into bankruptcy (i.e. the government wants Frontier to keep serving the areas that it does, and that’s exactly why Frontier receives all those government subsidies). Unless some hostile takeover occurs, whereby the barbarians intentionally take Frontier into bankruptcy, the bonds are money good (especially considering the government regulators want Frontier to stay in business).

Risks

As we mentioned earlier, Frontier’s business faces a variety of risks that are worth considering. For example, Frontier serves customers in dispersed regions across the US which makes supporting the network expensive. And in many areas, the network has been neglected and requires significant capital expenditures. Other risks include the threat of a reduction in government subsidies, potential competition from wireless providers, costly pension obligations, the costs of unionized workers, and customers angry about the quality of service. However, despite the risks, there are a lot of stakeholders that want the company to remain a going concerns such as the government regulators, the customers that have no other viable phone and data options, and the investors and management that have skin in the game.

Conclusion

If it’s big safe yield that you’re after, consider Frontier’s high-yield bonds, not the stock. Frontier will cut the huge dividend on its stock long before it defaults on its debt. And if you are interested in more companies with big dividends and a high level of fearful investors (like Frontier), consider this list of 40 Big Dividend Stocks with High Short Interest. Lastly, and most importantly, don’t subject yourself to unnecessary risk (unless you want to) such as is the case with Frontier’s stock.