Tumultuous Retail Real Estate:

Unibail is buying Westfield, and Brookfield is trying to buy GGP. Two things that standout about these retail real estate deals is that some investors are starting to see deep value opportunities in the brick-and-mortar stores that are suffering from very real financial challenges driven by growing competition from online retailers (e.g. Amazon (AMZN)), as well as a snowballing negative narrative. The second thing that stands out is that the perceived value is being found in higher quality (more rent and sales per square foot), convenient, experiential properties. In our view, there are lots of valid reasons to believe both trends (FAANG stocks up, retail REITs down) will continue, but if history is any indication, “hot stocks” will eventually underperform, and when the market capitulates, you may be left wishing you had owed a few more high-income, contrarian, retail REIT opportunities. This article reviews five relatively attractive retail REITs that contrarian income-focused investors may want to consider.

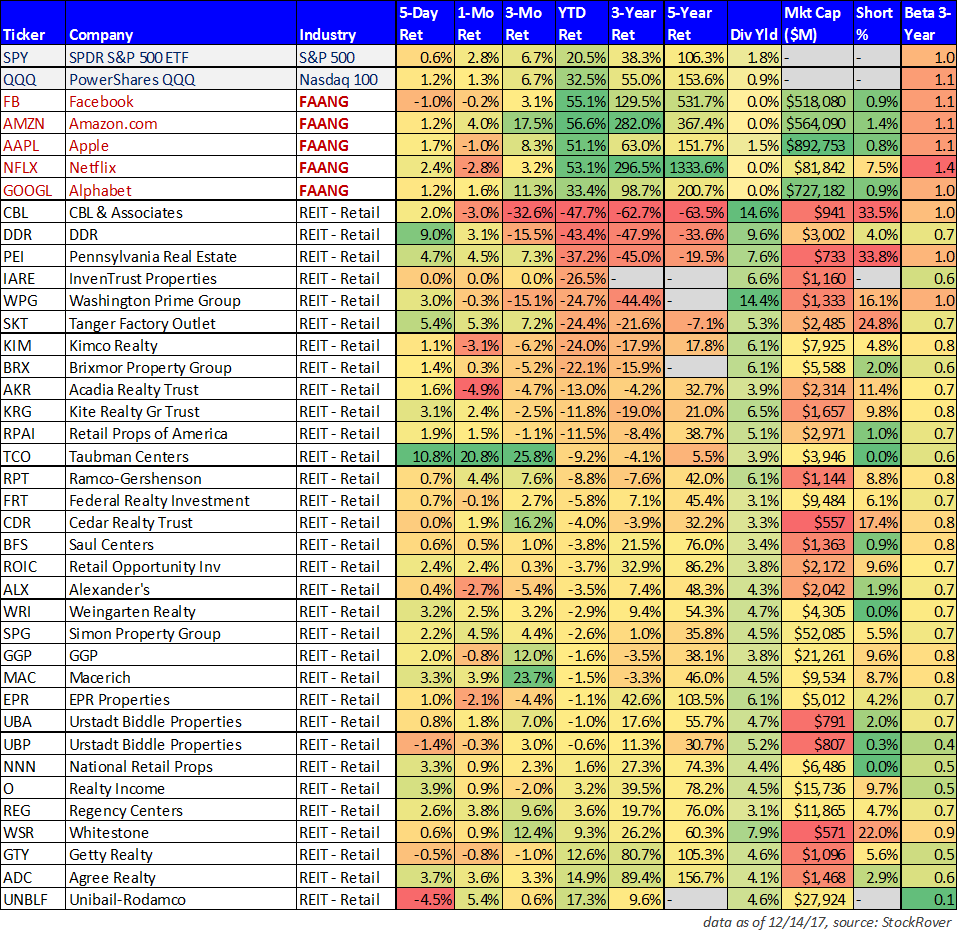

Historical Performance Perspective:

Here is a look at the recent performance (total returns) of retail REITs, Amazon (and other FAANG stocks), and the S&P 500 (SPY).

It should be no surprise that REITs have been performing very poorly, and FAANG stocks have been putting up flashy high numbers. But to put things in perspective, here is a look at what happened to REITs when (and since) technology stocks (as measured by QQQ) sold off so hard in 2000-2002 when the “tech bubble burst.”

As the chart shows, technology stocks sold off very hard, and REITs performed very well. For a little more perspective, here is a look at REITs versus QQQ so far this year.

Keep in mind, the iShares US Real Estate ETF includes a lot of additional REIT categories (e.g. industrial, residential, office) that have performed much better than retail REITs this year (i.e. retail REITs have been even worse, as shown in our earlier table).

We are certainly NOT calling current market conditions as “bubbly” as the original "dot com" era (bitcoin may be getting there though), but we are saying when market sentiment changes (we don’t know when, but it eventually will) a lot of investors will be left wondering why they concentrated all their money chasing growth and not value stocks. For more perspective, here is a look at the historical performance of market styles (i.e. large cap, small cap, value and growth).

And more recently…

What stands out about historical style performance is that value stocks (particularly small cap value stocks) have significantly outperformed over the long-term.

Retail REITs: There Will Be Big Winners, and Big Losers

We are not saying all retail REITs are cheap (they're not), but from a contrarian value standpoint, there is reason to believe certain Retail REITs can coexist very profitably at the same time as Amazon and other online companies and retailers. For some perspective, Amazon recently bought brick and mortar Whole Foods, indicating they certainly don't believe all brick and mortar is dead. Also, Unibail and Brookfield are pursuing acquisitions of Westfield and GGP (thereby indicating there is some value, in their view). And Target recently acquired same day grocery delivery company Shipt, in an effort to provide both brick and mortar and online retail sales channels. The point is that the Internet is NOT going to kill off all brick and mortar stores--that notion is ridiculous.

From our perspective, we like select retail property owners. Specifically, we like the ones that own properties in convenient, experiential locations that receive high rent payments, and own stores with high sales per square foot.

On the other hand, we suspect some of the less desirable property owners (e.g. declining rents, declining sales per square foot) still may not have sold off enough considering the continuing retail evolution. For example, we expect more weak retailers to file bankruptcy and or require rent concessions.

Five Attractive High-Income Retail REITs...

1. Taubman Centers (TCO), Yield: 4.0%

In our view, well-located retail assets can coexist very profitably with internet retailers, and Taubman’s portfolio of properties is among the most desirable. For example, here is a look at Taubman’s sales and rent per square foot relative to its peers.

Among retail REITs, we believe those with less productive locations face the greatest risk of being made obsolete by internet retailers. However, Taubman’s locations provide value and convenient experiences that shoppers will continue to seek out. And considering it currently trades at around 17.1 times the midpoint of 2017 adjusted FFO guidance, we think it’s worth considering if you are a contrarian income focused investor.

2. Simon Property Group (SPG), Yield: 4.4%

Simon Property Group is another one of the retail REITs with more valuable property locations (as shown in our earlier chart), but rather than purchasing shares outright, we’ve generated attractive income by selling out-of-the-money put options (selling insurance) on it each time the negative market narrative flairs up. This strategy, allows us to generate premium income immediately, and it also gives us the opportunity to own the shares at an even lower price if they get put to us. And to be clear, we’d be happy to own SPG at a considerably lower price considering it is one of the retail REITs that owns highly valuable, convenient, experiential locations that can coexist with the internet.

3. CBL & Associates Properties (CBL):

Equity (14.3%) versus Debt (+6.0%)

CBL & Associates Properties is a retail REIT, and its shares often grab the attention of income-focused investors because of their huge 14.3% yield. However, this is a REIT we have no interest in owning because the recent dividend cut is an indication to us that management sees more pain ahead as its portfolio of lower quality retail locations (see rent and sales per square foot in our earlier table) will continue to face challenges. CBL has a very low price to FFO multiple of only 2.9 times ($5.65/$2.10) which we view as a danger, not an opportunity. And short interest of around 33% is another clear red flag, in our view.

On the other hand some of CBL’s debt may be worth considering. Specifically, we don’t expect CBL to go out of business over night, but rather we suspect it could just shrink dramatically, over time. For example, CBL could have more dividend cuts ahead as its less valuable properties continue to decline in value. Another dividend cut would be bad for income-focused equity owners, but it could be a good thing for the debt (bonds). For example, the most recent dividend cut freed up more cash to support the debt, which is ahead of the equity in the capital structure. Given the slow pace that we expect CBL to decline, and the additional cash flow that may become available via more dividend cuts, we think the CBL bonds may actually be worth considering. We wrote about the bonds in more detail here (members-only).

4. Macerich (MAC), Yield: 4.5%

Sticking with our preference for highly valuable, convenient, experiential locations, we believe Macerich is another retail REIT that is worth considering if you are an income-focused contrarian investor. For example, the following graphic shows that Macerich’s rent and sales per square foot remain strong (almost as high as Taubman’s in our earlier chart).

Yet despite the strength, Macerich’s price to 2017 diluted FFO expectatins has declined to 16.7 times as the negative retail REIT narrative has continued. Also like Taubaman, we believe Macerich’s locations will allow it to successfully coexist with Amazon and other internet retailers. In fact, Macerich sees a trend of more online companies moving into brick-and-mortar stores as well, as shown in the following graphic.

5. GGP Inc (GGP), Yield: +3.8%

As a sign of value, as we mentioned earlier, Brookfield Property Partners (BPY) recently made a bid to acquire GGP at $23 per share, and GGP has reportedly rejected the offer (an indication that GGP also believes they are worth more). This bid is consistent with our belief that the retail REITs with better locations have a much better chance of succeeding (and ultimately thriving in the long-term) despite the current internet-driven carnage. As shown in our earlier chart, GGP achieves higher sales and higher rents per square foot than many other less desirable retail REITs. And consistent with our views, GGP’s properties are located in more attractive, convenient, experiential locations than many of its peer’s properties.

Whether or not GGP's rejection of the $23 bid was a good idea is yet to be known. For example, market conditions (both real and perceived) could still get worse before they get better, and GGP may end up regretting its decision to reject the bid. Also, there are some twisted management conflicts of interest in the whole Brookfield Property Partners—Brookfield Asset Management (BAM) relationship that could make GGP and BPY shareholders relatively worse off relative to BAM. For example, we wrote about this in detail in our recent members-only article.

However, assuming Brookfield’s belief is correct that we are closer to a bottom (not a top) in retail REITs (that’s why they’re interested in buying), GGP could have a lot of long-term upside, regardless. Plus, the proposed deal (which may be sweetened) involves what amounts to an immediate dividend increase to GGP shareholders if the deal goes through.

Conclusion:

We believe there will be big winners and big losers in the retail REIT space, and there are attractive ways to play these opportunities with stocks, bonds and options, as described in this article. More specifically, we like high-quality, convenient, experiential REITs that are able to collect high rents on properties that continue to generate high sales per square foot. And based on the recent acquisition efforts, some of the long-term, value-focused, institutional dealmakers agree.

We’re not saying the negative market narrative will change overnight, and there could still be more pain to come. However, if history is any indication, "hot stocks" will eventually underperform (e.g. Amazon and other FAANG stocks), and when the market capitulates, many investors may be left wondering why they didn’t diversify into a few more high-quality, high-income, contrarian, retail REIT opportunities.