HCP Inc. (HCP) is a big dividend (+7.0%) healthcare real estate investment trust (REIT) that is also a dividend aristocrat (i.e. it’s increased its dividend more than 25 years in a row). We believe HCP is interested in maintaining its dividend aristocrat status because it’s the main reason why so many people own HCP in the first place (i.e. they like the big, safe, growing dividend). The recent challenge for HCP in maintaining its big dividend has been a high dividend-to-funds-from-operations (FFO) ratio. Specifically, HCR ManorCare (HCP’s largest tenant, contributing 24% of total revenues) has ongoing unresolved issues that are negatively impacting investor confidence and increasing risk. We believe HCP’s decision to spinoff HCR ManorCare in the second half of 2016 into a separate company (SpinCo) is smart because it will help HCP maintain its dividend aristocrat status (by reducing risk, reducing its cost of capital, and freeing up more cash), and because it will unlock value by allowing for a more customizable risk profile and thereby expanding the potential investor base (i.e. SpinCo may appeal to more investors that would not normally be interested in HCP).

About HCP

HCP, Inc. is a fully integrated REIT that invests primarily in real estate serving the healthcare industry in the United States across five distinct sectors: senior housing, post-acute/skilled nursing, life science, medical office and hospital. Generally speaking, this is not a bad industry to be in from a secular growth standpoint as the US population ages as shown in the following chart.

(Source: U.S. Census Bureau, Population Estimates and Projections).

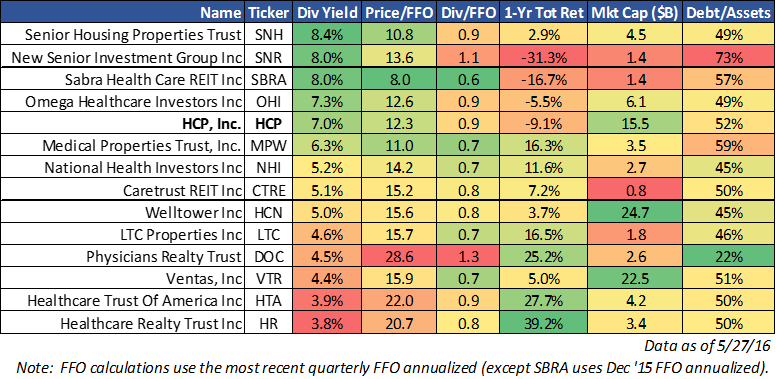

And as the following chart shows, HCP compares favorably to some of its REIT peers in terms of valuation (Price/FFO) and dividend yield. However, HCP’s performance has lagged many of its REIT peers over the last year (-16.7%), and its dividend to FFO ratio is precariously high.

And for further color, here is a graph comparing HCP's dividend per share versus FFO per share.

And the main reason why HCP’s performance has been poor over the last year is HCR ManorCare.

About HCR ManorCare

HCR ManorCare (HCRMC) is HCP’s largest tenant (it accounts for 24% of total revenue), and it continues to be a consistent problem child for HCP. For example, according to HCP’s most recent annual report, HCRMC has been especially challenged in the post-acute space, forcing HCP to concede significant rent reductions while working towards a long-term solution, most likely including additional assets sales and/or rent reductions. In the first quarter of this year, HCP reported an income reduction of $0.11 per share related specifically to HCRMC investments. Generally, speaking, HCP investors are not pleased with the risks HCR ManorCare has created.

Why the Spinoff?

We believe the decision to spinoff HCRMC into a new company (SpinCo) is a smart move by management for multiple reasons. For starters, it will help HCP maintain its dividend aristocrat status. For example, spinning of the troubled HCRMC asset reduces risk and volatility, and increases investor confidence that HCP will be able to continue its track record of dividend increases. It will also reduce the cost of capital (when risk is lower debt is cheaper and more money can be raised with equity) thus increasing HCP’s ability to invest and grow profitably. Additionally, HCP recently explained that there will be debt proceeds raised at SpinCo that will come back to HCP. This will help ensure HCP has plenty of cash to continue paying and growing its dividend.

Another benefit of the spinoff is that it will unlock shareholder value. For example, SpinCo will have a different risk profile than HCP and this will potentially increase the investor base and increase demand for the stock (i.e. higher risk investors that may not invest in HCP may be interested in investing in SpinCo as a stand-alone opportunity). Additionally, SpinCo will be able to do things HCP cannot. According to management, SpinCo will be able to deploy a wide range of strategies, some of which may not be available or practical within HCP.

How to “Play” the Spinoff

The risks of HCR ManorCare (SpinCo) are already baked into HCP’s market price, and the spinoff will work to unlock value by strengthening HCP’s dividend aristocrat status and also appealing to more/new speculative investors via SpinCo. If you currently own shares, we believe there is no reason to sell HCP now or after the spinoff. However, we also believe SpinCo (once it begins trading) will have a different risk profile. Specifically, we expect SpinCo to have higher volatility (and potentially higher price returns) with a lower dividend yield (i.e. it seems unlikely that SpinCo/HCR ManorCare will have the financial wherewithal to support the same high dividend yield as HCP, but that will be up to SpinCo’s new board to decide).

If you own shares now and you’re not comfortable with HCR ManorCare then just sell now. Don’t wait until right after the spinoff because the price will be volatile and it’s unclear if the short-term volatility will work for or against you. Otherwise, just continue to hold (both HCP and SpinCo) for the long-term because, ceteris paribus, the spinoff creates additional long-term value by appealing to a wider investor base which will increase demand, flexibility, and the stock price.

Risks

HCP faces a variety of additional risks, many of which are highlighted in the “Risk Factors” section of the company’s most recent annual report. For example, healthcare reform notably affects the operations of HCP and its tenants. Additionally, the strong growth enjoyed at HCP’s senior housing operating assets could slow as levels of new competitive supply and uncertainty grow. Also, tenants of HCP’s life science portfolio include many pharmaceutical, biotech, and tech companies, industries which historically possess greater volatility. HCP is certainly not without risks, however we believe the risks will be reduced once the HCRManorCare spinoff has been completed.

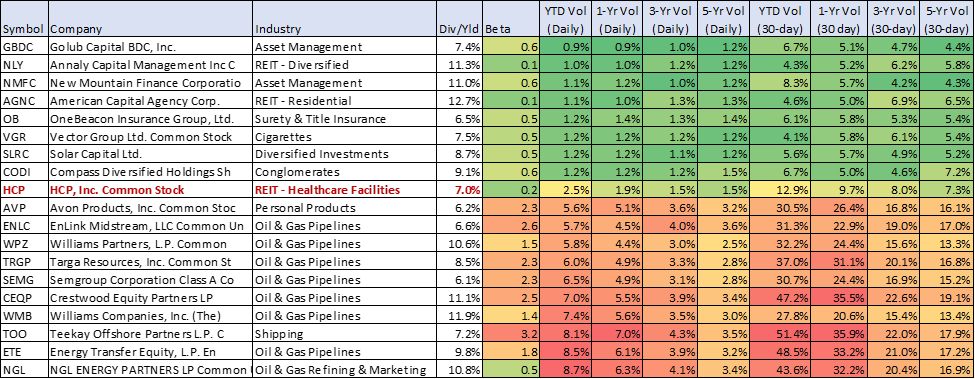

Quantitatively speaking, we like HCP’s very low beta, and we are comfortable with its historical level of volatility as shown in the following chart of a variety of other big dividend stocks.

(click here for unabridged version of this table).

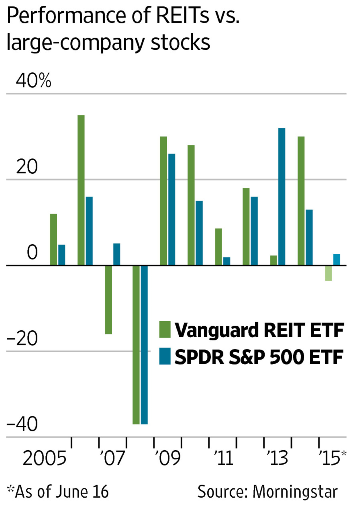

It may also be worth considering how REITs fit into your larger investment portfolio. For example, it is true that historically REITs have offered a lower correlation with other stocks, which has helped reduce big swings in the value of many investment portfolios (see chart below).

Conclusion

We like HCP’s big dividend, risk profile, and long-term prospects. In fact, we like HCP so much that we’ve ranked it #17 on our list of 20 Big Yield Investments Worth Considering because we believe the spinoff will unlock value. Specifically, SpinCo makes HCP’s dividend aristocrat status safer, and it also attracts a wider overall investor base. If you are a long-term income-focused investor, HCP is worth considering.