Passively managed Exchange Traded Funds (ETFs) are a popular, low-cost, way to invest. The growing conventional wisdom is that they are a far better option than high-cost actively managed funds which tend to underperform anyway. In fact, over the last 12 months investors have pulled more than $175 billion out of active funds, and they’ve added close to $435 billion to passive funds.

For reference, actively managed funds (such as mutual funds) are those that rely on professional stock pickers to try to pick stocks that will outperform a benchmark (such as the S&P 500), whereas passive funds (such as ETFs) simply buy everything in the benchmark and end up closely matching the benchmark’s performance (generally speaking).

Recent data from Morningstar shows that over the last 10 years, 73% of actively managed funds have underperformed their benchmark (this is a very bad thing considering active fund managers are generally paid very high fees because they’re supposed to outperform their benchmark). However, before you go dumping your hard-earned savings into ETFs, here are the top ten ETF mistakes and misconceptions we come across that you may want to consider...

- You can’t own too many ETFs. Wrong. For starters, consider the most popular ETF in the world, the SPDR S&P 500 ETF (ticker: SPY). Its annual expense ratio is 0.0945% (9.45 basis points). However, instead of buying the entire SPY ETF, you can buy any one of the eleven sector ETFs that collectively add up to SPY. For example, Energy (XLE), Financials (XLF) or Health Care (XLV). However, the fees for each of the sector ETFs are 14 basis points (48 percent higher than SPY). And if you’ve ever opened the pages of Barron’s or turned on CNBC, you can’t go 30 seconds without seeing an advertisement for these sector ETF’s. The advertisements usually say something like “Do you like Pfizer and Johnson & Johnson? Why not buy the whole Health Care Sector ETF…” The advertisements go on to explain the importance of diversification. But if they really believe in diversification then why not just buy the entire S&P 500 ETF (SPY)? SPY is more diversified and it costs less. The reason is because they really don’t care about you and your investments, they just want to get more of your money. Further, the advertisements are implicitly encouraging you to trade more often. This active trading strategy is generally a bad idea because, as we mentioned earlier, active strategies (e.g. trading in and out of sector ETFs in this case) generally underperform passive strategies (e.g. buying and holding the entire S&P 500 ETF). Plus, active trading piles on transaction costs, and it often results in you being out of the market at certain times whereby you miss out on returns. If you are truly a smart, long-term investor, then don’t get taken to the cleaners by frequently trading in and out of over-priced, under-diversified ETFs.

- All ETFs are diversified. As we’ve alluded to above, this is completely incorrect. There are literally thousands of ETFs out there, and many of them are very specific and not diversified. In addition to the sector ETF’s we mentioned above, there are also country-specific, style specific (e.g. dividend-focused, triple-levered, inverse market exposure) and market-cap specific (e.g. small cap, mid cap, large cap) ETFs, to name a few. You could buy several hundred of these concentrated ETF’s and still not be diversified. Plus many specific ETF categories charge much higher fees than they’re worth. For most investors, your best ETF option is to buy large, broadly diversified, low-cost ETF’s, such as SPY.

- All ETFs have low fees. Not true. We highlighted (above) the higher fees of sector ETFs versus their aggregated parent ETF (SPY), but in perspective the fees of those ETFs are small compared to some of the others. For example, there is a “High Income ETF” (ticker: YYY) that charges nearly 2% in annual fees/expenses. (prospectus, p.1) This ETF index is comprised of 30 closed-end funds ranked highly according to fund yield, discount to net asset value and liquidity. We believe this ETF’s ticker is appropriate because “why, why, why” would you ever pay this much for an ETF? (We’ll talk more about “discount to net asset value later). Another overpriced ETF is Daily Gold Miners Bull 3x Shares (ticker: NUGT) that charges a fee greater than 1% (prospectus, p.1). This completely flies in the face of the idea of diversified, low-cost, long-term investing that many investors expect from ETFs. ETFs like NUGT are simply designed to extract money from investors by sensationalizing popular punditry. Plus NUGT doesn’t always do what it’s supposed to do anyway.

- All ETF’s do what they’re supposed to do. Another common misconception is that ETF always do what investors expect them to do. For example, NUGT (mentioned above) and it’s inverse ETF DUST seek daily investment results, before fees and expenses, of either 300% or 300% of the inverse (or opposite) of the performance of the NYSE Arca GoldMiners Index. However, a quick view of performance on the ETF company’s website shows that, over the course of a year, the actual performance can be quite different with NUGT down 79% and DUST down 38%. One should be up and one should be down, and fees cannot reasonably account for this huge tracking error.

- ETF’s are always fairly priced. Yet another common misconception is that ETFs are always fairly priced in the market. In reality this is not true. For example, ETF’s generally have a net asset value (NAV) based on the aggregated value of all the assets they hold. However, ETF market prices can deviate from their NAV’s and trade at significant discounts and premiums. Unsuspecting investors often buy into ETF’s at premiums and then sell them at discounts, and then they can’t figure out why their investment performed so poorly. To be on the safe side, most investors should stick with larger, more liquid, ETFs because they generally don’t trade at significant discounts or premiums. You can also view the historical discounts and premiums on many ETF provider websites.

- ETF’s make it easier to trade market themes. In reality, most investors are not as smart as they think they are. This is evidenced in the active management underperformance statics provided above. The truth is that ETF companies often market theme-based ETF’s so they can charge higher fees and so they can encourage more trading (which results in more fee income for the companies). Our advice is don’t let some media pundit or ETF marketer pressure you into trading all the time. This generally results in less money for you and more money for them. Investing in diversified, low-cost ETFs for the long-term is generally a far better option.

- It doesn’t cost extra for an advisor to buy an ETF for you. Not true. Just because it’s an ETF doesn’t mean it’s low cost. We saw examples of this above (some ETFs charge very high fees), but it also can apply to financial advisors. Historically, some companies have offered advisor class ETF’s with built in higher fees so your advisor can get a cut of your money. We recognize there are some very good advisors out there that are worth their weight in gold, but if you are truly a long-term investor then you’re probably better off simply buying a well-diversified, low-cost ETF (such as SPY) instead of letting an advisor buy it for you. As we’ll see later, advisor fees can add up to a truly enormous amount of money over the long-term due to the amazing power of compound growth.

- ETFs don’t have misleading names. In reality, it’s important to do your homework before buying an ETF because their names can be misleading. For example, we saw (above) how “3x” ETFs don’t always deliver 3x performance over the long-term. As another example, a popular ETF is the iShares MSCI World ETF. And while the name may suggests the ETF invests in a basket of stocks from all around the world, in reality it excludes emerging markets which are a very significant portion of the global economy. It’s important to understand what you are investing in before you invest.

- ETFs don’t cause individual stocks to be mispriced. Wrong again. A growing complaint we hear from small cap investment managers is that prices are being driven by ETF trades. Many small cap stocks are less liquid, and the majority of their trading activity is the result of big ETF buys or sells that have nothing to do with the underlying fundamentals. This can cause significant price moves as well as significantly mispriced stocks (i.e. babies are getting thrown out with the bath water, and vice versa).

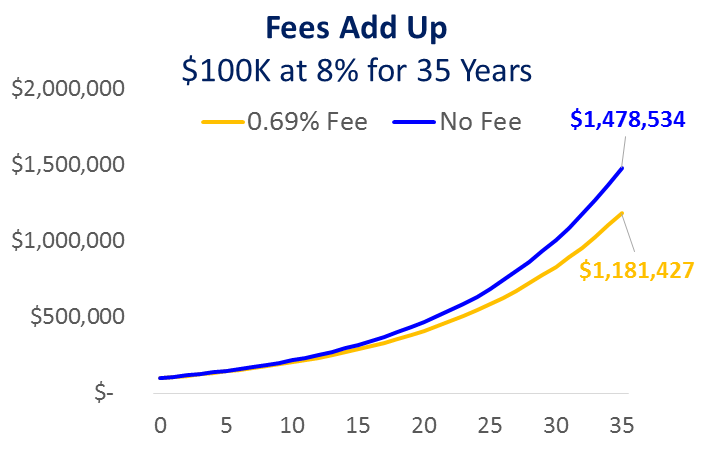

- Owing ETFs is cheaper and less risky than owning individual stocks. Given the chronic underperformance of actively managed mutual funds versus ETFs (per the data above), many investors have concluded that ETFs are the end-all, be all nirvana of investing. Not so fast. While passive ETFs may be better than active mutual funds in many regards, let’s not forget that ETFs exist so some business can make money. According to the Morningstar article, the average fee among passively managed index funds and ETFs is 0.69%., and over the long-term that really adds up. For example, if you have $100,000, a 35-year investment horizon, and we assume an 8% annual rate of return, then a 0.69% annual fee robs you of $297,108. That’s a lot of money!

Alternatively, even if you have no stock-picking ability whatsoever, if you simply construct a long-term investment portfolio of 30+ stocks diversified across market sectors and capitalizations (i.e. it’s not market-cap weighted), then you’ll very likely outperform a passive broad market ETF by at least $297,108! That’s because the benefits of diversification become statistically negligible after your portfolio has more than 25-30 well-diversified holdings (check out this paper for a detailed explanation: Risk Reduction and Portfolio Size: An Analytical Solution). It’s also why random portfolios constructed by monkeys almost always beat expensive active managers (check out this paper for a detailed explanation: The Surprising Alpha From Malkiel’s Monkey and Upside-Down Strategies).

Conclusion: ETFs are a decent way to invest if done correctly. Heck, even Warren Buffett gives instructions in his will to use an ETF for his wife’s benefit:

"Put 10% ... in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard’s.) I believe the trust’s long-term results from this policy will be superior to those attained by most investors – whether pension funds, institutions or individuals – who employ high-fee managers." (Source: 2014 Berkshire Hathaway Letter to Shareholders, p.20).

Specifically, if you’re going to invest in ETFs, and you want to avoid many of the common ETF mistakes, we like broadly diversified, highly-liquid, low-cost, long-term, ETF investing.

For more information on our ETF investing strategies, check out our Blue Harbinger Lazy Person Portfolio.