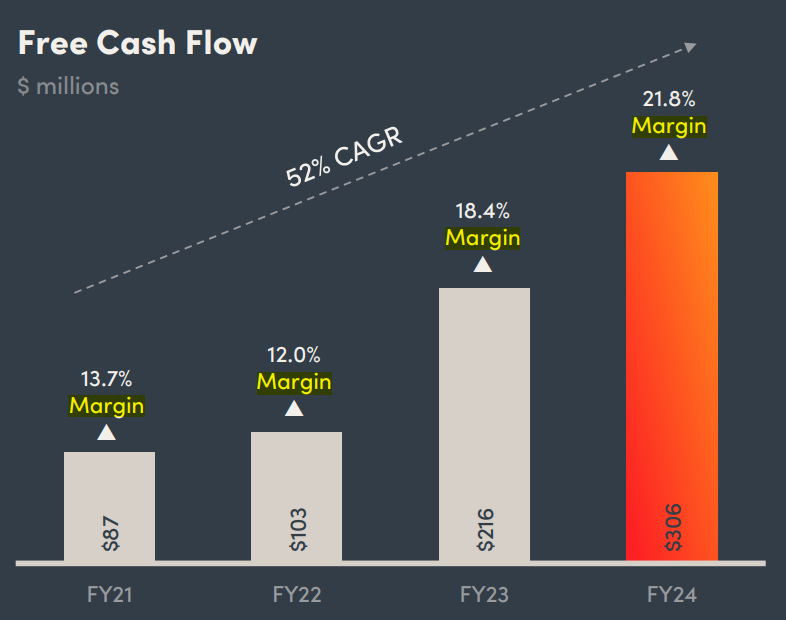

Quick Note: Paylocity (PCTY) beat earnings and revenue expectations, and the shares are up. However, Paylocity shares have been so beaten up for so long (they’re still down ~50% from the 2021 high, thanks in large part to its focus on small-and-mid-sized businesses as customers) that some people haven’t noticed the fundamentals have never stopped improving. Revenue keeps growing, margins keep expanding and the market opportunity remains large (especially as the rotation from large cap to small and mid cap continues).

Trading at 7.6x EV/Sales, with 68% gross margins and a 23% revenue growth rate (in a large total addressable market), Paylocity is very attractive (especially considering its high-renewal land-and-expand business model.

Here is what CEO Steve Beauchamp had to say during the quarterly call:

Our differentiated value proposition of providing the most modern software in the industry continues to resonate in the marketplace and help drive recurring revenue growth of 15% and total revenue growth of 16% in Q4. For fiscal 2024, recurring revenue grew 17% over fiscal 2023, and total revenue grew 19% and finished at $1.4 billion.

Our solid results were once again driven by both adding new clients and employees and increasing average revenue per client. We ended fiscal 2024 with 39,050 clients compared to 36,200 at the end of last fiscal year, an increase of 8%. Additionally, our average number of employees per client increased to over 150 given our continued upmarket success. Average recurring revenue per client was nearly $33,000 in fiscal 2024 compared to just over $30,000 in fiscal 2023, an increase of approximately 8% as a result of increasing product attach rates across our client base.

We are long PCTY in our Blue Harbinger Disciplined Growth Portfolio.