This big-dividend hidden gem of a BDC may be popular in certain niche investment circles, but if you haven’t considered it previously, it is attractive and worth a closer look. It has many of the important qualities you’d like to see in a BDC (such as internal management, strong NII and a healthy dividend), plus the growing macroeconomic interest rate risks are already baked in—to a significant extent. In this report, we dive into the important details (ahead of its upcoming earnings release on January 31st), and then conclude with our opinion on investing.

Overview: Capital Southwest (CSWC)

CSWC is a middle-market lending firm focused on supporting the acquisition and growth of middle-market companies across the capital structure. The company is based in Dallas Texas, it was formed in 1961, and it elected to be regulated as a BDC in 1988. It is publicly traded (on Nasdaq). And importantly, Capital Southwest is internally managed (this eliminates the conflicts of interest that plague many other BDCs), and CSWC has RIC tax treatment for U.S. federal income tax purposes (CSWC can basically avoid corporate income tax if they pay of 90% of income in dividends). Also noteworthy, in September of 2015 CSWC completed a tax free spin off of CSW Industrials (CSWI), and this helped clean up the business (so it could focus on lending to middle-market companies, instead of equity investments). Also noteworthy, in April 2021, CSWC received an SBIC license from the U.S. Small Business Administration (this provides some loan support, thereby opening up new attractive risk-reward lending opportunities). Also, CSWC has only 24 employees (the market cap of the business is only around $550 million—it’s a smaller small cap), and total balance sheet assets were $867 MM as of September 30, 2021. Lastly, and importantly, CSWC also manages the I-45 Senior Loan Fund (“I-45 SLF”) in partnership with Main Street Capital (MAIN).

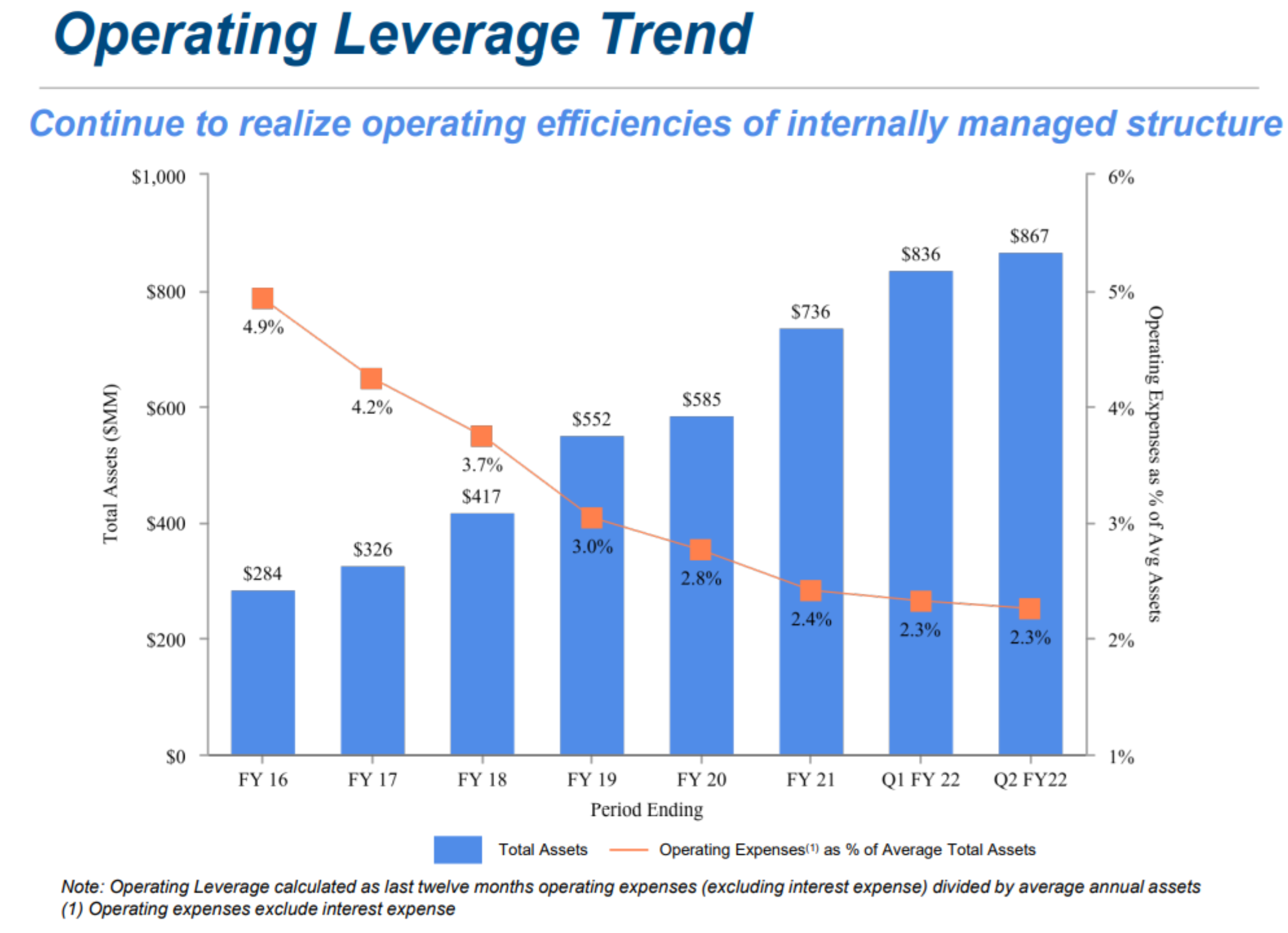

Also worth noting (considering CSWC’s small size versus some other BDCs), the company continues operating efficiencies (thanks to its internal management structure) that continue to flow through to its bottom line.

Capital Southwest’s Investment Strategy

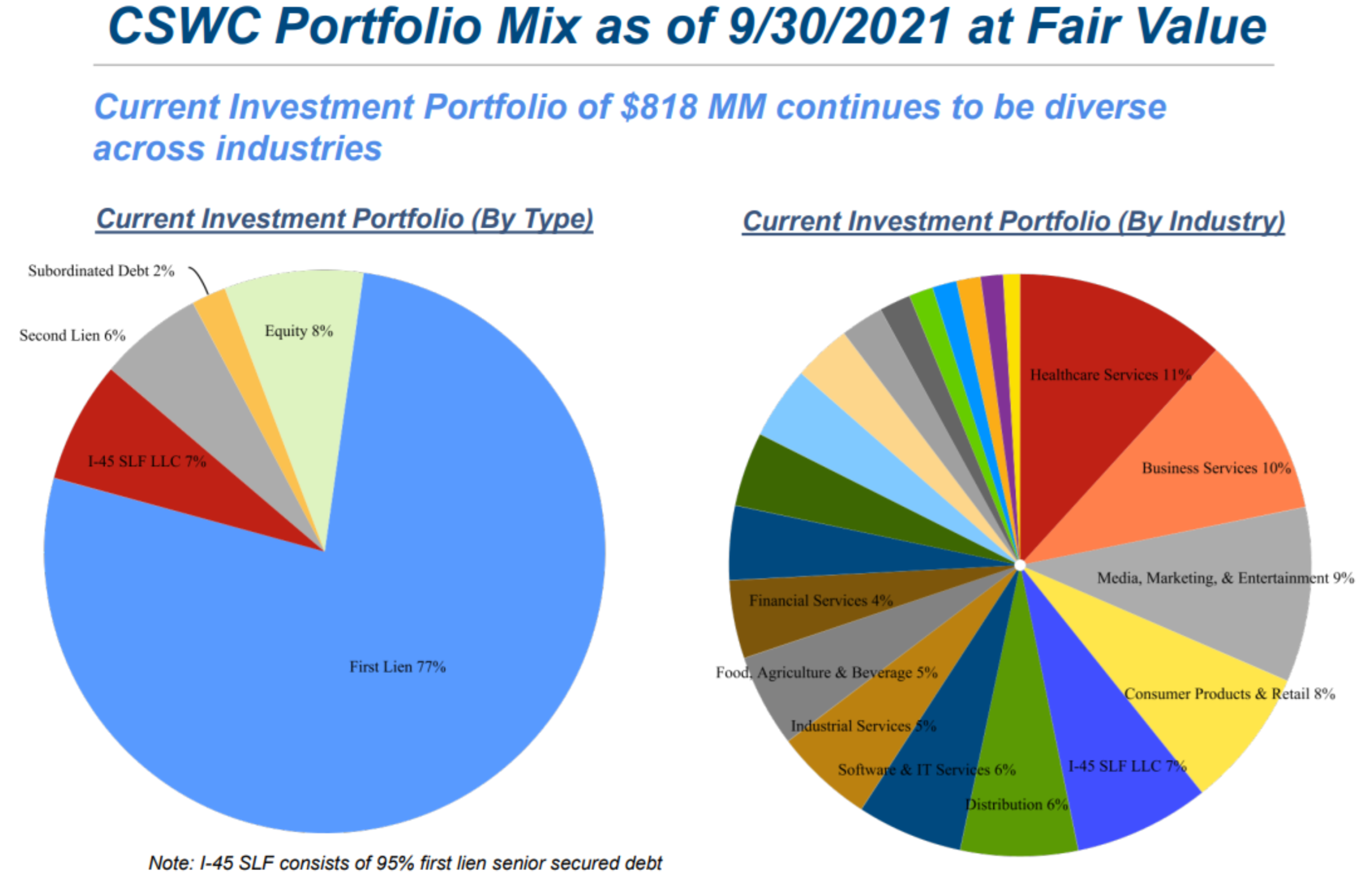

The company’s core lending business is focused on lower middle market (“LMM”) in what it terms (CSWC led or Club Deals). These are typically companies with EBITDA between $3 MM and $20 MM, and typical leverage of 2.0x – 4.0x Debt to EBITDA (through CSWC’s debt position) They make commitment sizes up to $30 MM (with hold sizes generally $10 MM to $25 MM), including both sponsored and non-sponsored deals. Securities include first lien, unitranche, and second lien. And the companies frequently make equity co-investments alongside CSWC’s debt.

The company’s opportunistic business is focused on upper middle market (“UMM”) in syndicated or club, first and second liens. Companies typically have in excess of $20 MM in EBITDA; and typical leverage of 3.0x – 5.5x Debt to EBITDA (through CSWC’s debt position). Hold sizes are generally $5 MM to $15 MM, including floating rate first and second lien debt securities. These types of investments are generally more liquid assets relative to LMM investments. And this provides flexibility to invest/divest opportunistically based on market conditions and liquidity position.

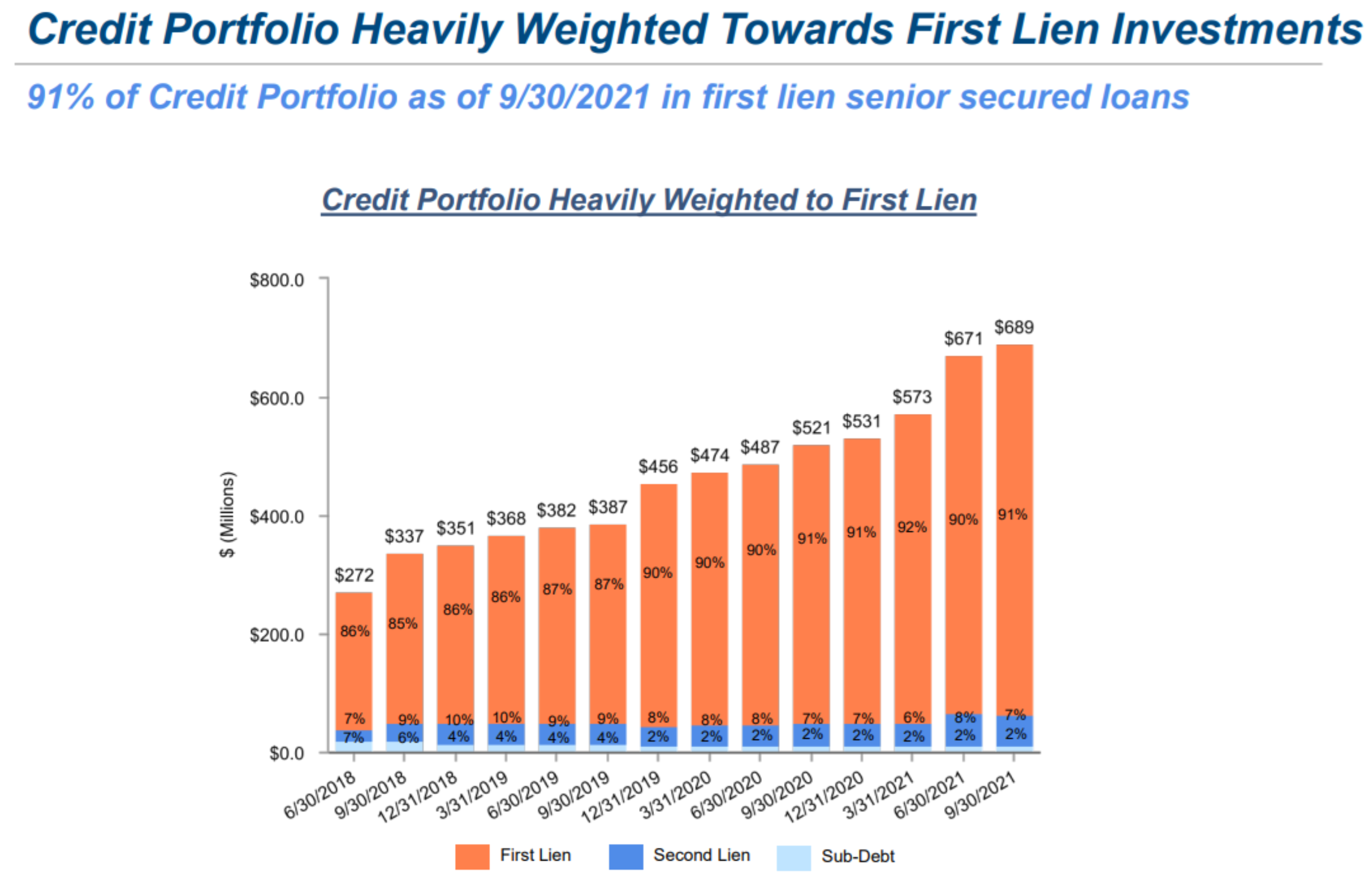

Importantly, Capital Southwest’s credit portfolio is heavily weighted towards first lien investments, which are less risky than second lien investments.

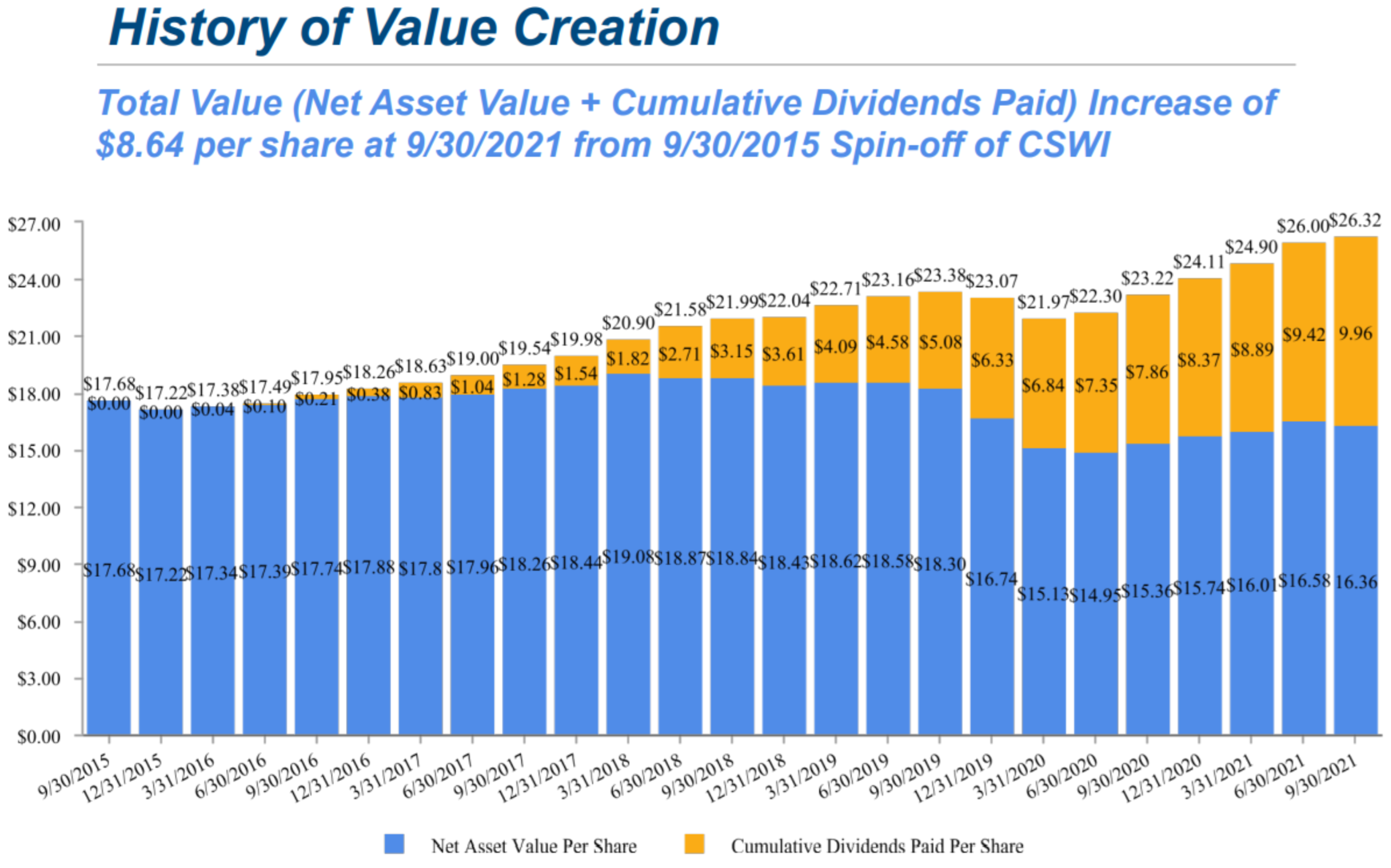

And the company has a strong history of value creation, which is not a guarantee of future performance, but it is still nice to see and adds confidence consider the longevity of the existing management team at CSWC.

Also encouraging, CSWC continues to be active in both originations and investment “exits,” a sign of healthy market conditions and opportunities for the business. For example, in the most recent quarter, CSWC had $112.9 MM in total new committed investments to six new portfolio companies and four existing portfolio companies, and $60.9 MM in total proceeds from six portfolio company exit.

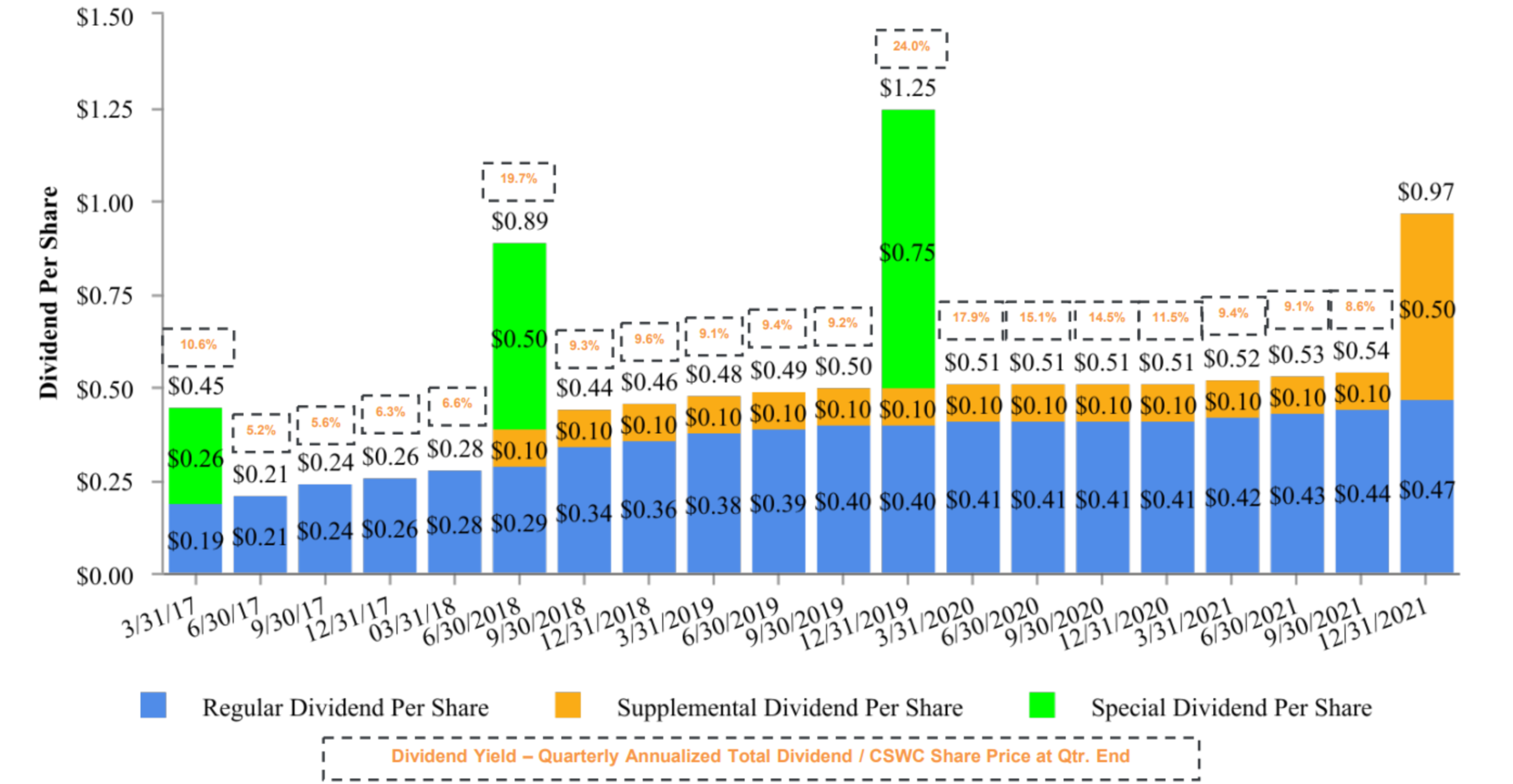

Track Record of Consistent Dividends Continues

Another encouraging characteristic of Capital Southwest is its track record of consistent and healthy dividends. For example, over the last 12 months (ended 9/30/21), CSWC generated $1.85 per share in Pre-Tax NII and paid out $1.70 per share in regular dividends. Furthermore, the cumulative pre-tax NII regular dividend coverage has been 107% (over 100% is good) since the 2015 Spin-Off. And very importantly, the total special and supplemental dividends of $3.41 per share since the 2015 Spin-Off. Also, there was undistributed taxable income ("UTI") of $0.69 per share as of September 30, 2021.

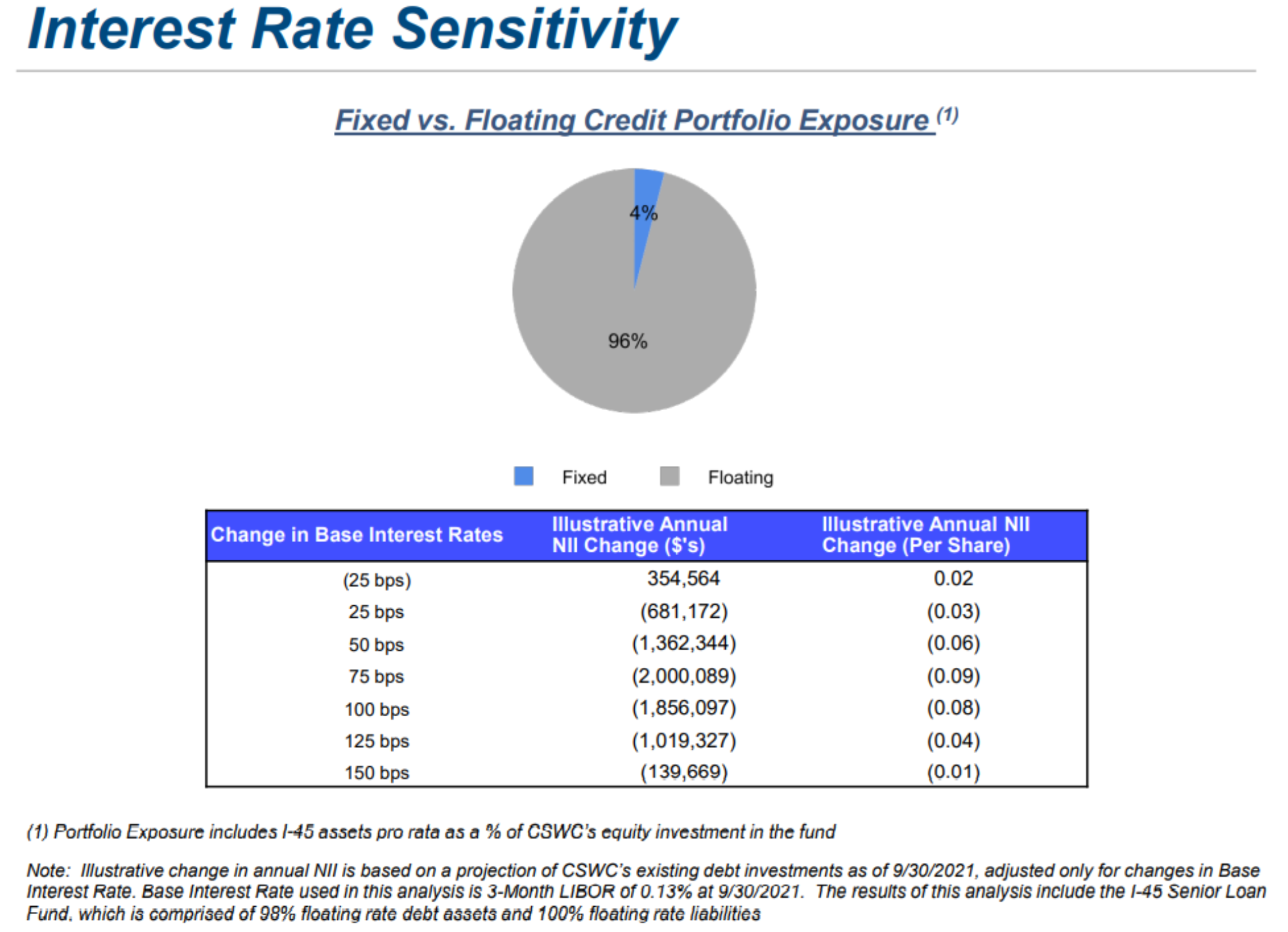

Interest Rate Risk

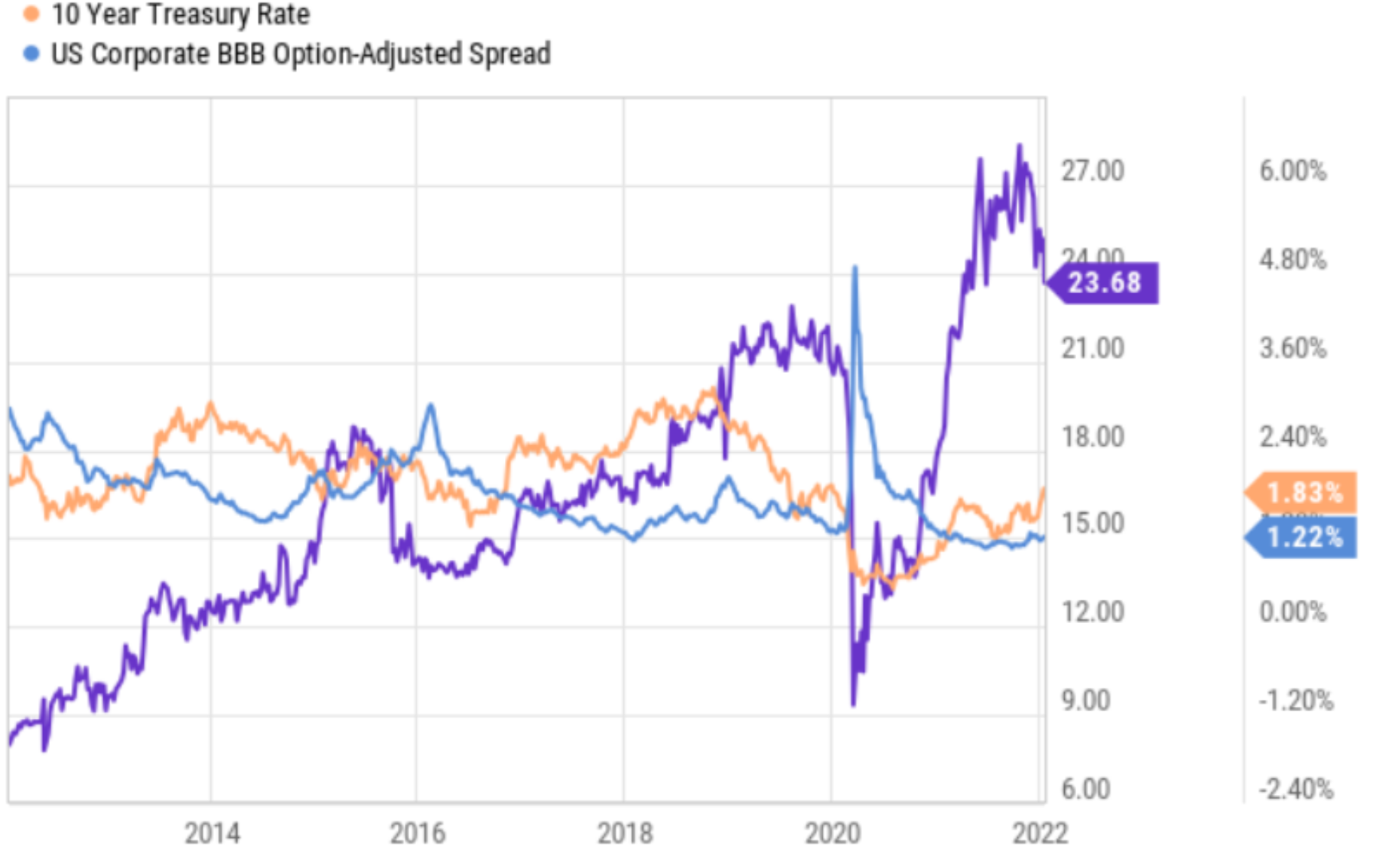

The big macroeconomic risk that currently has investors concerned across almost all markets is interest rate risk. Specifically, the US fed is on a trajectory to begin raising interest rates in March (with 3 hikes expected this year) while they simultaneously slow down the quantitative easing be open market bond purchases. This increasingly hawkish stance by the fed has had the impact of spooking stock market investors, as markets have broadly declined so far this year. This is also concerning for Capital Southwest’s business, considering debt (borrowing) is impacted by interest rates and it is at the core of everything Capital Southwest does.

Here is a look at the company’s estimate of its sensitivity to interest rate changes.

As you can see above, CSWC is negatively impacted by rising interest rates because it has slightly more exposure to floating rates on the expense side than on the revenue side. However, given the recent decline in the share price of the CSWC, rising interest rate expectations are already significantly baked into the shares. If the fed becomes slightly more hawkish on rates, that could be a negative impact on CSWC shares, but if the fed becomes slightly more dovish then that would be a benefit to the shares. This is typical to financial companies, such as CSWC. Also noteworthy, CSWC is even more sensitive to credit spreads than interest rates because the portfolio consists of higher yield (higher risk loans). So in a volatile market, where credit spreads widen—CSWC would like sell off (likely temporarily), but the dividend would likely remains consistent as it has throughout its history.

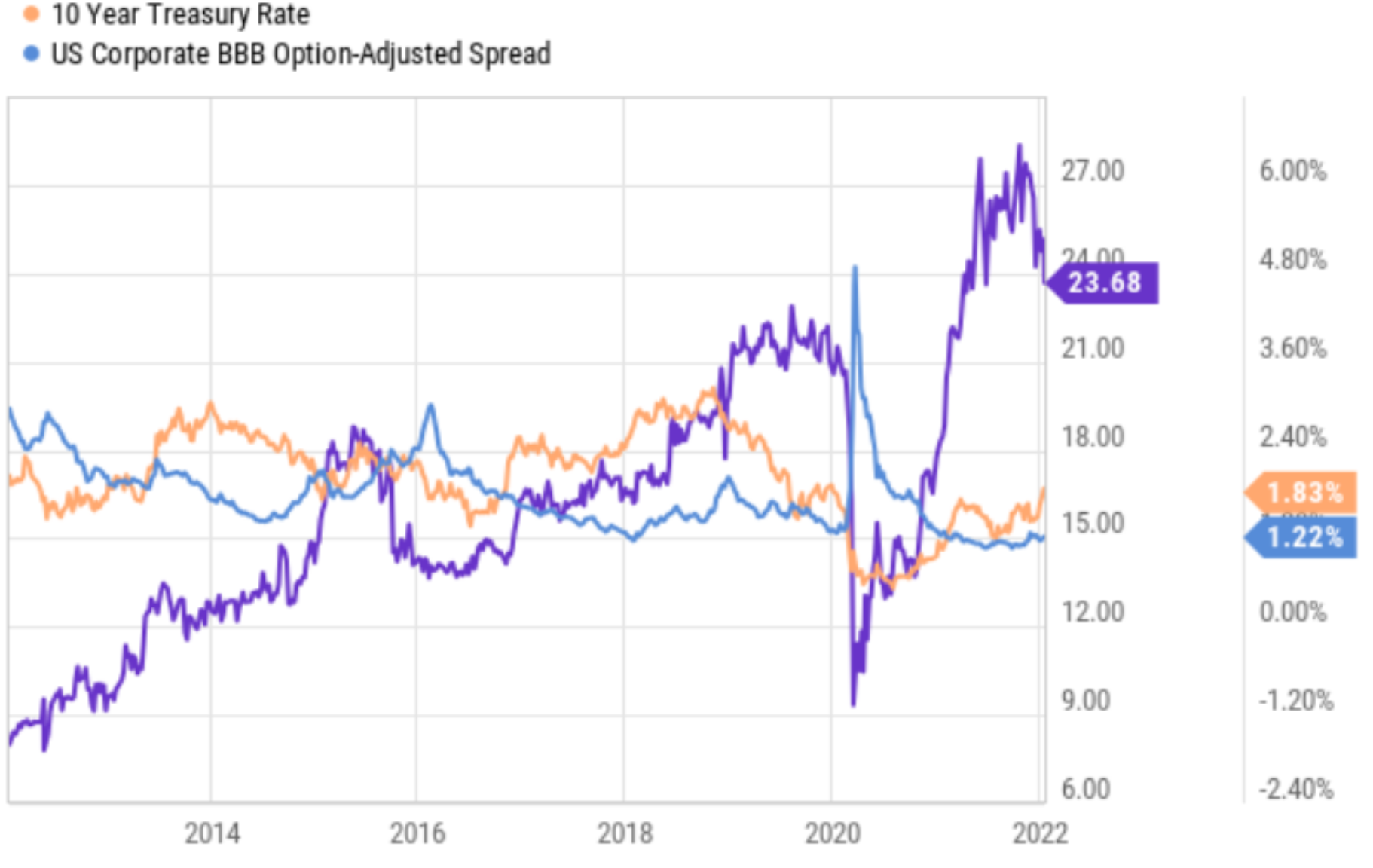

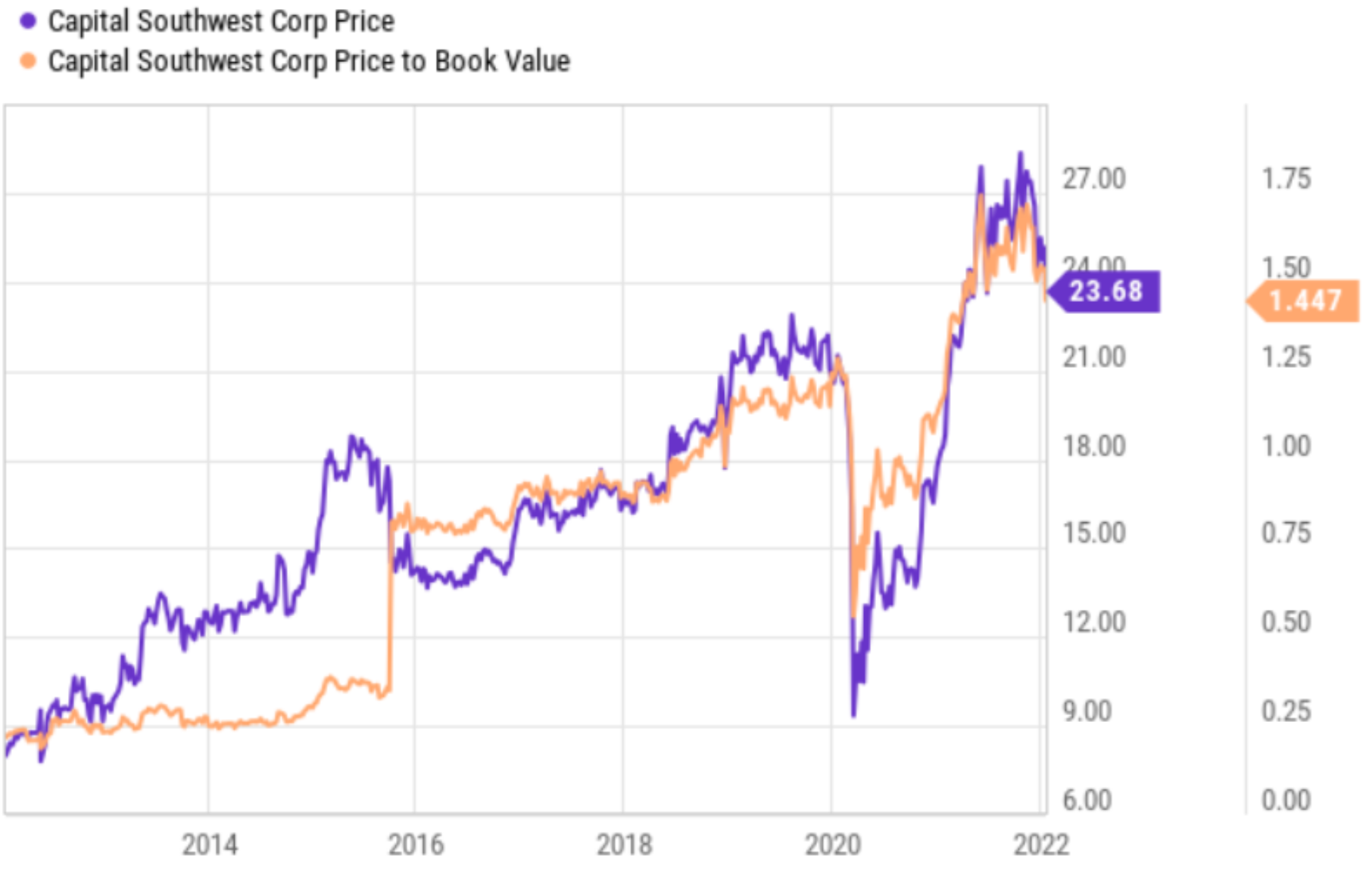

Purple Line is CSWC’s share price

Regarding valuation, BDCs often trade in conjunction with their book value. In the case of CSWC, the valuation increased following the 2015 and it has recently pulled back as interest rate expectations have increased while credit spreads remained low/healthy.

The Bottom Line

If you are looking for hidden gem of a BDC, Capital Southwest is worth considering. It is smaller than many BDCs which arguably excludes the “economies of scale” advantages that larger companies have. However, this is significantly offset by the lower costs of its internal management team, as well as its small business license (something that can move the needle for a smaller BDCs, but not for a larger one). The strength of the portfolio and healthy dividend are also highly encouraging, and the recent dip in share price makes for an even more compelling entry point. Depending on how the January 31st earnings announcement goes, this one is worth considering for a spot in your prudently diversified long-term investment portfolio.