The market has been ugly. But as they say, this too shall pass. And when it does, the most attractive buying opportunities will be gone. No one knows the exact timing of when the turmoil will end, but there are currently a lot of REITs trading at compelling prices (there is enormous fear baked in) and offering unusually attractive big dividend yields. And it’s those big dividends that can give you the steady income you need while you wait patiently for the long-term price gains to come to you. This report counts down our top 10 big-dividend REITs.

Before getting into the rankings, it’s worth considering what is happening in the market and how that is impacting REITs in multiple ways. The three big things spooking the market right now are (1) the coronavirus, (2) plummeting energy prices, and (3) the general notion that Mr. Market was getting frothy and looking for a reason to correct. The impact of lower interest rates on REITs is also worth considering.

The Coronavirus

The market’s reaction to the coronavirus is more than just fear. There are very real impacts to the economy that will impact all stocks in varying ways. For example, most major sporting events (e.g. the NBA, March Madness) have been cancelled. That’s a lot of tickets sales, concession sales and advertising dollars that have now vanished into thin air. Similarly, hoards of people are cancelling airline tickets and non-essential travel. With regards to REITs, there are specific cases of coronavirus outbreaks at senior living properties owned by popular REITs. Also, foot traffic at shopping malls (and shopping mall REITs) will be impacted as more people practice social distancing. Those are just a few examples, and the full list is extremely wide-ranging. The impacts of the cornavirus to the economy are no joke.

Energy Prices

You may think the plummeting price of oil has nothing to do with REITs. But it does. First of all, it has most certainly contributed to the market fear and selling that has impacted all stocks (including REITs). Further, it impacts certain geographical regions more than others (for example, the sub-economy of the Houston-area can be more impacted by the energy price slump because of the significant exposure to the energy sector in that region).

Market Valuation

The market hadn’t gone straight up for 10 years following the financial crisis, but it was fairly close, and valuations were getting very frothy by multiple valuation metrics. We’re not going to spend too much time on this one because frothy valuations can get frothier, and cheap valuations can get cheaper. Nonetheless, it almost seemed as if the market was just looking for an excuse to blow off some steam, and it certainly found it in the coronavirus and plummeting energy prices. However, we will say that disciplined long-term investing has proven to be a winning strategy over and over again throughout history, and there are a lot of attractive big-dividend REITs out there right now.

Interest Rates

Interest Rates are a huge factor for REITs. And in relatively short order, the market has gone from expecting rising rates, to the opposite. Rates were recently cut 50 basis points, and the US Twitter-In-Chief wants more (to make America more competitive around the globe). REITs rely heavily on the capital markets to fund growth, and lower rates makes funding that growth cheaper. Further, as investors are starved for yield (US treasuries certainly don’t yield what they used to), REITs can become relatively much more attractive for income-focused investors.

The Top 10 Big-Dividend REITs

The names on our list are wide-ranging. And in our view, they are very attractive if you are an income-focused investor that likes to “buy low.” However, it’s also important to remind investors of the importance of diversifying your investments across multiple big-dividend categories, as well as to focus on some long-term capital gain opportunities too. At Blue Harbinger, we do our best to write about attractive opportunities from across multiple categories because prudent diversification can help keep risks lower and returns higher.

Without further ado, here are our top 10 big-dividend REITs.

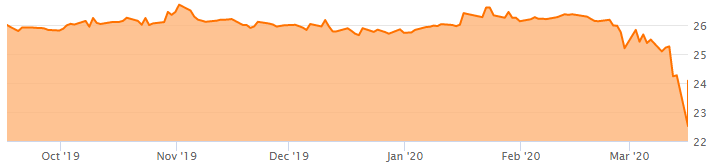

10. Brookfield Property REIT (BPYU), Yield: 11.6%

Like a lot of REITs right now, Brookfield is interesting because as the price has fallen (for mainly the reasons described earlier) the dividend yield has mathematically risen significantly (plus the company just recently boosted its dividend payment by a small amount too).

There are lots of additional attractive qualities about this one, such as its price discount versus NAV, portfolio diversification and demand for its core assets. We don’t own Brookfield (we own many other names on this list), but we like it (it’s on our watchlist). And the main reasons we haven’t ranked it higher on our list include its relatively high debt and ongoing potential bankruptcies of its many tenants (in addition to office properties, retail is Brookfield’s other main property type, and that faces challenges related to secular consumer shopping habit changes, mainly the growth of online shopping, plus the current dramatic aversion to the coronavirus). Overall, we view Brookfield as presenting a relatively attractive buying opportunity considering its current price and dividend yield. You can access our full report on Brookfield here.

9. Gladstone Preferred Shares (GOODM), Yield: 7.3%

If Brookfield is attractive, but one of the riskier names on our list, we’re offsetting it with a less risky opportunity in the form of REIT preferred shares. Specifically, the preferred shares of Gladstone have recently fallen only slightly amongst the market turmoil.

More specifically, they’re far less volatile than other opportunities because they’re preferred shares (higher than common shares in the capital structure). We also like them because they pay dividends Monthly and the company has been strengthening its balance sheet. Further we have less relative concern about Gladstone’s business as it is an office and industrial REIT (still commercial real estate, but not the big retail exposure of Brookfield and others). For more detail, be sure to check out our recent full report on Gladstone preferred shares here.

8. Iron Mountain (IRM), Yield: 10.0%

Some investors are afraid of Iron Mountain because its main business (it’s the market leader in physical storage and document retrieval REIT) seems outdated compared to other newer REITs (such as data center REITs, including the one we’ll cover in a moment). However, Iron Mountain’s legacy business isn’t going to disappear overnight (it’s mission critical for many of the tenants that use its properties), and Iron Mountain is making strong efforts to expand into newer growth business (including data centers to serve many of its existing legacy clients).

And considering the recent market wide plunge, the price and dividend yield of Iron Mountain have become significantly more compelling in our view. You can read our full detailed write up on Iron Mountain here.

*Honorable Mention: Digital Realty (DLR), Yield: 3.1%

We currently own shares of Digital Realty, but it only makes it onto our list as an honorable mention because its yield is too low to be considered a “big dividend” as compared to the other names on our list. And interestingly, DLR’s share price has actually Risen during the recent coronavirus panic as many investors view it as less susceptible to coronavirus risks.

If you don’t know, DLR is a data center REIT. A data center is a physical facility that organizations use to house their servers, critical applications and data. These facilities provide a highly reliable and secure environment, and are equipped with uninterruptable power supplies, air-cooled chillers and physical security. You can read our most recent full write up on DLR here.

7. The Geo Group (GEO), Yield: 15.1%

Without getting too philosophical or too political, sometimes things sell off for the wrong reasons. And in this case, we believe that The Geo Group (GEO) has been unfairly incarcerated by Mr. Market.

The GEO Group is a specialty REIT that owns, operates and manages correctional, detention and reentry facilities. And in some sense, the business is a prisoner to swings between the political left and right. However, in Geo’s case, it seems to have swung more than just a bit too far thereby making for a very attractive investment opportunity if you understand what you are getting into. You can read our full detailed report on The Geo Group here.

6. EPR Properties (EPR), Yield: 13.9%

In some regards, the coronavirus outbreak has removed the curtain on just how fragile some businesses are. For example, experiential property REIT EPR has been hit extremely hard. In particular, just last week the company withdrew its previous guidance and:

“announced the deferral of its anticipated gaming venue investment and all other uncommitted investment spending due to unfavorable current market conditions.”

If you don’t know, EPR is a triple-net lease specialty REIT focusing on property types such as theaters, eat and play, ski, attractions, experiential lodging, gaming, fitness and wellness, cultural and live venues. Yuck! Considering the coronavirus outbreak, who wants to go there!

However, if Wuhan China is any guideline (see tracker tool here), the coronavirus is being brought under control there, and with any luck it’ll be brought under control throughout the rest of the world sooner than later (President Trump suggested August). EPR’s business was attractive before the truly massive sell off, and we believe it’ll become attractive again. Only time will tell just how truly draconian the impacts will be, but it you are an optimist, the market will recover, and eventually EPR will too. You can read our previous full write-up on EPR here.

*Honorable Mention: CyrusOne (CONE), Yield: 4.1%

This is another data center REIT that we own, and it has done relatively well this year (it’s down less than the overall market). We’re including it as an honorable mention because its dividend yield is not high enough to be included on our “big dividend” REIT rankings. However, the shares are worth considering for investment.

We like CONE because it offers a steady growing dividend (the dividend has been increased in each of the last seven years), and the potential for strong capital gains. Further still, we view CyrusOne as a potential buyout target because if it gets acquired it would likely be at a significant premium to its current share price, which means investors would get a significant and immediate gain on their investment. You can read our most recent full report on CyrusOne here.

5. Core Civic (CXW), Yield: 16.7%

Core Civic owns and operates private prisons and immigration detention facilities. And political rhetoric, combined with the recent market wide sell off, has created a very attractive buying opportunity.

Specifically, the shares have sold off hard despite solid cash flows and a high demand business with long-term visibility. It’s basically a mission critical business with a lack of alternatives, and the dividend is very well covered. You can access our full report on Core Civic here.

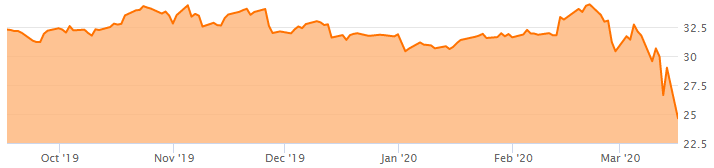

4. Monmouth (MNR), Yield: 6.5%

Monmouth is an attractive industrial REIT. Not only does it have long-term leases with investment-grade tenants at attractive rentals, but it’s also offering an attractive dividend yield—significantly higher than many of its industrial REIT peers.

This is essentially a very strong dividend at a very compelling price. You can access our full report on Monmouth here.

3c. Ventas (VTR), Yield: 13.3%

Ventas is a healthcare REIT with a main focus on senior housing. The shares had already been trading at an attractively discounted price, in our view, as a supply/demand mismatch has caused occupancy and NOI to fall. And now the sell off has been magnified by the coronavirus.

In particular, the sell off was magnified at Ventas in particular because of news of a coronavirus outbreak at another senior living facility owned by healthcare REIT peer Sabra Health Care (SBRA). We shall see how recent market events impact long-term demand, but considering the absolutely enormous price decline, a huge amount of fear is already baked into the price. You can access our last full report on Ventas here.

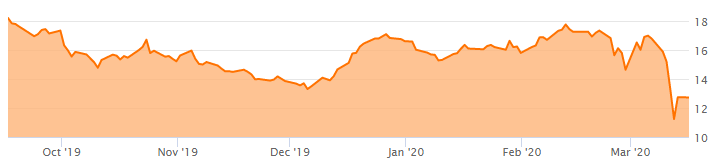

3b. Welltower (WELL), Yield: 9.0%

Welltower is a healthcare REIT (mainly senior housing and outpatient medical), and the business has been strengthening. Specifically, FFO growth challenges have been brought under control, and the metric is now expected to increase in the years ahead. Also, the payout ratio of ~82% is attractive, and leaves plenty of cushion for the dividend. Further, the company will benefit from powerful demographic trends, and the Fed’s most recent interest rate cut. The dramatic market sell off has likely created a very attractive entry point.

If you are a long-term income-focused investor, Welltower is worth considering for a spot in your prudently diversified portfolio. We own it. You can access our recent full write-up on Welltower here.

3a. HealthPeak (PEAK), Yield: 6.7%

Over the last couple years, Healthcare REIT Healthpeak wisely and proactively took steps to reduce its exposure to troubled senior housing through its new joint venture and focus on private pay. However, HealthPeak (formerly HCP) has slid under the radar for many investors.

Considering its improved business model, low share price, and high dividend yield, we believe it is worth considering. We own shares. You can access our previous write-up on HealthPeak here.

2. WP Carey (WPC), Yield: 5.6%

If you are looking for healthy durable income, consider WP Carey (we currently own shares). It is a commercial REIT that owns owns single-tenant industrial, warehouse, office, retail and self-storage properties subject to long-term net leases with built-in rent escalators.

WPC’s management has been a sound steward of capital, simplifying the business model, lowering the cost of capital and growing the dividend. You can access our full report on WPC here.

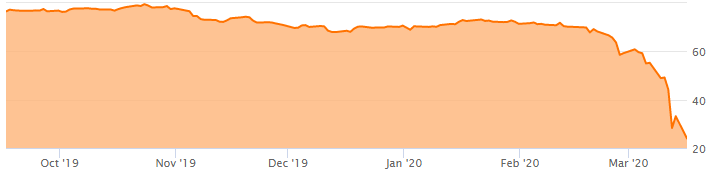

1. Simon Property Group (SPG), Yield: 12.8%

If you are looking for a big healthy dividend, trading at an inappropriately low price, consider investing in Simon Property Group (we own shares).

Simon is basically an A-Class mall REIT that has faced indiscriminate selling pressure as investors fear the ongoing disruption of traditional retail by online shopping. Simon management also believes brick-and-mortar REITs are trading too low as evidenced by SPG’s recent acquisition of Taubman for ~3.6B in cash. We believe Simon’s shares were trading too low before this whole coronavirus mess, but the shares have plummeted in recent weeks, driving the dividend yield to an incredible level. We believe this coronavirus mess will eventually pass, and SPG’s share price will eventually go much higher, and investors can keep collecting its big safe dividend yield while they wait patiently for the long-term gains to come. You can access our most recent full report on SPG here.

Conclusion

The recent market sell off has been extreme. And no one knows with certainty when it will end. But what we do know is that despite the very real impacts of the coronavirus, long-term investing has repeatedly paid off throughout history. Dividend yields are extraordinarily attractive right now (as share prices are prices in the worst), and it’s highly likely that in the months and years ahead, investors will look back at the current market conditions now, and wish they took advantage. For reference, you can view all of our current holding here: Portfolio Tracker.