This report reviews an attractive industrial REIT that will continue to benefit from e-commerce trends. It has maintained or increased its dividend for 29 years in a row and it currently yields ~4.0%. It has the highest occupancy and rent collections in the industrial REIT space (tenants include some of the largest well-know investment grade companies) and the valuation is attractive. It also has multiple growth catalysts. This article reviews the health of the business, valuation, risks, dividend safety, and concludes with our opinion on why it may be worth considering if you are a long-term income-focused investor (that likes growth too).

Monmouth (MNR) share price

Overview: Monmouth (MNR)

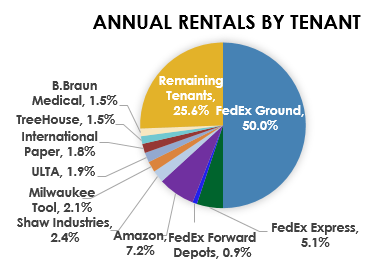

Monmouth Real Estate Investment Corporation (MNR) is an industrial REIT which focuses on single-tenant, net leased industrial properties in the US. Its portfolio consists of 119 properties in 31 states with a total of ~23.4 million square feet (MSF) of gross leasable area (GLA). The vast majority of the company’s industrial buildings are leased on a long-term basis primarily to investment grade tenants who accounted for 81% of FY20 rental revenues. Notably, a large portion of the portfolio is exposed to the ecommerce ecosystem, with marquee clients such as FedEx and Amazon accounting for ~63% of annual rentals. This bodes well for MNR as the continuous shift of consumer spending from traditional stores to internet sales, accelerated by the COVID-19 pandemic, results in rising demand for industrial properties. MNR’s property portfolio also includes one shopping center located in New Jersey, and it also owns a securities portfolio of REIT stocks, which represents ~4.9% of its undepreciated assets.

Source: Company Presentation

Source: Company Presentation

A Young and High-Class Property Portfolio

MNR’s portfolio is the youngest in the industrial REIT sector with a weighted average building age of 9.8 years, and consists of traditional warehouses as well as large state-of-the-art automated buildings that can handle both wholesale distribution, as well as direct-to-consumer distribution. Most of these properties are located in the eastern half of the US, which has the highest population density (over 70% of the US population lives east of the Mississippi river). Logistically, these regions are well connected to the US railroads and with the expansion of the Panama Canal, the container traffic has also been rapidly shifting to the East Coast ports. These factors make MNR’s portfolio highly attractive to large tenants who rely heavily on omni-channel sales and distribution strategies.

Consequently, MNR has been able to lease its industrial buildings to some of the largest and best-known companies in the US, and this has resulted in it being able to consistently maintain the highest occupancy rate in the sector, despite the uncertain macro environment, and also collect almost all of its accrued rentals throughout the pandemic.

Source: Company Presentation

Multiple Growth Catalysts

Rising Online Sales: The COVID-19 pandemic has created a parabolic shift in the amount of goods moving online as it has accelerated the shift to online shopping by nearly two years. E-commerce sales in the US are expected to rise to $795 billion in 2020, representing a 32.4% increase from 2019 and 14.4% of total retail sales in the US. By 2024 online sales are expected to account for ~19% of all retail sales, indicating a CAGR of ~11% from 2020 through 2024, and compares favorably to an estimated 1.8% annual growth rate of brick-and mortar sales, and an estimated 3.3% annual growth of total retail sales in the US through 2024.

Source: eMarketer, Oct 2020 and US Census Bureau

It is estimated that ecommerce sales require about three times the warehouse space relative to brick-and-mortar retail sales. As the majority of retail industry players continue to migrate from brick-and-mortar stores to omni-channel platforms to take advantage of the vast e-commerce opportunity, there is an enhanced demand for large, modern industrial distribution centers.

Acquisition Pipeline and Expansion Projects: MNR has a differentiated business model wherein it takes out fully amortizing property-level mortgages to secure the payment of indebtedness. This makes it safer from an individual bad property fallout and also helps it with ample liquidity to pursue growth through accretive acquisitions as well as expansion projects. According to Eugene W. Landy, Founder & Chairman, on FY2020 earnings call

“If they (properties) have leases on them with credit tenants, we can borrow against them. Now you have to picture the amount of liquidity we're going to have. I hear some questions that when we have this pipeline of $300 million, $400 million, people are worried where we're going to get the money. Well, we worried about that in advance and we have the money. We're very liquid.”

Also, the company has built strong relationships with the merchant builder community over five decades of its operating history, which has resulted in growth of its high-quality pipeline. During the same call, Landy also explained:

“We're not going to grow for growth's sake, but I think I'm confident we'll be able to continue to land the type of deals that we've built this portfolio. One high-quality acquisition at a time. And the people we've done transactions with have been partners for decades, and so they come to us with deals……the prospects, future prospects have never been better.”

As of 30 September, 2020, the value of MNR’s new pipeline stood at $338.4 million with six modern built-to-suit industrial buildings comprising 2.4 MSF. Notably, all of these properties are leased to investment grade tenants - four to FedEx, one to Home Depot and one to Mercedes-Benz. Altogether, the new pipeline is expected to represent a 10% increase in the company’s GLA and will have a weighted average lease term (WALT) of 15.3 years, thereby substantially adding new rental stream in the future.

On the expansion front, the company has six FedEx Ground parking expansion projects in progress, with ten additional locations under discussion. These expansion projects will result in extension of the lease terms as well as additional rental income. And, with a land to building ratio of 5.3:1, MNR has ample expansion capabilities, which further builds on its rental revenue growth opportunities.

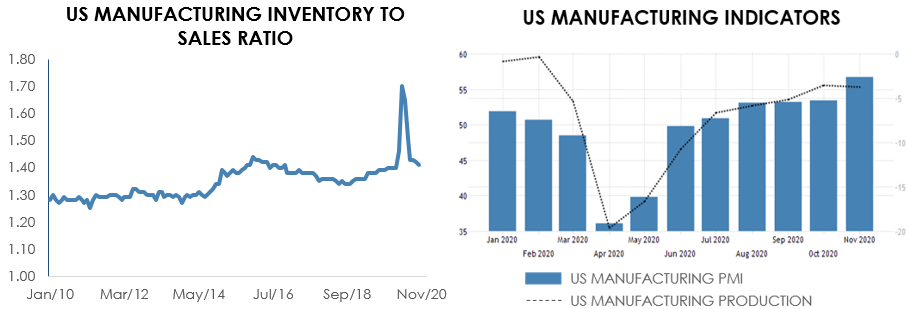

Supply Chain Reconfiguration and Accelerating US Manufacturing: The pandemic has created a need for supply chains across many industries to be more resilient in the post-COVID world. There is an increased inventory stocking already taking place, and as supply chains seek to better prepare for future surges in demand, they will increase their inventory levels substantially, leading to greater demand for industrial space.

Also, with supply chains favoring shorter travel distances and reduced reliance on foreign production sources, the manufacturing activity in the US has accelerated and is expected to continue to increase. This will drive the demand for industrial assets in the US in the near future.

Source: US Census Bureau and tradingeconomics.com

Overall, with an existing property portfolio positioned around the e-commerce industry, a unique business model that provides ample liquidity to pursue accretive acquisition opportunities and the significant aforementioned macro tailwinds, we believe MNR has multiple opportunities for growth, going forward.

Sustainable Dividend

MNR has one of the best track records in the industrial REIT sector in terms of dividend payments. It was the only REITs that maintained its dividend throughout the recession of 2008-2009, and has now maintained or increased its dividend for 29 consecutive years. At the current annual dividend of $0.68 per share, MNR delivers a dividend yield of 4.0%, which looks fairly attractive considering the NAREIT industrial REIT dividend yield of 2.55%. The current payout ratio on funds from operation (FFO) is 85.0%, and on adjusted funds from operation (AFFO) is 89.5%, which makes the dividend quite safe in our view. For the full year 2020, MNR expects its dividend payout on FFO to be 83.5%, which is relatively higher than its peers.

Source: Company Presentation and Yahoo Finance

Additionally, MNR manages its balance sheet quite conservatively and uses all the three capital forms - equity, debt, as well as preferreds under an ATM program primarily used to fund its acquisition pipeline. As of 30 September, 2020, the company’s net debt to market capitalization was 31%, while preferreds represented 18% of the total capitalization. Although the high debt load, coupled with a leverage of 6.0x (net debt/adjusted EBITDA) and a 2.3x fixed charge coverage might cause some concern, we note that ~91.5% of the debt comprises of mortgages that are backed by assets rented to investment grade tenants. The mortgage debt has a weighted average maturity of 11.1 years, representing one of the longest debt maturity schedules in the REIT sector.

Source: Company Presentation

On the liquidity front, MNR has ~$457.3 million in potential liquidity, comprising of $23.5 million in cash, $225 million available on revolving line of credit with an additional $100.0 million potentially available on an accordion feature, and $108.8 million from its REIT securities portfolio.

We think MNRs conservative capitalization strategy improves its ability to raise capital, while allowing it to tap capital at the lowest cost, and the available liquidity provides a safety net around which it can sustain and continue to grow its dividends.

Valuation:

MNR has tripled its size over the last 7 years and is one of the best performing industrial REIT this year, having returned 20.3% year to date and is up about 90% from the March lows at its current trading price of $17.10. Despite the rise in price, the company’s management has not tapped the equity markets to fund its acquisition pipeline as it thinks the current prices do not accurately reflect their value. In the words of the company’s CEO, Michael P. Landy during the FY2020 earnings call:

“As far as issuing common equity, not at these prices, NAV is well north of where we're currently trading. And so, while we've had a common ATM up and running since -- for 2 years now, we haven't issued a single share and nor do we intend to at these levels.”

Source: Yahoo Finance

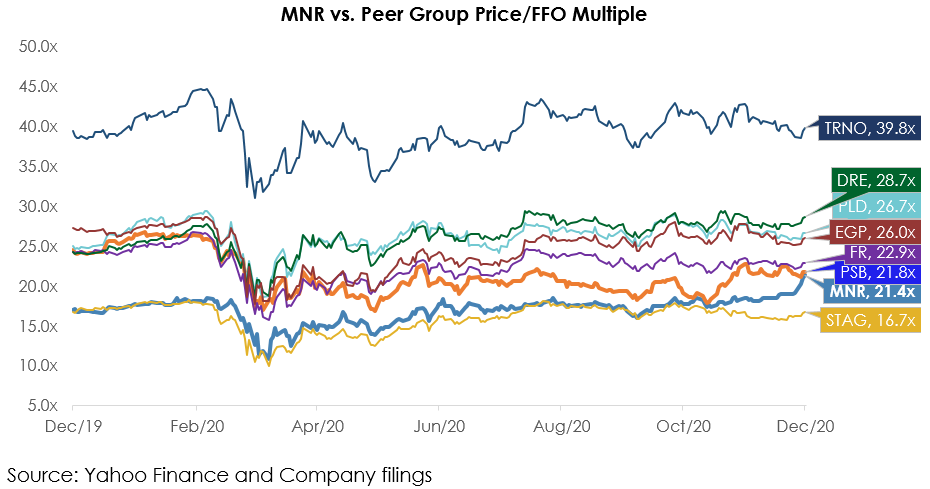

Further on a Price/FFO multiple basis, the shares trade at 21.4x. This compares favorably to most of its industrial REIT peers, some of which trade in the high 20s and high 30s multiple range. This creates a comparative valuation gap, which we believe is unwarranted considering the multiple growth catalysts it has.

Risks:

Blackwells Acquisition Offer: In December, Blackwells Capital offered to acquire Monmouth for $18 per share. While this represented a premium to the share price at that time (and currently), the offer does not adequately represent Monmouth's long-term value considering the high demand and growth prospects for Monmouth's relatively young asset portfolio. We'd prefer Monmouth not be acquired, and at the very least that the offer price be increased significantly. According to reports, Monmouth Chairman Eugene Landy said that exploring the offer would "not be in the best interests of the company." However, the possibility of acquisition presents a risk to current shareholders.

Concentration of the Portfolio: Although MNR is well diversified across geographies within the US, its portfolio is largely concentrated with FDX which accounts for ~46% of its GLA and ~56% of its annual rentals. Such a large concentration on a single tenant has inherent risks which can cause significant business disruptions, should an unfavorable situation arise.

Interest rate risk: Federal Reserve has cut interest rates to near zero levels and even though we expect interest rates to remain relatively tame, dramatically rising rates could create challenges. As REITs are often seen as an alternative to bonds, higher interest rates could mean decreased demand for REITs, thereby causing a decline in their share price.

Tenant Bankruptcies: As with other REITs, MNR is also exposed to the risk of tenants not being able to meet their rental obligations owing to the difficult operating environment. However, MNR’s focus on large investment grade clients is a key mitigant of this risk.

Oversupply of Industrial Properties: There is an enhanced demand for industrial properties in the US due to the secular shift to online sales and favorable macro factors. The US industrial vacancy rate is at a record low of 4.7%, and ~341 million square feet of industrial properties are under construction in the US. This has created a highly competitive environment with almost all the capital earmarked for commercial real estate getting targeted toward industrial properties. This can possibly lead to an oversupply of industrial properties and could have a negative effect on MNR.

Conclusion:

MNR has a modern portfolio of large industrial properties that is positioned around the e-commerce industry. This makes it one of the best positioned industrial REITs that can benefit from the long-term secular trends of online sales growth. Although the current dividend yield at 4% looks a little low compared to the overall REIT universe, it is still the best in the industrial REIT space. Further, a attractive payout of only 85% of FFOs suggests that the dividend is safe and is likely to grow as the company grows its cash flows in the future. While MNR’s stock has outperformed its industrial peers this year, the trading multiples suggest it is still valued at a relative discount to its peers. With multiple growth catalysts clearly visible, we believe Monmouth presents an attractive investment opportunity. If you are looking for steady income and continuing growth, shares of Monmouth are worth considering for a spot in your portfolio.