Don't be this guy! As many investors got burned last month with overly concentrated "hyper-growth" portfolios, our performance continues to be strong, and we like our holdings going forward. Some of our under-priced securities started to post the big gains we believe they're overdue for, and a couple positions sold off, thereby making them even more attractive now; we will review those (and our overall performance) in this report.

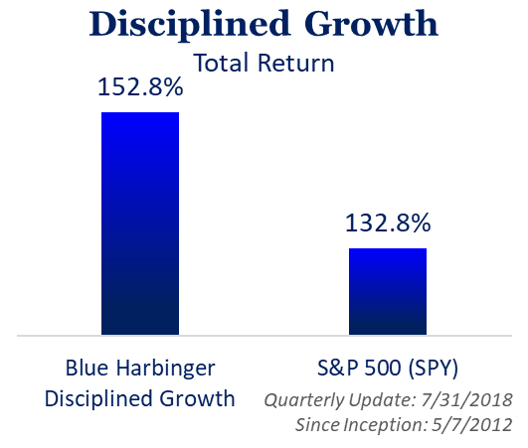

Here is a high-level look at growing performance track-records of our three strategies...

And here are the July month-end total returns for each strategy, and for each position within each strategy...

Income Equity Portfolio Holdings:

Disciplined Growth Portfolio:

Balanced Portfolio:

Big Movers & Attractive Opportunities...

And here are updates on the biggest "movers" over the last month, as well as some ideas on our top investment ideas (to be clear, we like all of our current holdings, especially within their respective diversified investment portfolios, but a few are looking particularly attractive right now)...

Williams Partners (WPZ)

There's been a lot going on with this big dividend name recently (and the energy and the MLP space, in general), but the two big highlights are: (1) In May, Williams Companies (WMB) agreed to buy all the outstanding shares of its master limited partnership William Partners (WPZ) for $10.5B; and (2) WPZ beat revenue expectations (a good thing) slightly after the end of July. Overall, we view the combination of WMB and WPZ very positively as it will create less conflicts of interest and less MLP regulatory concerns. Williams owns a vast network of attractive assets, and even though the dividend (distribution) will be reduced moderately post combination, the company is steady, strong, and has plenty of cash flow and growth ahead.

Phillips 66 (PSX):

Phillips 66 is an energy refiner that has long deserved a higher valuation multiple based on its expansion into more midsteam business (which provides steadier long-term revenues). PSX also beat earnings expectations at the end of July as refining gains powers earnings (and the shares) significantly higher. This is a powerful business, with significant competitive assets (it's geographic asset footprint cannot realistically be recreated by anyone) that has significant continuing long-term price appreciation and big dividends in the years ahead.

Triton International Limited (TRTN):

TRTN experienced a very large share price gain this past week after a very bullish article in Barron's over the weekend. Here is the article. Earlier this year we wrote about the attractiveness of selling income-generating put options on Triton at a $30 strike price. And here is another one of our recent Triton articles. We agree with the Barron's article, and believe these shares can easily go 15-20% higher from here (in the relatively near future), and that is on top of the big dividend yield offered by Triton (check out our articles (links above) for more details.

Tsakos Energy Navigation Ltd (TNP):

This big-dividend payer was down 5.9% during July, however we believe it remains attractive (for reasons described in our link below). Tsakos offers an array of high-yield equities including 5 series of preferred shares with dividend yields ranging from 7.9% to 9.5%, and common shares offering a dividend yield of 5.8%. We recently wrote in detail about the attractiveness of Tsakos in this article:

Walt Disney Co (DIS):

These shares steadily rose in July leading up to the approval by shareholders of the $71 billion deal between Disney and Fox. The transaction is still months from closing, but is anticipated to create powerful new growth opportunities for Disney in the rapidly evolving media world. The shares currently trade at around $113, but for perspective Bank of America sees significant upside with a price target of $144 based on "healthy studio and theme park trends" expected in Q3. And aside from studio gains from Incredibles 2 and Marvel films, the company should see affiliate fee growth in cable and rising fees in broadcasting. (see: BofA sees 29% upside as Disney streaming approach evolve.

Facebook Inc (FB):

Facebook is a high-margin money printing machine, and July's significant sell-off creates a very attractive buying opportunity, in our view. The shares have been unusually volatile as it faced heat from US and European governments over privacy concerns. Facebook announced lower than expected quarterly earnings recently, which contributed to the further sell-off, but remember this sell-off was due mainly to Facebook taking its foot off the advertising gas (as a result of near-term regulatory concerns), NOT because there are fundamental problems with the underlying business. Facebook does not pay a dividend, but if you are looking for a little long-term growth, Facebook is a buy. As the saying goes: "buy when there is blood in the streets." Facebook has been beaten up badly in the news--it's a buy!

First American Financial Corp (FAF)

If you need title insurance on a new home purchase (or refinance), FAF will likely be involved because the company is the clear leader in the space. The company also announced very positive earnings results at the end of July which powered the shares nearly 9% higher for the month of July. The dividend yield on these shares was originally much higher when we first purchased over 2 years ago, but the price has risen strongly (which we're happy about) that the % yield has mathematically lowered. This remains a healthy growing business with more upside ahead.

Omega Healthcare (OHI)

This big-dividend healthcare REIT has been volatile, and it announces earnings after the close Friday (8/3). We own shares in our Income Equity portfolio because we believe it's long-term prospects remain attractive. You can read our recent Omega write-up here:

Nuveen Real Estate Income Fund (JRS), Yield 8.3%

We don't currently own shares of this big-dividend closed-end fund, but it is high on our watch list considering its attractive allocations and the fact that it currently trades at an attractively large discount to its net asset value. We recently wrote about this one in detail in this members-only article:

Digital Realty (DLR)

Data center REIT, Digital Realty announced positive earnings during the month that drove the share price significantly higher, as expected. As we wrote about earlier this year, DLR was dramatically underpriced (see article link below), and it was overdue for a big price gain. Further, we believe this one has a lot more room to run (i.e. more upside and big dividend payments ahead).

Johnson & Johnson (JNJ)

As we wrote about JNJ just over two months ago...

...And since that time, the shares have rallied hard, gaining 8.5% in July. As described in the above article, this blue chip dividend grower has lots of room for steady growth, the dividend growth is outstanding, and there is more long-term upside from here.

Conclusion:

in our view, one of the keys to long-term investment success is not to be greedy like the cash-consuming business man graphic at the start of this article. A lot of investors get burned by overly concentrating their investment portfolios, and by chasing only the hot stocks garnering the most sensational media attention. Diversified, long-term investing is a proven strategy for long-term success.