There is a lot of gloom and doom surrounding big-dividend skilled nursing facilities (“SNF”) REIT Omega Healthcare Investors (OHI). The negativity originates mainly from Omega’s many troubled operators (as we wrote about in detail back in March: Despite 5 Huge Risks, Omega Is Worth Considering). And investor fear has grown as short-interest remains high, the share price has been volatile, and the very recently announced termination of restructuring support for SNF operator, Orianna. With Omega expected to announce earnings this week, this article reviews the big risks (e.g. dividend safety, slow growth, valuation, and the potential for more distress among operators) before concluding with our views on who might want to own this high-income REIT, as well as an idea on how you might want to “play it,” if at all.

Overview:

Omega is the largest SNF-focused REIT. As of March 31, 2018, Omega’s portfolio consisted of 963 operating facilities, located throughout the US and the UK. Based demographics (i.e. the aging population), Omega believes the SNF industry is at the beginning of a 20+ year secular tailwind (i.e. Omega believes there is lots of growth in the years ahead). However, as shown in the following chart, Omega has lagged the broader market (both the S&P 500 and the REIT industry) over the last two years.

Why Omega Has Lagged the Market:

Omega’s share price has lagged the broader market in recent years for two main reasons. First, Omega is a REIT, and REITs in general have lagged the rest of the market (as per the Real Estate ETF in the above chart) largely due to interest rate fears. Specifically, REITs rely heavily on borrowing to fund growth, and as interest rates rise it become more expensive for REITs to operate and grow.

Secondly, Omega has sold off because of the challenges in the SNF industry. Specifically, there is immense regulatory pressure to keep medical reimbursement rates low, and this creates significant challenges for the tenant companies operating Omega’s skilled nursing facilities. We wrote about this in detail in this article, and the challenges keep getting more complicated as Omega announced just last week that it had terminated its restructuring support agreement with large operator, Orianna. Omega is making sure SNF patients remain taken care of, and this termination isn’t expected to impact the company’s expected range of rent or rent equivalents of $32 to $38 million this year, but it will still be costly to transition facilities to a new operator, and this potentially makes dividend coverage even more challenging for Omega down the road (more about dividend coverage later).

Perhaps making matters worse, it doesn’t help investor confidence that short interest remains high, as shown in the following chart.

Dividend Coverage:

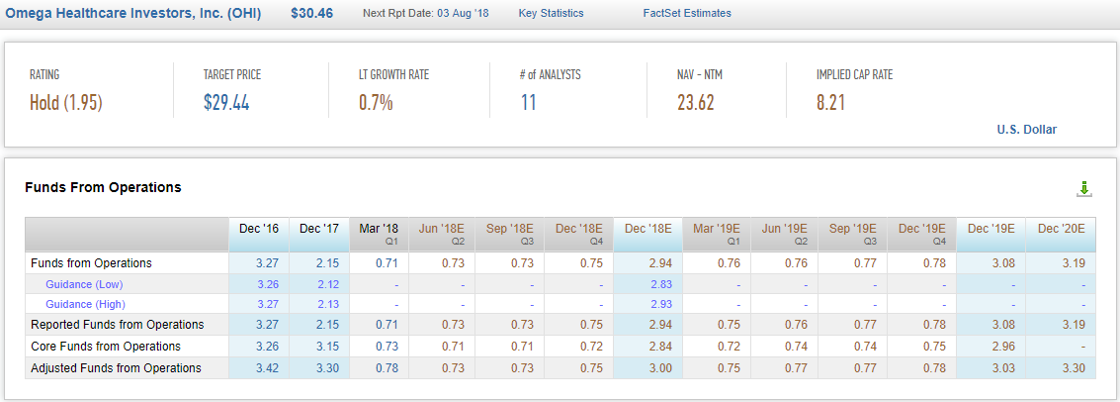

From a dividend coverage standpoint, Omega continues to have less and less “cushion” as market conditions remain challenging. The following chart shows Omega’s growing payout ratios (i.e. less cushion) in terms of funds from operations (FFO) and funds available for distribution (FAD); and with an earnings announcement coming up this week, the market is nervous.

Omega has already halted dividend increases for this year, thereby putting an end to an impressive multi-year stretch of raises.

Slow Growth:

Despite constant reminders from Omega's management about the coming demographic wave that will drive growth higher, Wall Street analysts still have low expectations. In fact, the average analyst has only a “hold” recommendation, and they’re expecting FFO per share to shrink through the year 2020, as shown in the following graphic.

For perspective, here is a look at current and historical Omega price targets from Wall Street Analysts.

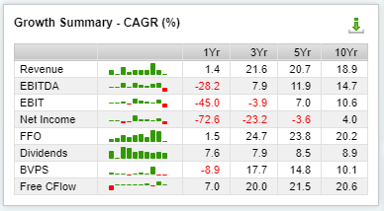

For more perspective, here is a look various growth metrics for Omega, which have clearly been slowing in recent years.

Valuation:

Comparing FFO to share price is one of the common ways to value REITs such as Omega. This next chart shows Omega’s price-to-FFO ratio versus other healthcare REITs, but keep in mind Omega is the only one focused mainly on skilled nursing facilities.

Omega’s low price-to-FFO ratio is a sign of value, but it’s also indicative of the higher risk perceived by the market.

Cap rates are another way to value many REITs (cap rate is essentially net operating income divided by market value, and it shows the potential rate of return on investments). As shown in our early graphic, Omega’s current implied cap rate is 8.21%, which is both attractive (because it’s relatively high) and risky (it’s high because the market perceives risk).

Here is a look at the range of various valuation metrics for Omega over the last 5 years, and current values sit in the lower end of the range in multiple important categories.

Who should Consider Owning Omega:

In case you haven’t figured it out yet, Omega is not a high-flying “FANG” stock. Omega is a big-dividend value stock, that may be compelling for contrarian investors. More specifically, if you are an income-focused value investor, then you may want to consider owning Omega as one allocation within your larger, income-focused investment portfolio. For example, management remains very optimistic as they work through challenging market conditions, and as the demographic wave grows larger on the horizon.

Consider Income-Generating Put Options:

Another way for income-focused investors to “play” Omega is to sell out-of-the-money income-generating put options, especially before this week's earnings announcement because uncertainty is particularly high (uncertainty drives up the premium income available on options). For example, here is a look at the premium income you can generate by selling puts.

We generally like to sell income-generating put options with about 1-month to expiration and with a strike price at least 4-5% out of the money. This trade generates up front income for us, and it gives us a chance to own shares of Omega at an even lower price (if they get put to us before expiration); if they don’t get put to us, then we’re happy to simply keep the premium income we generated for selling the puts.

Very important to note, Omega starts trading ex-dividend on Monday (7/30), and it is expected to announce earnings on Friday (8/3). Both of these may increase the volatility and the premium available for selling the puts, as the market digests all of the activity.

Conclusion:

If you are a long-term, income-focused, contrarian investor, Omega is worth considering, bearing in mind the significant risks, as described in this article. We are currently long Omega within our Blue Harbinger Income Equity portfolio, and we may sell income-generating put options this week (before earnings) because we wouldn’t mind owning more if the price falls far enough. This is NOT a low-risk investment, but it does offer high-income and the potential for significant long-term gains.

You can view all of our current holdings here.