We like to share a variety of investment ideas with our readers, and today we share a differentiated high-yield opportunity that we have discussed in the past. It may not be interesting to everyone, but we believe the yield is attractive and the rewards outweigh the risks.

Frontier Communications 1/15/2023 Bonds

Frontier's (FTR) high-yield bonds are attractive. They offer a +9% yield, and they trade at a 22.5% discount to par value, thereby offering a +13% annualized yield to maturity in 2023. In our view, the company's stock will continue to be challenged, but the bonds offer more reward than risk, and they're worth considering if you are an income-focused investor.

For your reference, our latest write-up on Frontier is included below. As you read through it you'll probably sense we are negative on the stock. However, we like the 2023 bonds. We believe these bonds are "money good" and they're currently trading at an attractive price.

Frontier Communications (FTR)

Highlights:

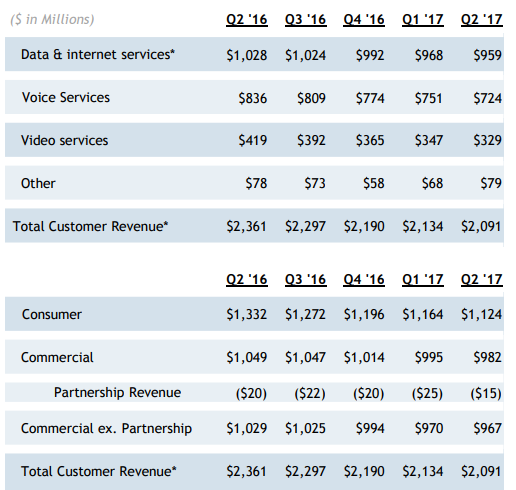

- Frontier’s revenues are slowly declining across all three of its main business segments (including: data & internet services, voice services, and video services), and its cash flows are stretched very thin between capital expenditures (to support its network), a large amount of debt, and customer service/retention efforts.

- Frontier’s network is subpar compared to larger telecoms such as Verizon and AT&T. However, Frontier’s operations include smaller rural areas where they are often the only provider. Frontier receives government subsidies and regulated revenue that account for roughly 9% of total revenue.

- Frontier’s shares have declined 72% year-to-date, the dividend has been cut, and the company completed a 1-for-15 reverse stock split this year. The company may need to cut the dividend again, issue more debt and/or equity, and sacrifice network quality and customer service just to meet its upcoming debt maturities.

- Despite the challenging and highly uncertain conditions for the stock price, we believe the company has plenty of sustainable business and cash flow to support its debts through at least 2023.

A Summary of the business and the industry

Frontier provides phone, Internet, and data services to urban, suburban, and rural communities in 29 states. The company has been struggling with customer attrition, challenging integration issues (it acquired assets from Verizon in California, Texas, and Florida in 2017, and assets from AT&T in Connecticut in 2014), and a significant amount of debt. Revenues have been declining across all segments.

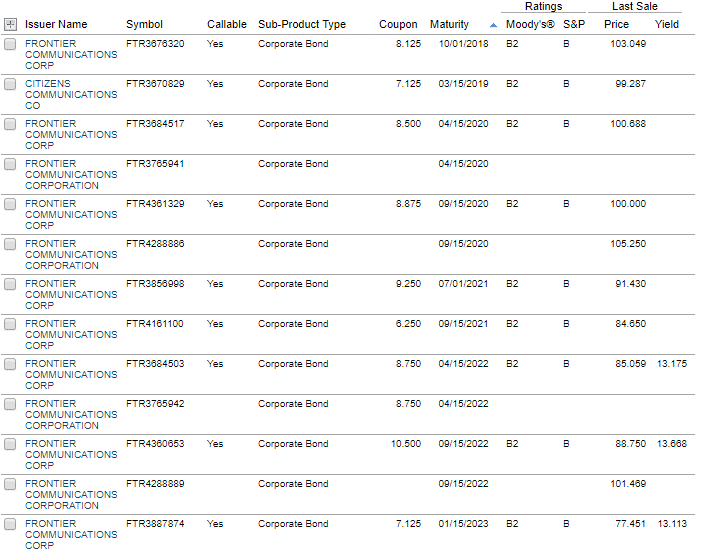

Frontier has been working to improve its debt profile. For example, during the second quarter Frontier completed a term loan facility and upsized the cash tender offer for its 2020 notes, which lowered interest expense and extended maturities. Specifically, during the quarter Frontier issued $1.5 billion in secured debt, and retired $763 million of 8.875% Notes due in 2020 and $527 million of 8.500% Notes due in 2020. Frontier’s debt maturity profile is as follows.

Based on current yields on Frontier bonds, the market has a high degree of confidence that Frontier can support its debt through 2020, but beyond that date the yields get significantly higher implying a higher degree of uncertainty in the company’s ability to remain a going concern.

From a liquidity standpoint, Frontier has $387 million of cash and short-term investments on its balance sheet (as of 6/30), and management expects between $800 million and $900 million of free cash flow for 2017 (an achievable figure based on history and recent cost cutting, including the dividend cut). Assuming Frontier can stop the customer attrition, the company may be able to remain a going concern well beyond 2020. However, it will be increasingly challenged to refinance its existing debt considering its weakening financial positon and the expectation for rising market-wide interest rates.

Brief History of the Company and its founding

Frontier was known as Citizens Utilities Company until May 2000 and Citizens Communications Company until July 31, 2008. The company previously served primarily rural areas and smaller communities, but now also serves several large metropolitan markets. Originally based in Minneapolis, Citizens Utilities Company was formed from remnants of Public Utilities Consolidated Corporation in 1935.

Valuation:

We value Frontier using a discounted cash flow model with both bull and bear case scenarios. In our bull case we assume the midpoint of the company’s 2017 adjusted free cash flow guidance ($800 million to $900 million) can grow at 2% into perpetuity, and we assume a weighted average cost of capital of 5.34%.

Our bull case assumptions amount to an enterprise value of $25.4 billion, and after adjusting for $17.6 billion of long-term debt and $1.1 billion of preferred stock, the equity value is $6.7 billion. This represents significant upside versus Frontier’s current market capitalization of $1.1 billion, however it is consistent with Frontier’s market capitalization in 2015 and 2016.

Our bear case uses the same assumptions as the bull case except the growth rate is assumed to be 0%. In this scenario, Frontier’s enterprise value is only $15.9 billion, and after accounting for the company’s $17.6 billion of long-term debt, the equity is completely wiped out.

Competition:

Frontier’s operations include small rural areas where they are often the only provider. However, the company has recently expanded into some larger metropolitan areas (by acquiring assets from larger companies) where competition exists. Worth noting, the larger telecom companies have exited many of the smaller rural areas because they view them as less attractive.

Also, Frontier faces competition from cable companies with regards to internet and cable TV options. Additionally, wireless data services have the potential to emerge as a viable alternative to serve many of Frontier's territories where populations are highly dispersed.

Management (Capital Allocation):

Management has issued new equity and taken on additional debt to finance acquisitions in the past. For example, Frontier’s recent acquisition of Verizon assets was financed with a combination of debt and equity. Thus far, management’s acquisitions have been poorly integrated and the stock price has declined significantly. Capital allocation over the next two years will be critically important as the company struggles to get its debt under control. Management has cut the dividend once already this year, and may need to cut it again in the upcoming quarters.

Catalyst:

There are a variety of catalysts that could boost the share price in the upcoming quarters. Primarily, if Frontier can stop the steady loss of customers (and revenues) that would be a positive that could drive the share price higher. Additionally, an increase in government funding could boost the company. Also, an acquisition or consolidation with another telecom company could boost the shares by strengthening the financials. An acquisition may seem compelling based on the low price, but the high debt and struggling business could be a deterrent. Further still, a bankruptcy could be a significant negative catalyst for the stock price. If the company cannot get its debts under control, bankruptcy could be an option.

Recent Price action:

Frontier’s shares have declined 72% year-to-date, the dividend has been cut, and the company completed a 1-for-15 reverse stock split this year. Short interest is currently over 30% of the shares outstanding.

Special /Unique:

Frontier is unique because of its focus on rural areas that other companies are not interested in. Also, Frontier receives significant government support (recently 9% of total revenues).

The Last Downturn:

As a telecommunications company, Frontier should be less sensitive to the economic cycle, however the stock was very volatile during the financial crisis of 2008-2009. Also, because of Frontier’s challenged financial condition, it may continue to be volatile regardless of overall market conditions.

Quality:

Frontier’s network is lower quality than larger providers such as Verizon and AT&T. Frontier has skimped on capital expenditures needed to maintain and improve its network. Also, its recent asset acquisition integrations from Verizon and AT&T have not gone smoothly, leaving many customers disgruntled.

Insider Activity:

A very small 1.2% of shares are owned by insiders. There are no significant insider buys or sells to report.

Capital Structure:

Frontier’s debt to equity ratio has increased dramatically in recent years.

Frontier has outstanding common stock (FTR), preferred shares (PIY and FTPR), and a variety of publicly traded debt (as described earlier).

Risks:

Perhaps the biggest risk for Frontier is simply that it will not be able to refinance its existing debt when it comes due. Considering the current low cash position, and the company’s deteriorating financial strength, it will not be able to pay off the debt, and it may not be able to refinance it thereby leading to a bankruptcy situation. The debt challenge is compounded by the potential for rising market-wide interest rates. The continued availability (and to what extent) of government funding is also a risk the company faces.

Conclusion:

Frontier's stock price faces a high degree of uncertainty. However, the company also continues to generate attractive free-cash-flow. We expect continued attractive free-cash-flow in the coming years, but the amount may be reduced over the long-term as customers convert to wireless or cable competitors. Despite the challenging and highly uncertain conditions for the stock price, we believe the company has plenty of sustainable business and cash flow to support its debts through 2023 (and potentially beyond). We believe the 1/15/2023 bonds are attractive.

For your reference, you can view our previous Frontier report here:

And you can view all our current holdings here: