As we wrote here, we sold our shares of Caterpillar on Friday for +110% gain after owning them for 19-months. We expect to purchase new shares with the proceeds within the next several trading days. This article highlights four very attractive investment opportunities that we are considering for purchase.

Overview:

- This article highlights four attractive investment opportunities, and we expect to purchase one (potentially two) of them within the next week.

- The impetus for the first trade is the cash available in our account after taking profits (+110% long-term gain in 18-months) on our Caterpillar shares that we sold on Friday.

- The impetus for the potential second trade would be profit-taking, to make room for an attractive new opportunity, and portfolio rebalancing based on our long-term view of shifting market conditions.

For your consideration, this article includes the high-level details on the four stocks we are considering (they are organized from least to most risky).

1. Kraft Heinz (KHC), Yield 3.2%

This blue chip company probably sounds completely boring to a lot of you, but it's long-term price appreciation potential (and healthy dividend growth) are very attractive for a variety of reasons.

For starters, Kraft Heinz is improving its already strong fundamentals, but the shares have pulled back thereby creating an even more attractive buying opportunity for long-term income-focused investors, in our view.

Our basic thesis on Kraft Heinz is fourfold:

- This is a very well-managed blue chip company with strong brand names that can thrive despite changing consumer shopping habits.

- The post-merger operational efficiencies continue to ramp up (and management is forecasting more benefits ahead), but the market is not yet giving enough credit.

- The entire consumer staples sector has been out of favor over the last several months relative to the overall market thereby creating a more attractive entry point.

- This company does an exceptional job maintaining prudent debt levels, strong (very safe) dividend payments, and highly attractive share repurchases that will allow the stock price to rise at a very attractive pace.

We'll have a lot more to say about Kraft Heinz in the coming days if we pull the trigger on this attractive trade.

2. Digital Realty Trust (DLR), Yield 3.1%

If you don’t know, Digital Realty is a blue chip data center REIT. It pays an attractive 3.1% dividend yield, it was added to the S&P 500 last year, and it sits square in the middle of a powerful long-term 21st century trend to move data into the "cloud" (which basically means data centers). For perspective, here is a look at a typical Digital Realty data center.

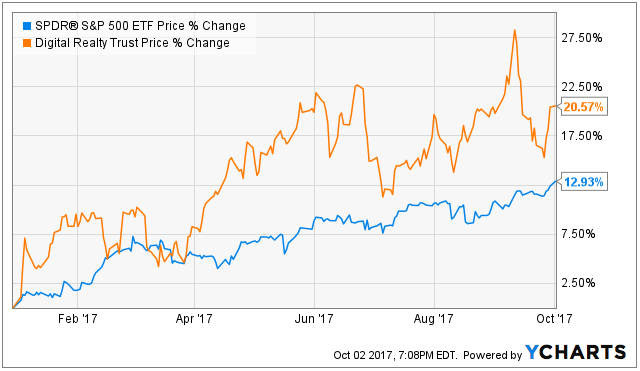

Further (and very importantly), Digital Realty generates a lot of cash, it pays a safe growing dividend, and the share price is on sale, in our view. The shares pulled back sharply in mid September after a regarded Venture Capitalist claimed the entire data center space was overvalued. However, coming from a venture capitalist that spends his days searching for investment “unicorns,” almost everything is unattractive to him, especially a powerful steady grower with a big growing dividend like Digital Realty.

For some important perspective, here is a look at the long-term secular trends that will continue to drive Digital Realty’s growth.

We also think it is important to understand Digital Realty’s diverse and growing customer base. As the following graphic shows, Digital Realty works with a diversified group of forward-thinking companies, however, we also believe there is an enormous wave of additional companies that will eventually benefit from moving to the cloud and Digital Realty is positioned to enjoy a lot of the benefits of the shift.

Digital Realty expects 2017 core FFO to be 5.95 to 6.10 per share, which on a price to core FFO ratio of around 19.7x. And considering the company’s continue growth opportunities, this is a very reasonable multiple. We've written about this company previously here.

3. Skyworks Solutions (SWKS), Yield 1.3%

We’ve written detailed reports about the attractiveness of Skyworks in the past...

...and the share price has recently pulled back thereby making for a very attractive purchase price in our view.

Our thesis on Skyworks is straightforward:

Skyworks is positioned to profit from the continuing growth in 4G LTE mobile services because its relatively large size, supply chain and technological sophistication allow it to meet growing marketplace demand.

Further, Skyworks is positioned to profit in the long-term (again due to its relatively large size, supply chain and technological sophistication) leading up to the release of 5G, which would enable powerful new (and high margin) applications (beyond mainly mobile phones) including smart cars, smart cities, and the Internet of Things (IoT).

Overview of Skyworks:

If you don’t know, Skyworks designs and manufactures semiconductors used in applications spanning smartphones, cellular infrastructure, broadband networks, the automobile industry, industrial markets, and others (although smartphones are the most significant). The company and the industry have experienced rapid growth in recent years as wireless data applications have expanded dramatically, particularly smart phones. Further, the industry will continue to grow rapidly as only 4.8 billion people worldwide subscribe to a mobile service (approximately two-thirds of the world’s population) with that number expected to reach 5.6 billion unique subscribers by 2020. Skyworks is expected to participate in the continued growth because its relatively large size and technological sophistication allow it to compete for large cutting-edge semiconductor business that some smaller firms are not able to deliver. In the long-term, Skyworks as enormous growth potential as semiconductor technology and uses will continue to evolve in ways almost unimaginable today, but the speed at which those advances arrive is uncertain.

From a valuation standpoint, the company trades at only 14.06 times future earnings, and analysts are forecasting a 5-year EPS growth rate of 32.0% (according to StockRover).

Overall, Skyworks has tremendous long-term growth prosects, and it has plenty of cash to support its growting dividend which it has already raised four times since being initiated in 2014, including a 14% increase just last quarter.

4. NXP Semiconductors (NXPI), Special Situation

(Suspected Cash Offer Increase Soon)

NXP Semiconductors is a special situation investment opportunity, and our thesis is straightforward: investors are about to receive a lot of cash. If you are not aware, Qualcomm has made a $110 cash offer for NXP (here is the press release from back in October of last year), and we suspect that offer is about to be raised significantly in the coming weeks, at which time the share price will “pop” higher. And even if the deal falls apart (which it might) the share price will still “pop” higher because the terms have been weighing down the price of NXP.

For perspective, here is a look at the recent performance of NXP versus the overall semiconductor index.

Specifically, the price of NXP has been hanging around the deal price of $110 for the last several months while the overall semiconductor industry has climbed much higher. The deal terms, which were announce when NXP’s price (and the semiconductor industry overall) was trading much lower. And considering the recent performance of the market and semiconductors in particular, the deal terms have prevented the price of NXP from climbing higher.

We expect one of two things to happen, and both of them are attractive. First, Qualcomm may be forced to up their offer price. If this happens then the price of NXP quickly moves higher. Second, if the deal is called off, we suspect NXP’s price still moves higher because it is the $110 deal price that has prevented NXP shares from climbing much higher this year. NXP shareholders would welcome the “calling off” of the deal because NXP is now worth more than Qualcomm’s offering, especially considering NXP’s attractive growth opportunities.

(NXP offers innovative products and solutions and a leadership positions in automotive, broad-based microcontrollers, secure identification, network processing and RF power, to name a few. Additionally, the semiconductor industry has tremendous growth opportunities as the number and sophistication of components per device increases and as 5G networks will eventually become reality).

There is a lot more going on here (such as regulatory approval requirements), but the thesis is straightforward. NXP is worth more than its current market price, and we suspect the share price is going significantly higher soon when either Qualcomm ups the offer price or the deal is cancelled altogether.

For your reference, here are some relevant news items about NXP to keep in mind:

- Still waiting on Qualcomm-NXPI deal (9/22/17)

- EU antitrust regulators pause Qualcomm, NXP acquisition decision(9/6/17)

- Morgan Stanley raises NXP Semiconductors price target (8/7/17, Morgan Stanley describes the “win win” scenario of Qualcomm offering a higher bid for NXP).

We'll have a lot more to say about NXP if/when we purchase the shares.

Final Thoughts:

We’ll be placing a new trade soon (to replace the Caterpillar shares we sold). We’ll likely be buying at least one of the four stocks listed in this article. We believe all four of the opportunities described in this article are currently trading at very attractive prices, and we may actually end up purchasing more than one of them for a variety of reasons such as profit taking, portfolio rebalancing, and to take advantage of current market opportunities as we have described in this article. You will be notified via email as soon as we place a new trade. Leave feedback. Stay tuned.

*As a reminder, you can view all of our current holdings here.