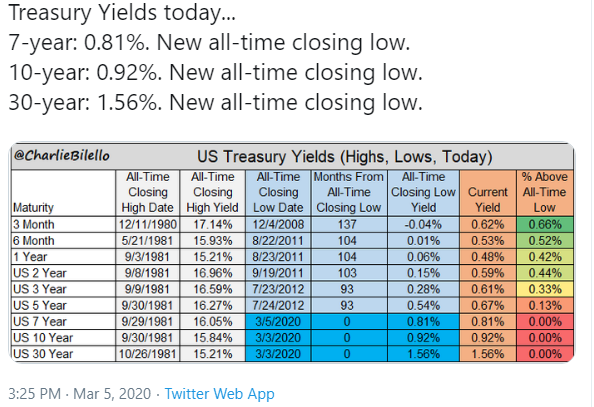

The 10-year US treasury just set a new all-time closing low of 0.92%. And for income-hungry investors, that makes select REIT investments increasingly attractive. For example, consider the big healthy monthly dividend payments of the preferred shares of industrial/office REIT Gladstone Commercial Corporation (GOOD). Not only did market wide fear drive the share price lower (and the healthy dividend yield higher), but it also made it easier for the businesses to refinance its debt, and on a relative basis it made the 6.2% yield that much more attractive. This article reviews the health of the business, the common and preferred shares, risks, dividend safety, and concludes with our opinion about why these big monthly-dividend-paying preferred shares are worth considering for a spot in your prudently-diversified long-term income-focused investment portfolio.

Coronavirus-Induced Rate Cut

In case you have been living under a rock, the market has been selling off hard in recent weeks. Specifically, the market’s recently frothy valuation has been gripped by coronavirus fears, and come tumbling lower. And it is the combination of fear and reality that caused the US fed to cut interest rates by 50bps, just this week. Here is a look at what happened to interest rates, as per US treasuries (courtesy of Charlie Bilello).

The rate cut was intended as stimulus for the economy, but it does a few interesting and positive things for select investments. For example, it makes the big dividend payments by REITs more attractive on a relative basis. Granted, REITs have more risk than US treasuries, but if you are focused on income, would you rather lock your cash up in treasuries for the next 5 years at a 0.67% yield, or would you prefer a few healthy REIT investments that yield over 6%.

Second, as the rate cut is intended to stimulate the economy, it has a positive impact on companies that can now refinance their debts at a lower rate (for example Gladstone, as you can see that company’s upcoming debt maturities in the following table).

Thirdly, the rate cut was the result of concerns about potential negative impacts from the coronavirus. And those concerns had already driven the price of Gladstone’s relatively safe preferred shares lower, and the dividend yield higher—an attractive characteristic for income-focused investors.

Gladstone Overview:

If you don’t know, Gladstone Commercial Corp is a REIT that invests in office and industrial properties globally. The company has a highly diversified portfolio and tenant base. For example, as of February 2020, it owned 122 properties totaling 14.6 million square feet of space across 28 states in the US. The tenants cover a broad cross section of business sectors and range in size from small to very large private and public companies. Its properties are leased to 101 different tenants in 19 industries. Approximately 63% of its tenants have an investment grade or investment grade equivalent credit rating. This is significant as it limits tenant default risk and increases visibility of rental income for the company.

(source: Company)

Also attractive, the portfolio is generally geared toward long-term agreements as evident from its average remaining lease term of 7.3 years. Gladstone enjoys high occupancy rates (currently 97%) and more impressively, the occupancy has never fallen below 96% since its IPO in 2003.

Common Stock Dividends—Healthy in the Near-Term

Gladstone has a strong track record of paying monthly dividends. Specifically, It has paid dividends for 180 consecutive months (15 years). The current dividend yield of ~7.5% (it’s up a bit as the common shares have sold off) is compelling. Further, in January 2020, Gladstone increased the monthly dividend to $0.12515 per share for January, February and March 2020. And while this is only a modest increase (versus $0.125 earlier), it is noteworthy because this is the first dividend increase in over 10 years.

However, despite the fact that Gladstone has shown an impressive ability to grow its revenues over time, this has not translated into funds from operations (FFO) growth. In our view, this is somewhat concerning regarding the health of the common shares in the long-term. More specifically, funds from operations (FFO per share) has not seen any meaningful growth since 2014 despite revenues growing significantly. After peaking at $1.80 in 2014, FFO per share fell to $1.54 in 2015 and since then has been moving around that range. We view the lack of FFO growth as partly due to a failure to control operating expenses and due to high share dilution to fund investments. This is more concerning for the common shares, but not so much for the preferred shares (as we will cover later in this report).

For more perspective, in 2019, Gladstone invested ~$130 million across 14 properties. This is unusually high for a company that generated just ~48 million in LTM FFO. Also, considering the fact that Gladstone’s market capitalization is only ~700 million, such high levels of investments have been funded by issuing more shares. This has hindered FFO per share growth. The company's Q4 FFO per share was $0.39 while its distributions were $0.375 per share. This suggests a payout ratio of 96% which leaves little room for any dividend growth.

source: Company data

Nonetheless, management remains optimistic about delivering meaningful FFO per share growth starting in 2020. According to Gladstone’s CFO, Mike Sodo:

“Our hope is here we can get to a point in time where on an annualized basis, we can demonstrate 1.5% to 3% growth in core FFO on an annualized basis.”

Strengthening Balance Sheet

We are encouraged by Gladstone’s deleveraging efforts (see chart below). For example, its net debt relative to gross assets was 46.1% as of the end of 2019, compared to 46.8% in 2018, the eighth consecutive year of declining leverage. Approximately 65% of its debt is at a fixed interest rate and further 26% is hedged to fixed via interest rate swaps which limits the exposure to interest rates. Nonetheless, the company does have some beneficial exposure to declining interest rates (8.4% floating). And upcoming 2020 and 2021 loan maturities will allow debts to be refinanced at lower rates as well.

(source: Company Data)

Growth Prospects

Gladstone’s management remains optimistic about the company’s growth prospects. For example, the current pipeline of acquisition candidates is approximately $260 million in volume, representing 17 properties, 15 of which are industrial. Of this total, approximately $50 million is either in the letter of intent or due diligence stage, and the balance is under initial review. Per CFO Mike Sodo, during the most recent quarterly call:

“In addition to these accretive deals, our same-store cash rent continues to grow at 2% on an annualized basis. With the number of years of improving the balance sheet behind us, including deleveraging the portfolio, and with substantial acquisitions both at the end of 2019 and early part of 2020, we're excited about the prospects to grow profitability for our shareholders, as well as increasing the industrial allocation of the portfolio. These new investments will provide significant contribution to the Company's performance and aspirations for core FFO growth in 2020 and beyond.”

The higher mix of Industrial allocation will improve property operating efficiencies, reduce capital expenditure levels and potentially result in improved valuation over time. To that end, the industrial allocation was 33% on January 1, 2019 and has increased to 38% by year-end.

Preferred Shares

In addition to the common shares, Gladstone also has two series of preferred shares (7.00% Series D (GOODM) and 6.625% Series E (GOODN)). They’re both cumulative (i.e. if Gladstone misses a dividend payment, they are required to make it up later, so long as they do not go bankrupt). And importantly, the preferred shares are redeemable by the company starting on May 21, 2021 for Series D and October 4, 2024 for Series E). The fixed rate on both series will continue if Gladstone does not redeem them (neither of them have a stated maturity date, and they’re not subject to any mandatory redemption).

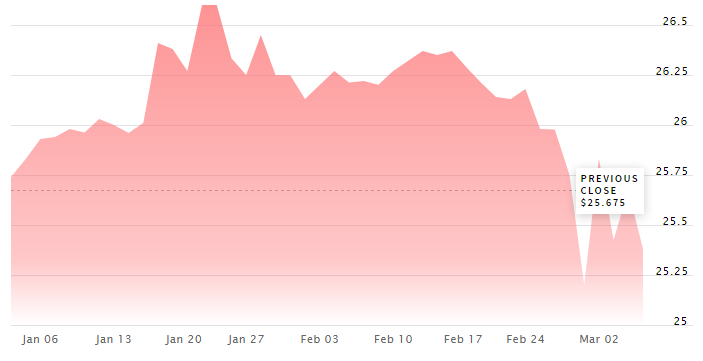

And while both series currently trade at a premium to their redemption price of $25, that premium has come down as the market has sold off, as you can see in the following charts.

source: Nasdaq

In our view, these premiums are acceptable considering the healthy monthly dividend payments. However, of the two series, we prefer the series E shares (GOODN), despite the lower dividend yield, because there is more time until they can be redeemed (2024 versus 2021). Gladstone has a recent history of refinancing preferred shares when they are able. And considering interest rates have fallen (and the company has strengthened its balance sheet) we expect the Series D shares to be redeemed as soon as possible (2021), whereas the Series E shares will likely keep paying until at least 2024. Further, even considering the small price loss (the shares would be redeemed at $25 versus the current price of $26.11) the dividend payments satisfactorily accommodate for this considering the current low interest rate environment.

Overall, we prefer the Series E preferred shares for their healthy dividend (preferred shares are ahead of common shares in the capital structure) and because of their longer time period until they are redeemable (as compared to the Series D shares). If you are an income-focused investor, these big healthy dividend payments are worth considering.

Valuation:

Gladstone’s common shares are currently trading at forward P/FFO multiple of 12.6x. We note that other office REITs such as (Boston Properties and Vornado Realty), are trading in the range of 17-18x, while industrial REITs (such as Duke Realty, Eastgroup Properties, Prologis Inc.) are trading in the range of 25-26x. The company’s lower valuation is partly due to its tight cash flow situation (high dividend payout ratio) and lack of FFO per share growth in recent years. This is also reflected in its relatively higher dividend yield compared to other peers. However, if FFO growth returns as management expects, this valuation gap will narrow and investors could expect solid share price gains.

Risks:

Market cycle sensitivity: Gladstone has a higher sensitivity to the market cycle than some other REITs given that it deals in office and industrial properties, which have higher default risk during times of distress. Nonetheless, we note that Gladstone was able to maintain its dividend during the last recession of 2008-2009. And it has a highly diversified mix of investment grade tenants.

Access to capital: As a REIT, Gladstone’s business model is capital intensive, especially with regards to growth. As such, the company is highly dependent on capital markets. If the company’s financial strength were to decline, it would become increasingly challenging (and expensive) for Gladstone to access capital to fund its business.

Interest rate risk: Even though we expect interest rates to remain relatively tame, dramatically rising rates could create challenges. As REITs are often seen as an alternative to bonds, higher interest rates could mean decreased demand for REITs, thereby causing a decline in the share price. However, we view this week’s Fed rate cut as an incremental positive for Gladstone is multiple ways (e.g. lower cost to refinance debt, increased relative attractiveness of the dividend yield).

Conclusion:

Gladstone is an attractive REIT with a fairly secure high-dividend yield on its common shares (supported in the near-term and mid-term by its FFO generation). There are some concerns about the common shares given their high payout ratio (~95% in 2019). However these uncertainties appear already reflected in the share price given the relatively lower price-to-FFO versus peers. Also somewhat reassuring, Gladstone has now paid its common share dividend for 180 consecutive months (15 years) and announced a modest increase in January 2020 for the first time in over 10 years. We believe the positives outweigh the negatives and the common shares offer an attractive opportunity for investors to generate solid monthly income. However, we prefer the preferred shares.

In particular, we like the Series E preferred shares (which are not redeemable by the company until 2024) despite their premium versus the $25 redemption price (they currently trade at $26.11 and offer a 6.2% dividend yield). Given the volatile market, and the strengthening balance sheet of the business (combined with its growth prospects), these preferred shares are safer than the common shares (preferreds are higher in the capital structure, and if the company were to get into trouble they could reduce the common dividend just to better support the cumulative preferred shares dividend). And while the preferred shares dividend is not as safe as a US treasury, the current record-low yield on US treasuries is not compelling to us compared to the 6.2% dividend yield (paid monthly) on Gladstone’s Series E preferred stock. If you are a long-term income-focused investor, the Series E preferred shares are worth considering for a spot in your prudently-diversified income-focused investment portfolio.