There is a lot of fear mongering surrounding data center REIT Digital Realty (DLR). However, we believe its 3.4% dividend is safe and it will grow, and its price will increase too. This article reviews four fears circling Digital Realty, and then highlights three reasons why we currently like it.

Overview:

Digital Realty is a real estate investment trust engaged in the business of owning, acquiring, developing and operating data centers. Data centers are basically offsite server warehouses where companies store data, often accessible via “the cloud.” As shown in the following table, DLR recently owned 182 data centers across the US and internationally.

DLR owns data centers across a variety of industries ranging from financial services, cloud and information technology services, to manufacturing, energy, healthcare and consumer products.

Digital Realty has delivered strong total returns (price appreciation, plus dividends) over the last 10 years, but has been underperforming over the last year, as shown in the following charts.

Four Fears Plaguing Digital Realty:

1. Rising interest rates are one of the market fears currently plaguing Digital Realty and contributing to its recent underperformance. As a REIT, Digital Realty relies on borrowing to fund growth, and as interest rates are expected to keep rising that makes borrowing more expensive. According to DLR’s annual report:

“We have substantial debt and face risks associated with the use of debt to fund our business activities, including refinancing and interest rate risks.”

However, this risk is offset to some extent by the company’s hedging program, and by the fact that if interest rates keep rising that means the economy is strong which will have a positive impact on DLR’s business. Regarding hedging, here's what DLR had to say in its annual report:

“Approximately 90% of our total indebtedness as of December 31, 2016, was subject to fixed interest rates or variable rates subject to interest rate swaps.”

To a large extent, rising interest rates are already baked into DLR’s price (which is part of the reason the shares have sold off) and it’s the incremental changes to future interest rate expectations that will impact the share price in the future.

Importantly, DLR’s business remains strong, which we will cover in more detail later in this report.

2. The false narrative that “income investing is going out of style” is another one of the fears plaguing Digital Realty. A recent review of market performance shows buyers have strongly preferred growth stocks over income securities in recent months. For example, here is a look at the “growthy” Nasdaq (QQQ) and the Russell 1000 Growth Index vs. traditional income sectors: REITs and utilities.

The surge in growth stocks makes sense considering our booming economy (e.g. strong GDP growth, low unemployment), but that doesn’t mean defensive income sectors (e.g. REITs, Utilities) are going out of style. Many of these companies (such as Digital Realty) continue to generate healthy income and cash flows. And from a contrarian standpoint, it’s not usually a good idea for investors to chase after what has been performing the best in the recent past (e.g. growth stocks).

3. Negative press also has plagued Digital Realty in recent months. Aside from the media pundits fawning all over growth stocks, back in September a prominent venture capitalist gave an overly negative outlook for data center REITs which drove the price lower.

Keep in mind, West Coast venture capitalists are usually more interested in finding the next unicorn (which is a different investment objective altogether) than they are in generating safe steady growing income.

4. Conflicting financials are another fear that has been plaguing DLR. Specifically, DLR has been completing a lot of investment activity that’s made its non-core FFO numbers look “lumpy” and lower than the company’s true cash generation power. The big one was on September 14, 2017 Digital Realty closed the acquisition of DuPont Fabros for about $7.9 billion. Other recent investments include land parcels in Japan and Texas, as well as an agreement to acquire 19-acre data center in Franklin Park, Illinois, for $350 million. The point is that DLR reported a net loss last quarter (Q3) and standard FFO that was lower than the same quarter a year earlier, NOT because the company is in decline, but rather because it’s been spending on attractive future growth opportunities. This is why it's important for investors to focus on core FFO, which adjusts for non-core activities, and core FFO has been growing, and is expected to keep growing, which is a big part of the reason we like Digital Realty: More growth, a safe dividend, and an attractive price. Digital Realty is expected to announce earnings again on February 15.

Three Reasons We Like Digital Realty:

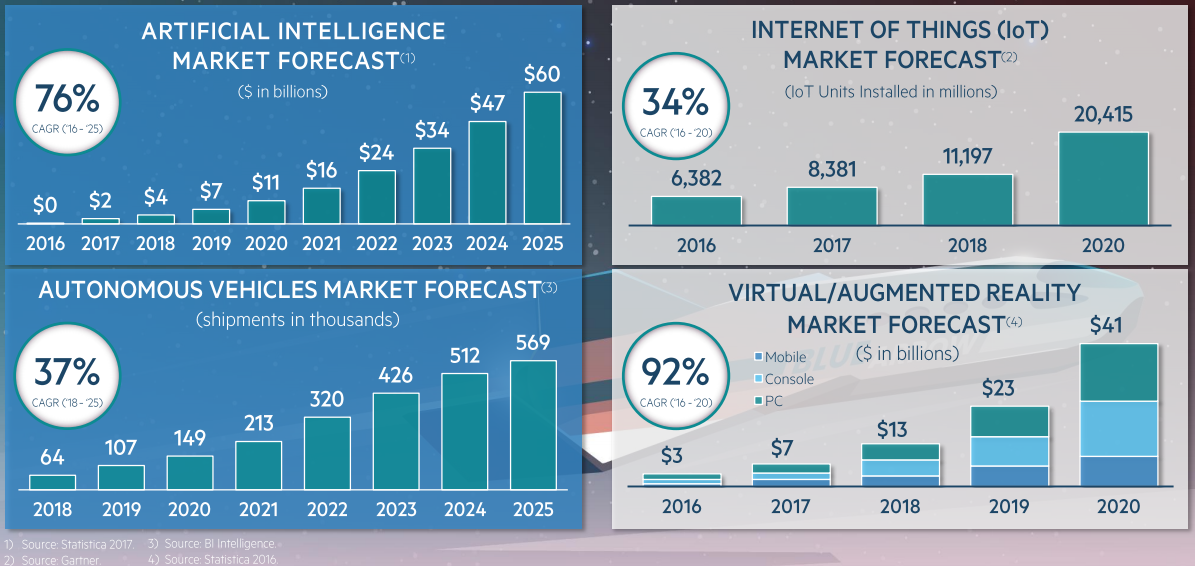

1. A powerful secular trend is one of the reasons we like Digital Realty. Specifically, data centers (especially including DLR) are benefiting from a huge secular growth trend (i.e. companies are moving their data into the cloud, and the amount of data companies need to store is expected to continue increasing rapidly). Data centers will benefit from enormous growth in artificial intelligence, autonomous vehicles, the Internet of Things (IoT), and virtual reality, to name a few.

And DLR expects these trends to benefit its EBITDA positively.

2. Attractive valuation is another reason we like Digital Realty. Specifically, the market appears to not be pricing in the company’s expected growth, as described above. For example, DLR recently provided 2018 Core Funds from Operations (Core FFO) per share guidance of $6.45-$6.60 (which is 8% year over year growth), and the shares still only traded at only 16.2 times 2018 Core FFO (which is a very conservative number, in our view, considering the continuing long-term growth potential). For perspective, at the midpoint of last year, DLR was trading at 18.7 times forward core FFO guidance, and despite the fact that core FFO guidance has been raised, the share price and multiple are both now lower.

3. A safe growing dividend is another reason we like Digital Realty. For starters, DLR currently has a dividend yield of 3.4%, and this yield is very well covered. For example, the bottom line in the following table shows DLR’s adjusted FFO payout ratio is only around 68%, which leaves plenty of room for cushion (i.e. the dividend is very well covered).

Also, DLR management is committed to a secure and growing dividend, and the company has a history of delivering.

And based on the current low dividend payout ratio, plus growth opportunities, we believe the dividend is likely to keep increasing in the future. Remember, DLR has been spending heavily on investments for growth, and these opportunities will literally help pay bigger dividends in the future.

Final Thoughts:

If you are looking for a high-risk high-reward stock that could triple in value over the next six months, Digital Realty is NOT for you. But if you are looking for safe, steady, growing income, along with the potential for healthy price appreciation, we believe Digital Realty is worth considering for a spot within your diversified investment portfolio.