The 3-month total return for most healthcare REITs has been ugly. As shown in the following chart, the group has pulled back as interest rate expectations have increased and investors have been selling “safe-haven” stocks in general. However, two mega-trends underlying the healthcare REIT group remain intact (i.e. demographics are very positive, and healthcare REITs have a relatively long runway for expansion). In addition to reviewing these two long-term mega-trends, this article provides high-level data for more than 20 big-dividend healthcare REITs, and then highlights three specific opportunities that we believe are worth considering.

The growing population of healthcare consumers:

The first mega-trend worth considering is demographics. Specifically, there is a growing population of healthcare consumers, with immense wealth and spending power, and increasing healthcare needs with age, as shown in the following chart.

This trend may be altered by the economy in the short-term, but over the long-term it will not be stopped. And it creates a lot of growth opportunity for healthcare REITs.

Long runway for healthcare REIT expansion:

The next mega-trend is the long runway for growth within the healthcare REIT space. Specifically, the following graph shows the percentage of real estate owned by healthcare REITs versus other categories of REITs.

The key takeaway here is that healthcare real estate may become increasingly owned by REITs, and this creates a lot of opportunity for healthcare REITs to grow. There is a long runway for growth before the space even begins to approach saturation, especially compared to multi-family housing, malls, and hotels.

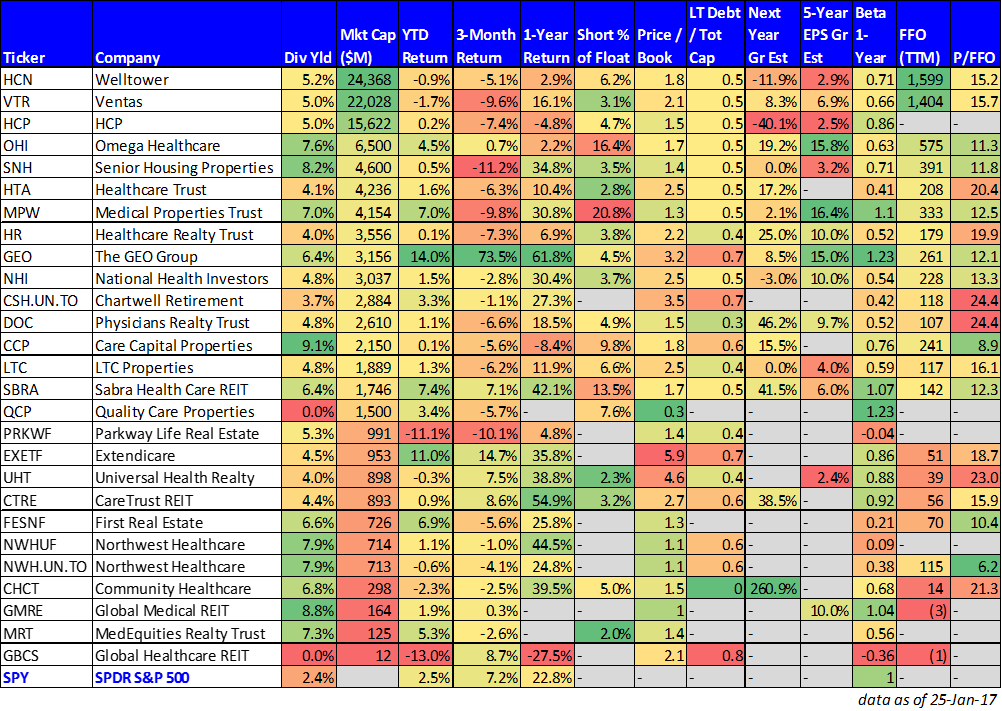

Company Specific Opportunities:

The following table provides additional data points for the 20+ healthcare REITs shown in our earlier performance chart.

As the table shows, 3-month performance has been poor, and dividend yields appear attractive, but it's worth digging deeper into the fundamentals, and we’ve elected to do so in this article for the following three companies.

Welltower (5.2% Yield):

Welltower is one of the more blue chip opportunities in the healthcare REIT space, and its price has recently declined, and its valuation has become significantly more attractive. Besides being the largest healthcare REIT, it pays a big, growing dividend. It’s also well-diversified across senior housing (triple-net and operating), outpatient medical, and long-term post-acute. The “post-acute” is somewhat risky considering other healthcare REITs (such as HCP and Ventas) have been shedding “skilled nursing” exposure because they don’t want to deal with the regulatory reimbursement risks. However, we like that Welltower has some exposure to the upside in that segment.

We don’t currently own shares of Welltower, but we wrote about its attractiveness last August (see: Welltower’s Big Dividend: Weighing the Risks Ahead). Since that time its business has remained strong, and its price to FFO ratio has dropped to a compelling 15.2x. We also like that Welltower rents properties under group leases, rather than separate per property leases, because this makes it harder for tenants to drop underperforming properties.

HCP Inc (5.0% Yield):

HCP Inc. in another healthcare REIT that offers a big dividend yield (currently 5.0%) and it’s trading at a discounted price. HCP has been through the ringer over the last year as it worked to spin-off its underperforming skilled nursing facilities properties to a totally separate REIT, Quality Care Properties (QCP). Many risk averse investors have been shunning both HCP and QCP because they’re uncomfortable with the risks and uncertainty. However, if we look at the combined market capitalization of both HCP and QCP in aggregate, it seems the total valuation has declined more so than other comparable REITs. Granted, QCP’s ManorCare properties are basically a dog with fleas, but there could be an attractive contrarian opportunity here as we wrote about in early August when the spin-off was first announced: HCP’s Big Dividend and Its New QCP Risks. HCP and QCP have much more flexibility now with regards to how they run their businesses (a good thing), and investors now have a choice between HCP and QCP, which opens the stocks up to a wider investor base (also a good thing).

Omega Healthcare (7.6% Yield):

Omega Healthcare Investors is also a skilled-nursing facilities REIT, albeit a less risky one in our view (i.e. they’re not dealing with the same draconian challenges as QCP’s ManorCare). Regardless, Omega’s returns have lagged the S&P 500 over the last year, and it currently has a significantly high “short % of float.” In our view, the market is overly pessimistic, and this is a very compelling, big-dividend, contrarian opportunity. We suspect regulatory risks and concerns are significantly overblown as President Trump has recently pledged to “provided insurance to everybody” under his plan to repeal and replace the Affordable Care Act.

It seems likely that the new administration will not reduce access to healthcare thereby shrinking the size of the healthcare pie (and the healthcare REIT pie), but rather he’ll simplify the laws, giving more control to the people and to businesses (instead of the government) and this will ultimately help skilled nursing facilities reimbursement fears abate (i.e. there will continue to be a growing market for skilled nursing facilities), and it will help Omega Healthcare’s stock price rise (due to less fear and more opportunity).

Conclusion:

Healthcare REITs have gotten a lot cheaper, and their valuations have gotten a lot more attractive, in our view. If you’re comfortable with the near-term volatility as the market adjusts to a new aggressive-growth US president, and you believe in the long-term mega-trends underlying the space, then the REITs highlighted in this article may be worth considering, depending on their particular valuation metrics and your level of aversion to skilled nursing facilities, for example. We’ve made similar data available for Industrial and Retail REITs here: 60 Industrial and Retail REITs Yielding Over 4%. And if you are a long-term income-focused investor, then current market conditions make big-dividend REITs in general worth considering for an allocation within your diversified long-term investment portfolio.