Prospect Capital (PSEC) is an income-investor favorite because it offers an outsized 11.6% dividend yield, paid monthly. However, we believe Prospect is considerably less attractive than it was at this time last year. In fact, we sold our shares of Prospect last week because we believe the market cycle and unintended regulatory consequences may be turning against the company, and its valuation and dividend coverage ratio are becoming decidedly less attractive. In addition to reviewing these big risks facing Prospect, this article also highlights three big dividend investments that we believe are healthier and more attractive than Prospect Capital.

Market Cycle Risk:

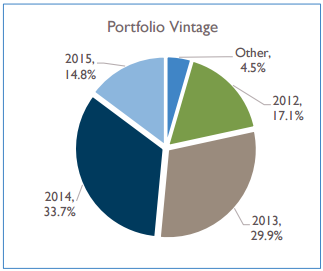

In recent years, Prospect Capital has enjoyed high yields on its debt investments and high returns on its equity investments because that’s what the market cycle gave to Prospect. Specifically, as the economy continued to recover from the financial crisis, Prospect continued to benefit from investments that appeared to be “high-risk” at the time they were made, but turned out to be largely “high-reward” because the market has risen from distress to stability. For perspective, the following chart shows the “vintage years” of Prospect’s investment portfolio which constantly moves further into the future as juicy distress-year investments roll off the books and less-juicy normalized investments roll on.

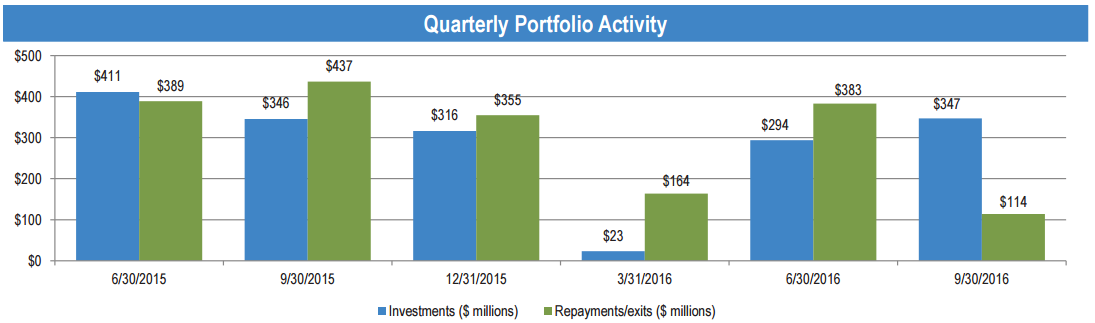

For added perspective, this next chart shows Prospect’s recent quarterly investment activity in terms of what is rolling off each quarter (“Repayments/exits”) and what is rolling on (“Investments”).

And for more color, this next graphic shows Prospect’s portfolio yield, which has been declining recently, and may continue to decline in the future based on market conditions.

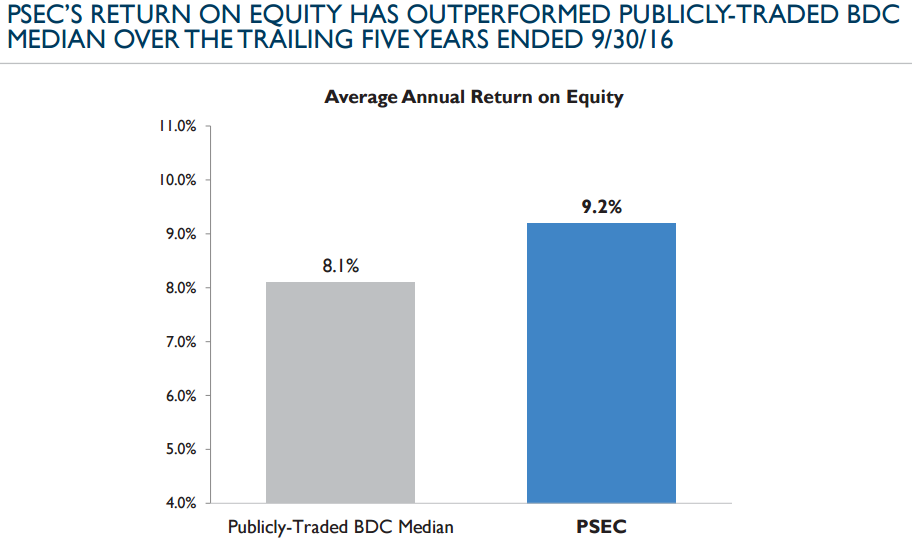

Worth considering, one thing Prospect likes to tout in its quarterly investment presentations is how it has delivered a higher return on equity (ROE) than its peers, as shown in the following chart.

And while ROE is perhaps a more comprehensive performance measurement than the popular net investment income (NII) because, unlike NII, ROE also captures net realized gains and losses, ROE can be misleading. Specifically, as this next chart alludes to, NII/NAV is declining, not necessarily because NII is declining (although it has in the last three quarters, more on this later) but because NAV has been increasing (relative to NII) as distressed assets purchased at distressed prices recover (and as management is perversely incentivized to grow AUM, more on this later).

And the distressed assets have recovered not just because of PSEC’s great underwriting standards, but also because of where we are in the market cycle (i.e. the market/economy has recovered, and while this is out of PSEC’s control, PSEC has certainly benefitted).

For added perspective, this next chart shows Prospect’s declining ROE in recent years as we move further away from the financial crisis vintage year originations/investments.

Worth considering, PSEC trades somewhat similarly to publically-traded high-yield debt as represented by ticker JNK and shown in the following correlation table.

Specifically, PSEC has a higher correlation to high yield debt over the last five years than it has to the S&P 500 (SPY) or to small cap stocks (IWM), which makes sense considering the types of loans PSEC is actually making (i.e. the loans, and equity investments, are being made to relatively higher-risk middle market companies). And for further perspective, high-yield bonds just had a great 2016 (and a great 8-year run, following the financial crisis) which suggest, from a contrarian standpoint, high-yield may not perform as well going forward and neither will Prospect.

For more perspective, this next chart shows the spread (versus Treasuries) for high-yield bonds has come down a lot since the financial crisis (and since early 2016 for that matter- which is important because PSEC was a lot cheaper at the start of 2016), and this suggests Prospect will likely not be able to make the same juicy-yielding investments it made during the financial crisis which it has also benefitted from in recent years because those loans lasted more than just a year or two as inferred from our earlier vintage year chart.

Unintended Regulatory Risks:

The newly-elected president of the United States is strongly in favor of less regulation, however this may have significant unintended negative consequences on BDCs, such as Prospect. As you may have noticed, financial stocks (as measured by the financial sector ETF (XLF)), shot up following November election as investors anticipated less regulation. Specifically, big banks have spent the last seven years shedding risky loans and investments from their balance sheets because of heightened regulations under the Obama administration, and this created somewhat of a boon for BDCs like Prospect (i.e. BDCs, like Prospect, picked up a lot of the business the banks were dumping or unwilling to take due to regulations). However, if regulations are dramatically reduced now, then Prospect could be facing a lot of daunting competition from the big, powerful, deep-pocketed, banks.

Perhaps compounding the risks, Prospect may have gotten “lumped in” with other financials and small caps (Prospect’s market cap is $3.1 billion) following the November election, two categories that soared as shown in the following chart.

However, given the unique risks that Prospect faces (e.g. it may actually get hurt by other financial companies like the big banks, and its high correlation with other small cap stocks, as measured by Small Cap ETF (IWM), as we saw in the earlier correlation table, may be unwarranted), its recent gains may be setting it up for a fall.

Valuation:

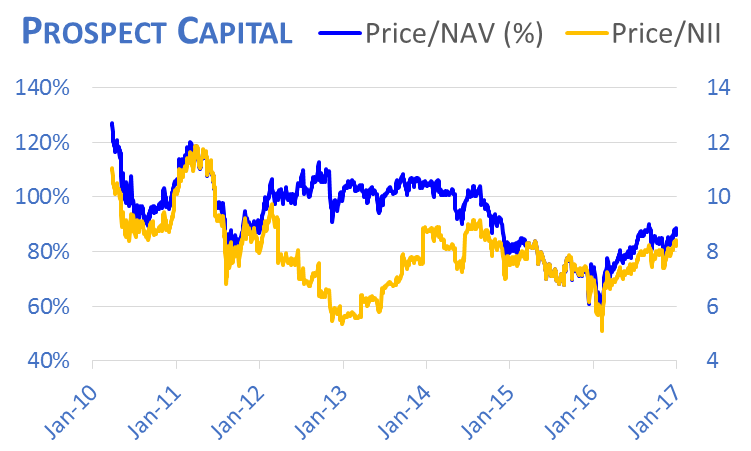

From a valuation standpoint, Prospect is significantly less attractive than it was just one-year ago. For example, the following chart shows Prospect’s current and historical price-to-NAV (Net Asset Value) and price-to-NII (Net Investment Income).

The first thing worth considering is that Prospect’s relative price is significantly higher than it was just one-year ago. And while these valuation metrics may make Prospect look cheap relative to 2010-2014, let’s not forget the market cycle. During 2010-2014 the markets, and subsequently Prospect’s investments, were distressed and thereby offering higher yields and ROEs. That is not the case today, and therefore Prospect should be trading at lower valuation multiples. And at the very least, Prospect is a lot more expensive than it was a year ago, and its prospects do not seem to have dramatically improved, especially considering it may soon be facing heightened competition.

This next chart shows Prospect’s Net Investment Income on absolute basis (in millions of dollars) and on a per share basis.

One thing worth considering in the chart is that absolute NII increased dramatically from 2010 to 2012 as the market wide recovery dictated (it created attractive opportunities) and as Prospect benefitted from big banks de-risking. Next, total NII leveled off from 2012-2015 as PSEC enjoyed the high returns on earlier vintage year investments. And now, at the end of 2016, total NII may be starting to fall off as some of those juicy vintage year investments roll off the books and are replaced with less-juicy investments (a trend that seems likely to continue).

Also, important to note, NII/share is declining in recent quarters which is not a good sign for investors. Further, as we saw in an earlier chart, price-to-NII is rising while NII per share is falling, a discouraging trend.

Also worth considering, this next chart shows Prospect’s historical dividend yield.

And as the chart shows, the yield is still large, but it has come down, perhaps a sign that the valuation may be getting ahead of itself, or simply a sign of lower yielding investment opportunities ahead (i.e. the middle market debt and equity opportunities in which Prospect invests may likely offer lower yields and lower returns going forward considering the market cycle and potential increased competition).

Dividend Coverage:

This next chart, taken from Prospect’s recent quarterly earnings presentation, shows that Prospect’s dividend coverage ratio is narrow (keeping in mind, Prospect is a BDC and regulated investment company, and thereby pays little to no corporate income tax, as long as it pays out at least 90% of its income as dividends).

And in the most recently announced quarter, Prospect paid out more in dividends per share ($0.25) than it earned in NII ($0.22). This is a payout ratio greater than one, which is generally unhealthy and unsustainable over the long-term. And in our view, given our current point in the market cycle, Prospect’s dividend may become increasingly challenging to sustain, particularly if its new originations offer lower yields and if its big ROE continues to decline as it has been in recent years as shown in our earlier chart.

External Management Conflicts of Interest:

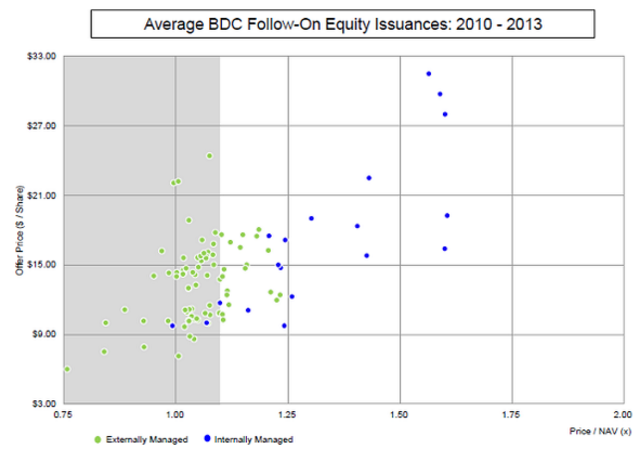

Prospect Capital is an externally managed BDC and this creates conflicts of interest between management (Prospect Capital Management (PCM)), and shareholders. For example, according to Prospect’s most recent 10-K, PCM’s liability is limited under the Investment Advisory Agreement, which may lead PCM to take on higher risk investments. Further, PCM is paid an incentive fee based on NII which can incentivize them to take on higher risk and less profitable investments simply to grow overall NII which is not necessarily in shareholder’s best interest. Additionally, the incentive fee can incentivize management to issue new shares to fund growth in NII (and growth in their incentive fees), but this can be dilutive to existing shareholders considering the shares trade at a discount to the company’s net asset value. For some perspective, the following chart shows new equity issuance for internally managed (blue dots) versus externally managed (green dots) BDCs.

The noticeable observation is that internally-managed BDCs have a track record of issuing new shares at a premium to their net asset values (suggesting investors expect a strong return on assets) whereas externally-managed BDCs have a track record of issuing new shares at a discount to their net asset values (suggesting they're more interested in growing assets under management, total NII and their own incentive fees, instead of focusing on per share profitability for shareholders). Therefore, if you’re going to invest in a BDC, we generally prefer internally managed BDCs (and incidentally, the one remaining BDC we own in our Blue Harbinger High Income Equity portfolio is internally managed).

Three healthier big-dividends than Prospect:

While the high dividend yield and monthly payments offered by Prospect Capital are tempting, we believe there are healthier investment opportunities, that offer outsized dividend payments, as well as better price appreciation potential, and we’ve highlighted three of them below.

1. EPR Properties (EPR)

EPR Properties is a big-dividend retail REIT that we first added to our watch list last summer as an alternative to the then overpriced, lower-yielding, Realty Income, as shown in the following chart.

At the time, we described EPR as an attractive REIT “priced for growth,” but noted that it can be “difficult to hit the buy button on a security that has just rallied like EPR,” and we suggested that income-seeking investors “add this one [EPR] to your watch list, and consider buying on the next pullback.” As the following chart shows, that pullback has arrived, and we believe EPR is an attractive alternative to Prospect Capital because it offers a large dividend payment (5.6% yield) and considerably more price appreciation potential than Prospect, in our view.

2. Omega Healthcare Investors (OHI)

Another big-dividend investment that we consider more attractive than Prospect is Omega Healthcare Investors (OHI), and in this case we actually do own OHI. It yields 7.7%, and has much more price appreciation potential than Prospect Capital, in our view. Our basic thesis on OHI is that it has been overly beat up (we are contrarians) as REITs sold off in recent months (due to rising interest rate fears) and as healthcare stocks have sold off (investors have been particularly fearful of OHI’s exposure to skilled nursing facilities, especially considering the uncertainty surrounding the future of the Affordable Care Act). We believes REITs have sold off too much, we may be about to get more clarity on healthcare laws (the market hates uncertainty), and Omega Healthcare Investors is an attractive alternative to Prospect.

3. Diversified Real Asset Income Fund (DRA)

Sticking with the REIT/real asset theme, we believe Nuveen’s Diversified Real Asset Income Fund (DRA) is an attractive alternative to Prospect Capital because it offers a big 8.3% yield (paid monthly), and it has significant upside potential. The fund invests across the capital structure mainly in common stocks, preferred stocks and corporate bonds, and it focuses on infrastructure and real estate securities. Its objective is to provide current income and long-term capital appreciation. And not only do we like the sector exposures from a contrarian standpoint (real estate as measured by ETF XLRE, and utilities/infrastructure as measured by ETF XLU), but it currently trades at a compelling discount (-12.9%) to its net asset value.

Conclusion:

We sold our shares of Prospect Capital out of our Blue Harbinger High Income Equity portfolio last week, NOT because we believe it is at risk of imminent collapse (we don’t believe it is), but because we do believe it faces increasing risks from the market cycle, new regulations, a frothier valuation, and a challenging dividend coverage ratio, and because we believe there are healthier big dividend investment opportunities available such as EPR Properties, Omega Healthcare Investors, and Nuveen’s Diversified Real Asset Income Fund. In fact, we like Omega Healthcare and the Diversified Real Asset Income Fund so much that we’ve ranked them #6 and #7 on our list of 10 Big Dividends Worth Considering because we consider them healthier and more attractive investments for a long-term, diversified, income-focused investment portfolio than Prospect Capital.