AmeriGas is the largest propane distributor in the US (with about 15% retail market share), it’s organized as a master limited partnership (MLP), and it currently pays a big safe growing distribution yield of 8.2% (paid quarterly). Additionally, AmeriGas offers low volatility, a low beta, and an exceptionally attractive return on invested capital. Further, AmeriGas is uniquely positioned to successfully execute on its growth-through-acquisitions strategy, and fears of a declining propane market are largely overblown. And despite the recent rebound in the stock price, the valuation is still very attractive for long-term investors. Overall, we believe AmeriGas’ big distribution payments are very safe, and long-term investors may want to consider adding this MLP to their diversified income-focused portfolio.

About AmeriGas

AmeriGas sells propane to over 2 million customers across all 50 states through its approximately 2,000 distribution locations. If you don’t know, Propane is a by-product of natural gas processing and petroleum refining. It is used for home heating, space heating, water heating, cooking, grilling, and motor fuel, to name a few. The company has been around since the 1950’s, and it is currently the largest marketer of propane in the United States.

AmeriGas by the Numbers

AmeriGas has a long history of increasing its attractive distribution payments, it has a low beta, low volatility, and a very attractive return on its invested capital. For starters, AmeriGas currently pays its unitholders $0.94 per quarter which amounts to an 8.2% yield. And as the following chart shows, it has a long history of increasing its distribution payments (12 years in a row, actually).

AmeriGas also offer attractive diversification benefits and lower volatility. For example, its beta is only around 0.2 which means it is less sensitive to systematic market-wide risks than other typical investments. It also means AmeriGas can offer very important diversification benefits to risk averse investment portfolios. Additionally, AmeriGas is less volatile than other big yield investments. For example, we compared the daily and monthly volatility of AmeriGas to other big yield investments over the last year-to-date, 1-year, 3-year and 5-year periods, and found AmeriGas to exhibit significantly less absolute volatility (this is different from “beta” because it’s absolute volatility instead of volatility relative to the overall market as measured by beta). Our analysis included over 200 equity securities with yields greater than 5%, revenues greater than $100 million, and market caps greater than $500 million. For your reference, here is an abridged view of some of the most and least volatile big yield securities.

AmeriGas also offers a very attractive return on capital versus its cost of capital. According to the reasonable assumptions at GuruFocus, AmeriGas’ weighted average cost of capital (WACC) is only 4.14%, and its return on invested capital is 11.58%. This is an exceptionally wide margin, and it means it only costs AmeriGas 4.14% to raise capital, and they can turn around and earn a return of 11.58% on that capital. This is a very profitable spread.

Growth through Acquisitions

According to AmeriGas’ most recent annual report “Our strategy is to grow by (i) pursuing opportunistic acquisitions, (ii) developing internal sales and marketing programs to improve customer service and attract and retain customers, and (iii) leveraging our scale and driving productivity.” It’s important to note that acquisitions are listed first. Acquisitions have been the largest part of the company’s growth strategy, and AmeriGas is uniquely positioned to pursue this strategy for two reasons. First, they have a large footprint across all 50 states, and second they currently have only 15% of total market share which means there is a lot of room for growth. AmeriGas describes both of these in their annual report as follows.

Our acquisition program reviewed many opportunities in 2015 and closed on nine small-scale propane acquisitions of quality local businesses with good synergies when combined with our local stores. Our national distribution footprint creates significant synergy opportunities in almost every deal we pursue and there are over 3,000 targets remaining, which means there is plenty of opportunity for further consolidation within the industry.

However, as AmeriGas continues to get larger, it needs to seek larger acquisition targets to drive meaningful growth. Fortunately, the propane industry is still very fragmented, and this creates plenty of opportunities for more growth though larger acquisitions. Some of the larger propane-related companies are included in the following table, and acquisitions/mergers for these companies may become a growing possibility in the years ahead.

And with regards to growth, it is worth considering the secular trend within the propane industry. There are some fears that the industry may shrink too quickly for AmeriGas to meaningfully grow. However, this narrative may be overblown. For starters, AmeriGas describes the industry in their annual report as follows: “the retail propane industry has been declining over the past several years, with no or modest growth in total demand foreseen in the next several years.” (Annual Report, p.10) However, the Propane Education & Research Council provides a more optimistic view of the industry explaining “the decline in oil prices and the corresponding decline in propane prices in 2014 and 2015 provides a window of opportunity for propane to increase market share in traditional markets that have been hurt by higher propane prices in the last five years.” We believe that the “growth-via-acquisitions/consolidation” strategy greatly overshadows the risk of slow or no propane industry growth. Therefore AmeriGas still has a lot of room for future growth.

Valuation

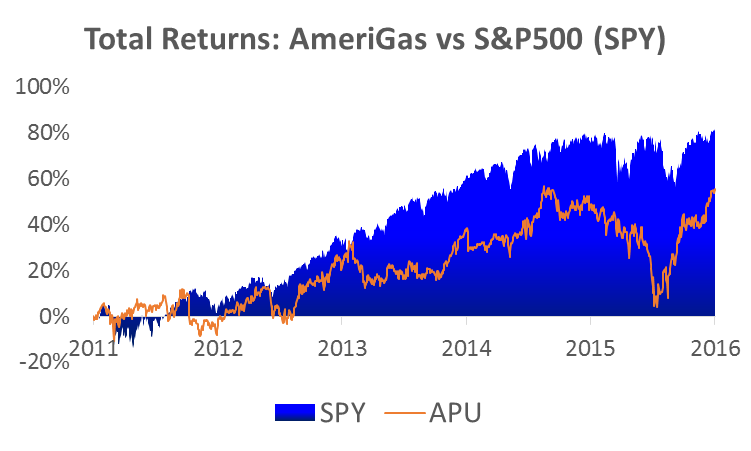

Despite the recent rebound in AmeriGas’ stock price (as shown in the following chart), we believe it is still trading at an attractive valuation.

For example, a basic discounted cash flow model suggests the company is worth roughly twice its current market price. Specifically, if we discount 2015 free cash flow of $421.85 million (cash from ops of $523.86 million minus capex of $102.01 million) by the 4.14% WACC and assume a zero percent growth rate then AmeriGas is worth $10.2 billion or almost $110 per share (Google Finance). Similarly, a distribution discount model suggests the company is worth even more. Specifically, if we discount the expected 2016 distribution payments of $349 million ($0.94 per share times 92.92 million shares) by the cost of equity 3.16% and assume a conservative zero percent growth rate (management’s actual goal is to grow the distribution by 5% annually) then AmeriGas is worth over $11 billion. These valuations use a variety of assumptions that are subject to discretion (for example the cost of equity capital is very low because the beta used in the CAPM equation is very low), but the point is that both valuation metrics suggest AmeriGas is not overvalued.

Other ways to think about AmeriGas’ valuation include considering its growing free cash flow, it’s price to free cash flow (versus history), and its cash distribution payout ratio (versus historical levels) as shown in the following charts.

These charts demonstrate AmeriGas’ strong growth, and also suggest that it is not overvalued.

Risks

It’s also important to consider some of the more significant risk factors that AmeriGas faces. For example, warmer weather poses a risk (demand decreases when the weather is warmer) and this has been a challenge for the company recently, but could just as easily work to the company’s advantage in the future. The availability of new/attractive acquisitions targets also poses a risk, however as we discussed previously we believe there is still plenty of room for big acquisitions in the future. Competition is another risk. For example, the barriers to entry in the industry are low. Additionally, AmeriGas’ MLP structure poses a risk. For example, AmeriGas faces limitations on how it can operate its business and still qualify as an MLP. Also, the management structure of AmeriGas creates risks. For example, AmeriGas has an agreement with Energy Transfer Partners that could delay or prevent a change in control, which could adversely affect the price of AmeriGas common units. Also, UGI owns 26% of AmeriGas, and has significant control over the company (limited partner unitholders have very little in terms of voting rights).

Conclusion

We believe AmeriGas is an attractive MLP, and its big growing distribution payments are likely safe for many years to come. Specifically, we like AmeriGas so much that we’ve ranked it no. 20 on our list of 20 Big Yield Investment Worth Considering because of its low risk, attractive valuation, and unique positioning to execute on its acquisition strategy. If you are a long-term investor, AmeriGas could be a valuable addition to your diversified income-focused portfolio.