Automatic Data Processing (ADP) is an attractive stock to own. It’s a stable, highly profitable, human capital management (HCM) company with a large and growing dividend. However, because of ADP’s large business with large companies, an important subplot within the HCM industry is easily overlooked. Specifically, as the benefits of cloud-based solutions have become obvious in recent years (i.e. they’re cheaper and more convenient) a high-stakes race has emerged to capture as much small company, cloud-based, HCM new business as quickly as possible. In addition to being cheaper and more convenient for customers, cloud-based HCM solutions are also very profitable for providers (i.e. they’re high margin, and once you’ve captured the business it is unlikely to leave). As a result, companies like Paycom (PAYC) and Ultimate Software (ULTI) are spending enormous amounts of money to capture new business now because they know the heavy spending will be unnecessary in the future and the business will eventually turn into an impressive cash cow.

We like ADP: It’s stable, highly profitable, offers an attractive dividend, and it’s not overvalued.

If you’re not familiar, ADP provides a range of software and services to help companies recruit, staff, pay, manage and retain employees. And as the following chart shows, ADP’s revenues and profits are very large and fairly stable:

A big reason for the stability is the high customer retention rate. For example, ADP’s worldwide client revenue retention was 91.4% in fiscal 2015 (Annual Report, p.26). This steady stream of business helps reduce the company’s volatility, and it also helps the company pay a healthy dividend (i.e. ADP has an above average 2.5% dividend yield).

Additionally, ADP’s stable business generates lots of free cash flow so it can continue to increase the dividend as well as repurchase shares. The following chart shows ADP’s free cash flow over the last several years:

Specifically, in fiscal 2015 ADP paid dividends of $927.6 million and returned $1,557.2 million in cash through their share buyback program (ADP Annual Report, p.20). The company also has a track record of increasing the quarterly dividend for 40 consecutive years.

ADP is able to increase the amount of cash retuned to shareholders because it is growing at only a moderate pace. Sources of growth for ADP include economic growth (ADP generally grows as the economy grows), international growth (the company is working to expand outside the US), and rising interest rates (management estimates that a change in both short- and intermediate-term interest rates of 25 basis would result in approximately a $12 million impact to earnings from continuing operations) (Annual Report, p.33). However, ADP would not be returning any cash at all to shareholders if they had the same aggressive growth opportunities as some of their smaller competitors (more on this later).

A basic discounted free cash flow model suggest the market is expecting ADP to grow at an annual rate of about 4.4% (we divided fiscal 2015 FCF by the WACC [8.4%] minus the growth rate to back into the current share price). A 4.4% growth rate is not unrealistic given the company’s growth opportunities. And realistically, ADP will likely achieve a higher growth rate given its current trajectory. For example, analysts surveyed by Yahoo Finance expect earnings to grow at an annual rate of 10.4% over the next 5 years, and management has already provided guidance for 7-8% revenue growth in 2016 (ADP Earnings Release).

We like Paychex for the same reasons as ADP, plus it has a bigger dividend.

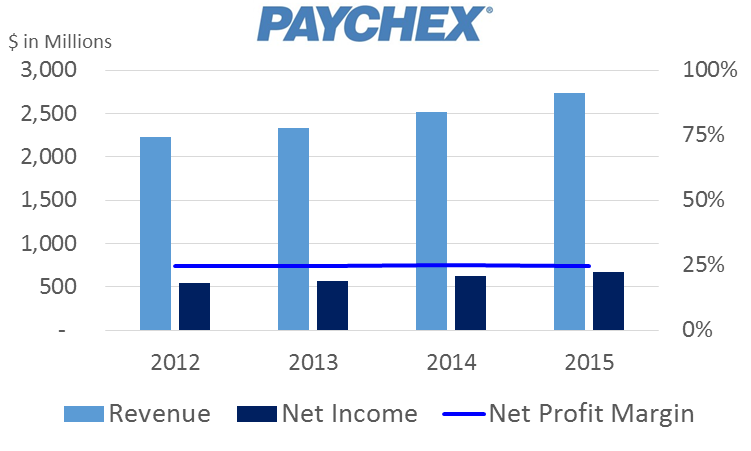

Like ADP, Paychex (PAYX) is an HCM company with large and fairly stable profits. And while Paychex market capitalization is smaller than ADP’s ($19B vs $39B), the following chart shows Paychex’s profit margin is higher:

Like ADP, Paychex also generates an impressive stream of FCF that can be used to grow the business or return to shareholders (i.e. share repurchases and dividends).

For example, Paychex used it’s FCF to repurchase shares ($182.4 million in FY 2015) and pay dividends ($551.8 in FY 2015) (source: Google Finance). And specifically, PAYX dividend payments amount to an impressive 3.2% dividend yield (significantly higher than ADP). For investors interested in a stable, high dividend yield, Paychex is worth considering.

However, also like ADP, if Paychex had better organic growth opportunities then they’d be using all of their FCF to grow the business instead of returning it to shareholders. In fact, Paychex explains that it seeks inorganic “growth through strategic acquisitions” (source: Google Finance description). This is in contrast to ADP’s strategic goal to grow organically (one of ADP’s three strategic pillars is to “grow a complete suite of cloud-based HCM solutions, Annual Report, p.3). Paychex’ interest in strategic acquisitions may include aggressive growth cloud-based competitors Paycom (PAYC) and Ultimate Software (ULTI), but more on these companies later.

A basic discounted free cash flow model suggest the market is expecting PAYX to grow at an annual rate of about 4.9% (we divided fiscal 2015 FCF by the WACC [9.1%] minus the growth rate to back into the current share price). A 4.9% growth rate is not unrealistic given the company’s growth opportunities. Somewhat similar to ADP, Paychex growth opportunities include economic growth, aggressive sales initiatives, strategic acquisitions (Paychex, not ADP), and rising interest rates. And realistically, Paychex may achieve a higher growth rate given its current trajectory. For example, analysts surveyed by Yahoo Finance expect earnings to grow at a rate of 9.5% over the next 5 years, and management has already provided revenue and earnings growth guidance of 7-8% and 8-9%, respectively, for fiscal year 2016 (Q1’16 Earnings Release, p.3).

If you like more risk, ADP’s cloud competition may offer a lot more reward.

ADP and Paychex are experiencing increased HCM competition from cloud-based software companies such as Paycom (PAYC). Unlike ADP, Paycom’s solution requires no customization and it is maintained in a single database for all HCM functions. This is particularly attractive to newer (and usually smaller) companies because they’re not bogged down by legacy systems and databases that they must maintain. To many companies, Paycom is simply a better, more cost-effective solution. And to drive home this point (and attract more business) Paycom has been spending very aggressively on sales and marketing.

The following chart shows Paycom’s increased spending on “Sales & Marketing,” as well as the resulting increase in revenues and net income. For example, spending on “Sales & Marketing” has increased from $22 million in 2011, to $29 million in 2012, $43 million in 2013 and $64 million in 2014 (Paycom 2014 Annual Report, p.37). The reason for the aggressive increase is because it increases revenues. Over the same period, revenues have grown at roughly 40% per year.

And while net income has been miniscule over this period, it will likely increase dramatically in the future for two reasons. First, as revenue continues to grow, economies of scale will help minimize the drag caused by fixed costs. But more importantly, when the heavy spending on “Sales & Marketing” eventually ceases, the revenues will remain high (because the business retention rate is so high), and Paycom will likely turn into a highly profitable cash cow.

Paycom currently trades around $38 per share, but it could be trading as high as $103 per share just over five years from now. For example, if revenues continue to grow at 40% for the next five years (management is already forecasting 47% growth for this year) then revenue could be as high as $845 million in 2019. Assuming the company significantly reduced its “Sales & Marketing” thereafter in order to simply focus on existing customers, then net income could be as high as $217 million in the following year assuming a 25% net profit margin. Assigning the same 28 times multiple that ADP currently receives, would give Paycom a market price of around $103 per share (roughly 171% higher than its current market price). Obviously, we’ve made some very broad assumptions here, but the point is that Paycom’s stock has very significant upside potential.

Ultimate Software (ULTI) is another cloud-based HCM software company that has been spending very heavily on sales and marketing in order to capture business and grow revenue. The following table shows the big increases in “Sales & Marketing” have caused revenues to increase around 23% per year.

We value ULTI using management’s 2015 and 2016 revenue growth guidance (22% and 23%, respectively) combined with a 17.5% growth per year for the following three years and then 2.5% each year thereafter to come up with possible 2020 revenue and net income of $1.3 billion and $316 million, respectively. And using the same 28 times multiple, suggests the stock could trade as high as $309 per share, giving it nearly 100% upside versus its current market price. Again, we are making some very big assumptions, but the point is that Ultimate Software stock has some very significant upside potential.

Worth noting, Ultimate Software and Paycom may be attractive buyout targets for larger industry players (for example Paychex) because all three of the companies generate lots of free cash flow and have little to no debt on their balance sheets. Plus, both PAYC and ULTI have relatively small market capitalizations. We are not interested in investing in Paycom or Ultimate Software simply as potential buyout targets, however they are both somewhat attractive in this regard, and if they do get bought out it will likely be at a large premium to their current stock prices.

Conclusion:

We like ADP. It’s a steady growth business, it’s not over-valued, and it offers an above average dividend. We also like Paychex for most of the same reasons as ADP, plus it pays an even bigger dividend. However, we believe some of the smaller cloud-based software competitors have much more upside potential than ADP and Paychex, albeit with more risk. The four companies mentioned in this article are just some of the players in this industry that are racing to capture new business market share as quickly as possible because of the high margins and high retention rate. We’ve reserved our favorite player in the space for Blue Harbinger Stocks subscribers, however this excerpt from our November 28th Blue Harbinger Weekly will give you a pretty big hint:

Our favorite cloud-based small cap holding is up 31% in the last month, and it beat the market again this week despite the broad sell off we are experiencing. If you are a diversified long-term investor, there is no reason to change your strategy just because volatility has picked up. Buying and holding quality stocks is a proven winning strategy.

Overall, we believe Human Capital Management is a steady growth industry that will benefit from a secular trend towards cloud based solutions. Additionally, because of the amount of client payroll cash some of these companies keep on their books, a rising interest rate environment will be a helpful tailwind.