Investors are hungry for yield. And as interest rates have remained depressed since the financial crisis, many investors have flocked to high-dividend stocks like AT&T. However, AT&T is a company in decline. Its wireline business continues to decline, and its wireless business can no longer grow fast enough to offset the declines. AT&T’s relatively recent purchase of DIRECTV was a short-sighted decision to acquire a sputtering stream of free cash flows in order to postpone an AT&T dividend cut. We believe AT&T’s very high 5.6% dividend yield is a red herring meant to distract investors from recognizing the company’s lack of long-term total return opportunities.

AT&T’s wireline business has been declining for years.

It should come as no surprise to anyone that AT&Ts wireline business has been declining for years. AT&T sums it up nicely in their most recent annual report (p.24) by saying:

“Wireline… will face continued competitive pressure in 2015 from multiple providers, including wireless, cable and other VoIP providers, interexchange carriers and resellers. In addition, the desire for high-speed data on demand, including video, and lingering economic pressures are continuing to lead customers to terminate their traditional local wireline service and use our or competitors’ wireless and Internet-based services.”

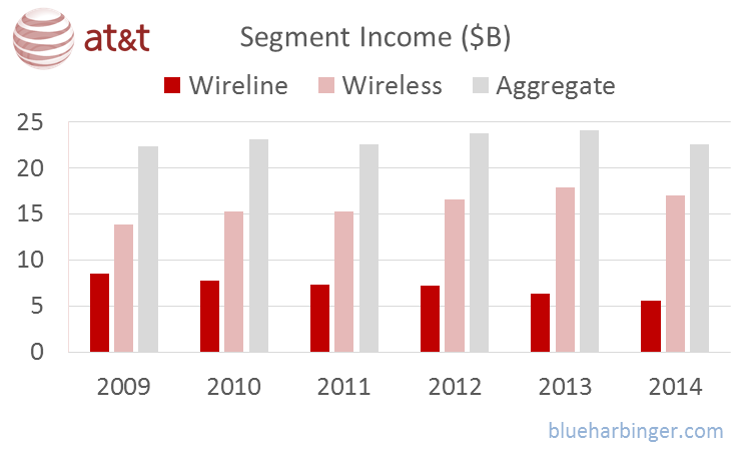

And per AT&T’s third quarter earnings release total wireline voice connections added only $22.8 billion in revenues during the quarter versus $26.2 billion for the same quarter a year earlier. And looking back even further we can see that AT&T’s wireline segment added $5.6 billion in income during 2014, down from $6.3 billion in 2013, and down from $7.2 billion in 2012, and down from $7.3 billion in 2011, and down from $7.8 billion in 2010, and down from $8.5 billion in 2009. (2014 and 2011 Annual Reports, pp. 17 and 37, respectively).

AT&T’s wireless business is no longer able to offset the declining wireline business.

For some time (see table below), growth in AT&T’s wireless segment was able to offset declines in its wireline segment, but that is no longer the case as wireless penetration becomes increasingly saturated and competition puts downward pressure on profitability. For example, AT&T’s Wireless segment income declined in 2014 for the first time in over five years (2014 and 2011 annual reports pp.51 and 33, respectively).

The declines are due to increasing market saturation and a variety of competitive forces (more on competition later).

AT&T bought DIRECTV so it could postpone a dividend cut.

AT&T has been paying out around $10 billion per year in dividends, but the company’s free cash flow from which it pays the dividend has been declining. For example, free cash flow was only $10.2 billion in 2014, down from $14.6 billion in 2011, and $17.9 billion in 2009 (2011 Annual Report, p.59) Realizing the imminent cash flow problem, AT&T’s management needed to do something to maintain the company’s 31-year track record of increasing the dividend. Or worse, they risked losing shareholders in droves if they ran out of cash and had to cut the dividend.

Management’s solution was a short-term fix. Specifically, they structured a deal to acquire the sputtering free cash flows of DIRECTV in a way that reduced AT&T’s aggregate dividend payout ratio while maintaining the amount of dividends paid per share. More specifically, AT&T paid $48.5 billion using a combination of debt and stock to buy DIRECTV (AT&T press release) . And this resulted in a reduction in the percent of free cash flows to be paid as dividends. AT&T expects 2015 total free cash flow to increase to at least $15 billion (because they get DIRECTV’s free cash flows now) and they will only pay around $11.6 billion per year in dividends going forward because of the way they structured the deal. It’s a clever short-term fix, but it is not a long-term solution considering the declines the satellite TV industry is facing. In fact, AT&T seems to have bought DIRECTV just as the satellite TV industry was peaking.

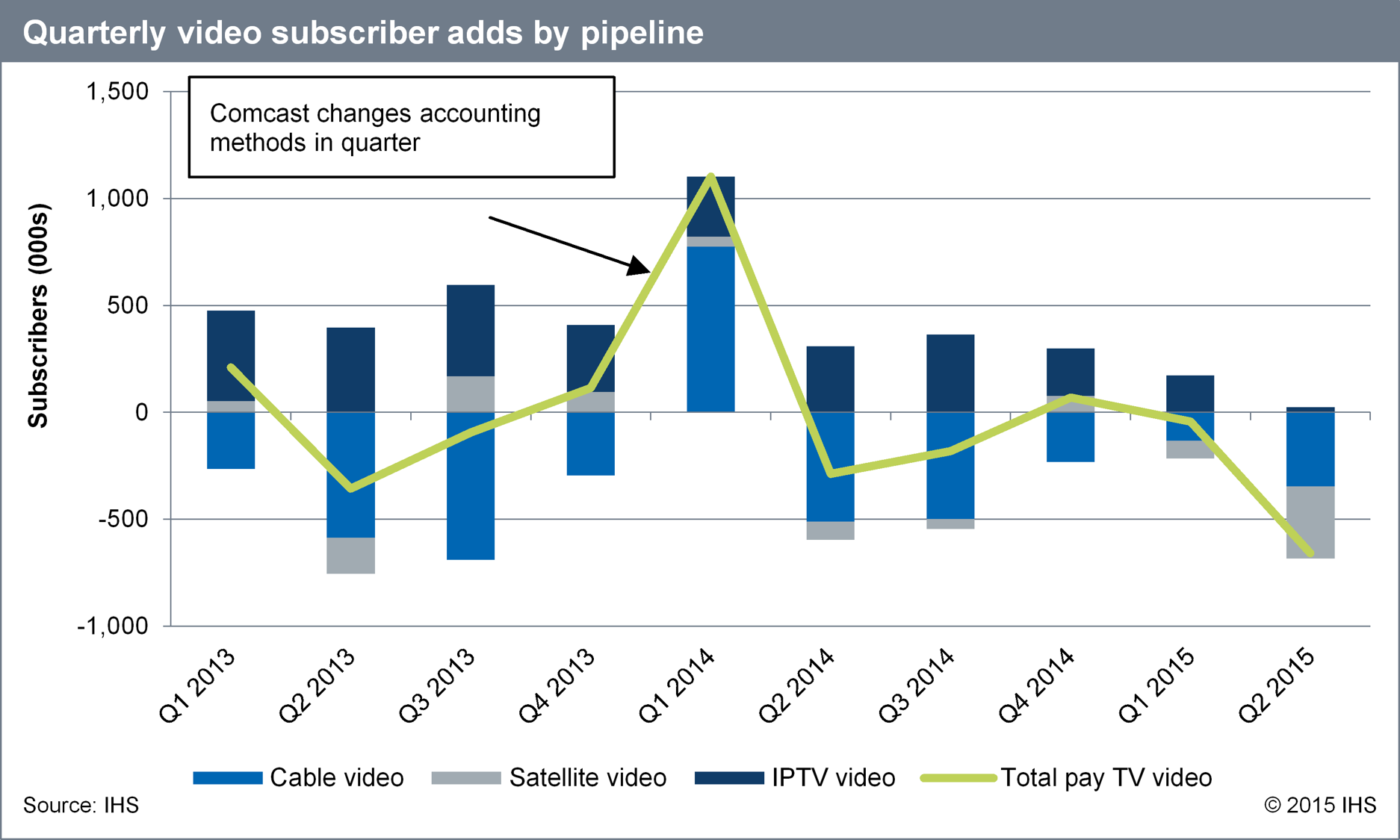

According to market information provider IHS, DIRECTV lost 133,000 subscribers in the second quarter of 2015. This is a threatening dynamic for AT&T and the industry in general as more people are giving up on their pay TV subscriptions altogether.

And while AT&T claims to have added back 26,000 DIRECTV subscribers in the third quarter, they also lost 91,000 U-verse video subscribers in the same quarter (Investor Briefing, p.5). AT&T claims to be focusing more on profitability and satellite sales (DIRECTV) in particular, but the accelerating trend of people giving up pay TV altogether is a significant threat to AT&T’s business. The challenge for management is to stop the declines (or at least slow them). And while they may find ways to increase the stickiness of subscribers by bundling pay TV services with Internet and phone offerings, it’s still a significant threat to AT&T’s business.

What is AT&T worth?

A basic discounted cash flow model suggest the market is expecting AT&T to shrink at about 1% per year into the future. Using management’s $15 billion 2015 free cash flow target, an assumed 6% weighted average cost of capital, and AT&T’s current stock price, we can back into the negative 1% annual growth rate. And if AT&T does resume its negative growth rate then it will eventually run into the same cash flow problem it had before the DIRECTV acquisition (i.e. AT&T will eventually not be able to pay its high dividend yield). However, if AT&T can simply maintain its current level of business (i.e. it neither shrinks nor grows) then it is worth around $41 per share giving it over 20% upside versus its current share price.

Stopping its business from shrinking seems unlikely for AT&T. For example, there is likely a floor to AT&T’s wireline business declines, but based on the accelerating rate of decline in recent years, AT&T has not yet reached that floor and further declines seem imminent. Also, AT&T’s wireless business seems likely to face continued pressure going forward given the intense competition in the industry with regards to service and price. And AT&T’s newly acquired DIRECTV business seems to be facing accelerating challenges with more people giving up pay TV altogether. Perhaps AT&T can slow the rate of decline by bundling its services (Internet, phone and pay TV) in a way that makes it harder for people to leave. For example, it seems people are much more likely to give up TV than Internet, and AT&T may be able to offer compelling bundled pricing discounts that at least slows the rate of decline.

Also, important for investors to recognize, if AT&T’s stock price continues to stay right where it is while the rest of the market grows (this is essentially what has happened in recent years) then the opportunity cost is great. A 5.6% dividend yield with 0.0% capital appreciation is not attractive. Further, the notion that AT&T is somehow more safe if the market crashes is not accurate, considering AT&T’s stock price fell right along with the rest of the market during the financial crisis which wasn’t that long ago.

Additionally, AT&T has increased its risk level by purchasing DIRECTV because it increased debt, and added a significant level of business that is much more sensitive to economic cycles and conditions than AT&T’s traditional low beta operations.

What additional challenges and risks does AT&T face?

In addition to the challenge of not shrinking, AT&T faces a variety of additional noteworthy risks and challenges ranging from intense competition, regulation, pension funding, a unionized work force, and less-than-perfect management incentives.

Competition: AT&T faces intense competition on a variety of fronts. From a wireless standpoint, AT&T faces competition from brands such as Verizon, Sprint and T-Mobile. As noted in AT&T’s most recent annual report, more than 98 percent of the U.S. population lives in areas with at least three mobile telephone operators, and almost 94 percent of the population lives in areas with at least four competing carriers. Additionally, AT&T faces competition from newer technology alternatives such as those that offer voice, text and other services as applications on data networks. Competitors compete on service/device offerings, price, call quality, coverage area and customer service. And from a wireline standpoint, AT&T continues to lose customers as they terminate their traditional service and use competitors’ wireless and Internet-based services due to their desire for high-speed data on demand, including video, and due to lingering economic pressures.

AT&T also faces competition from a video content perspective. For example, AT&T’s U-Verse and DIRECTV both face intense pressure from cable providers such as Comcast, and from satellite providers such as Dish Network. Further, a growing number of customers are shutting off traditional video content services in favor of alternatives such as Netflix and original content from Amazon.

Regulation: AT&T operates in a highly regulated industry. For example, governments control spectrum, which is essentially the airwaves over which wireless communication is transferred. And more spectrum is required as customer needs increase. For example, AT&T notes in its most recent annual report: “Over the last eight years, mobile data traffic on our wireless network increased 100,000 percent – driven by people downloading and sharing videos.” AT&T has been able to stay ahead of its customers’ needs by obtaining additional spectrum through the acquisition of Leap Wireless, and through government auction.

Additionally, in some instances, AT&T needs approval from the Federal Communications Commission (FCC) to operate. For example, AT&T needed approval from the FCC for the DIRECTV acquisition, and it took the FCC over one year to provide approval. Further, as part of the approval, the FCC mandated AT&T expand Internet services to more homes.

Net Neutrality is another example of regulatory challenges AT&T faces. For example, on page 5 of its most recent annual report, Chairman and CEO Randall Stephenson expresses a great deal of frustration with policy makers for taking the concept of net neutrality way too far. Stephenson explains the regulations are a threat to the United States’ continued global leadership in technology and innovation, and explains that AT&T will take legal actions in the courts if necessary.

Pension Risks: AT&T faces enormous risks related to its antiquated defined benefit pension plan. Most organizations have wisely moved to defined contribution plans to shift the risk from the employer to the employee. However, because of its long history, AT&T still has a significant amount of legacy defined benefit obligations.

One of the first things that jumps out about AT&T’s defined benefit plan (besides its enormous size) is the absurdity of the plan’s return assumptions. AT&T assumes their defined benefit plan will return 7.75% per year over the long-term (Annual Report, p.25). This is a reasonable assumption for a 100% equity plan, but AT&T has invested only 37% of the plan’s assets in equities. The remainder is 38% fixed income, 11% real assets, 12% private equity and 2% other (we’re assuming “other” is likely cash a derivatives) (Annual Report, p.67). The 38% fixed income won’t return anywhere near 7.75% considering the current low interest rate environment, and the fact that the plan’s fixed income future returns will likely be depressed if/when the fed start raising rates (which it is widely expected to do within the next year). The 11% real assets is probably meant to be an inflation hedge, which means it will likely return about 2% over the long-term (minus management fees and plus a lot of volatility). And the private equity allocation might return about the same as the public equity allocation in the long-term after factoring in the very high fees private equity managers charge.

The plan has achieved more than its current 7.75% target over the last several years as noted in the table below, but this occurred only because of the unprecedented and enormous quantitative easing completed by the US Federal Reserve in recent years in order to pull the economy out of the Financial Crisis.

The data in the table above (taken from AT&T’s historical annual reports) shows that the typical change in the plan’s underfunded status closely matches the difference between the actual return and the benefits paid. Therefore it seems AT&T will become significantly more underfunded at the end of 2015 given the lower market returns we’ve seen year-to-date (i.e. the plan will fall short of its 7.75% return target this year). Further, it seems the plan will become even more underfunded in the future given its asset allocation and its overly aggressive return assumptions. And as the plan becomes more underfunded, AT&T will likely make big contributions in the hundreds of millions of dollars per year (or even multiple billions of dollars per year). And these big contributions will be very significant to the overall health of AT&T considering its annual net income level (for example, net income is only around $9.3 billion for the first 9 months of 2015, and it’s been considerably less in recent years). The bottom line here is that AT&T’s defined benefit plan poses significant risks to the future health of AT&T.

Unionized Workforce: As of January 31, 2015, approximately 53 percent of AT&T’s 253,000 employees were unionized by Communications Workers of America, the International Brotherhood of Electrical Workers or other unions(Annual Report, p.28). This creates multiple risks for the company. For example, as contracts covering these workers expire, AT&T faces increased risk of work stoppages or other labor disruptions. Also, if AT&T shrinks in the future (as our discounted cash flow model suggests) then unionized workers can become especially challenging given the general difficulty and high costs associated with laying them off.

Less than perfect management incentives: Potential conflicts of interest created by management incentive programs create another risk for AT&T. As mentioned previously, AT&T’s acquisition of DIRECTV helped the company maintain a level of free cash flow sufficient to sustain its high dividend yield. However, it may also have helped senior management achieve some very large short-term performance bonuses. For example, AT&T’s 2015 proxy statement shows that senior management’s short-term performance based compensation is based on specific goals with regards to revenue, earnings per share, and free cash flow. The DIRECTV acquisition helped increase all three. However, as mentioned previously, the acquisition may not have been in the best long-term interest of AT&T shareholders considering it increased debt and added volatility to future returns (not to mention the satellite TV industry has recently been in decline).

It’s also worth noting that senior management’s “long-term” compensation incentives are tied to AT&T’s stock performance over a three year period. Three years is not truly long-term, and it creates incentive for senior management to make short-sighted decisions (such as the DIRECTV purchase).

Worth considering, AT&T management may be pressured to create aggressively optimistic expectations in order to achieve performance bonuses. For example, on page six of AT&T’s most recent 2014 annual report, CEO Randall Stevenson claims “Now that we’ve met our significant network transformation goals ahead of schedule, going forward you can expect us to return to normal capital expenditure levels.” However, the company has already spent $13.4 billion on capital expenditures through the first nine months of 2015, and they’re on pace to spend only slightly less on capital expenditures than they did in each of the last four years. Additionally it’s only a matter of time until AT&T will need to increase spending to match technological advances or simply to prevent its level of service from declining.

Additionally, management may be underestimating the integration costs of DRECTV. For starters, management acknowledges the integration costs by noting that the DIRECTV acquisition is “expected to be accretive within a year after close on a free cash flow per share and adjusted EPS basis.” (Annual Report, p.3). However, management teams have a track record of consistently underestimating the costs and overestimating the benefits of large acquisitions. For reference, check out either of these research reports: Why large M&A deals destroy value (Financial News, Matt Turner, Jan 2012) and The Sources of Value Destruction in Acquisitions by Entrenched Managers (Journal of Financial Economics (JFE), Vol. 106, No. 2, 2012)).

Further, the DIRECTV acquisition is still new, and management and investors may incorrectly extrapolate long-term trends out of short-term performance variances. For example, DIRECTV may experience some positive seasonality from its current “NFL SUNDAY TICKET” that could be misinterpreted as a long-term and consistent trend.

Conclusion:

AT&T may appear to do well in the short-term and its stock price may actually perk up (especially considering management’s significant short-term incentive program). However, we believe AT&T is not a compelling long-term investment because its wireless business can no longer grow fast enough to offset declines in its wireline business, its acquisition of DIRECTV was short-sighted, poorly-timed and increased risk, and AT&T will be significantly hampered if/when interest rates rise from both a market rotation out of dividend stocks and by the need for large contributions to its pension plan. From a total return standpoint (dividends plus capital appreciation), we believe the S&P 500 will significantly outperform AT&T over the next decade, and AT&T shareholders would be better off investing their money elsewhere.