Dividend-growth investing has been one of the most underrated strategies in recent years, however the tide is shifting. Specifically, with interest rates rising, and style leadership now shifting from growth to value, dividend-growth stocks are increasingly attractive and many of them are still significantly undervalued by the market. In this report, we share data on over 100 top dividend-growth stocks (those that have raised their dividend for at least 10 consecutive years), and then dive into four specific stocks that are particularly attractive, undervalued and worth considering as long-term staples in a prudently-diversified income-focused portfolio.

100 Top Dividend-Growth Stocks:

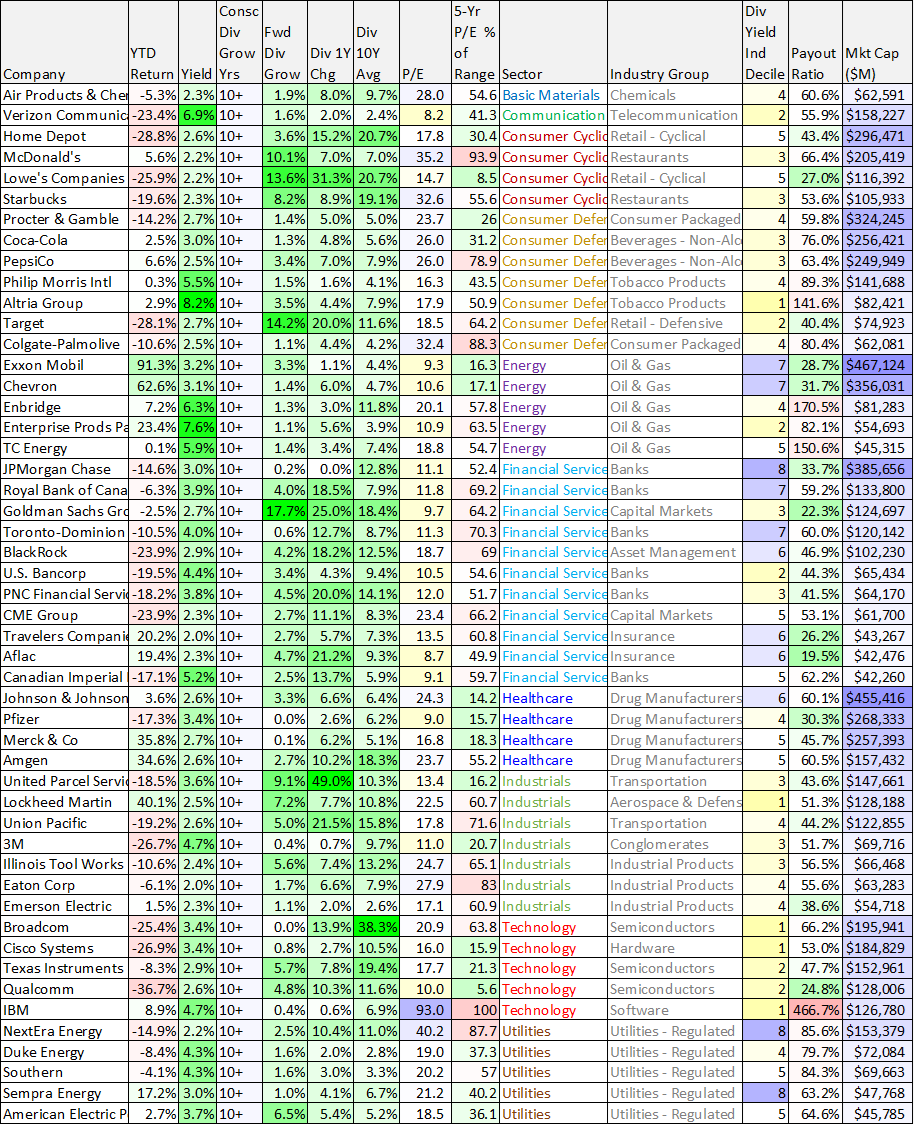

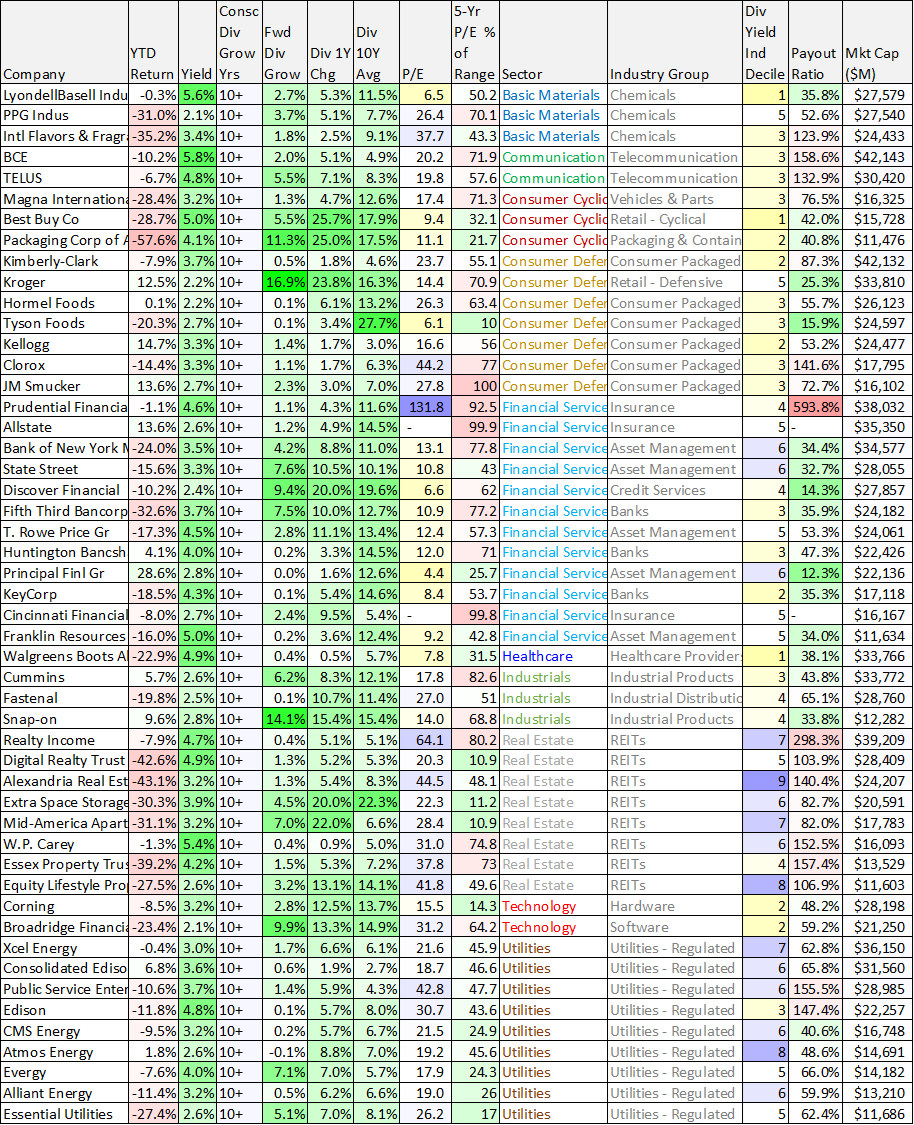

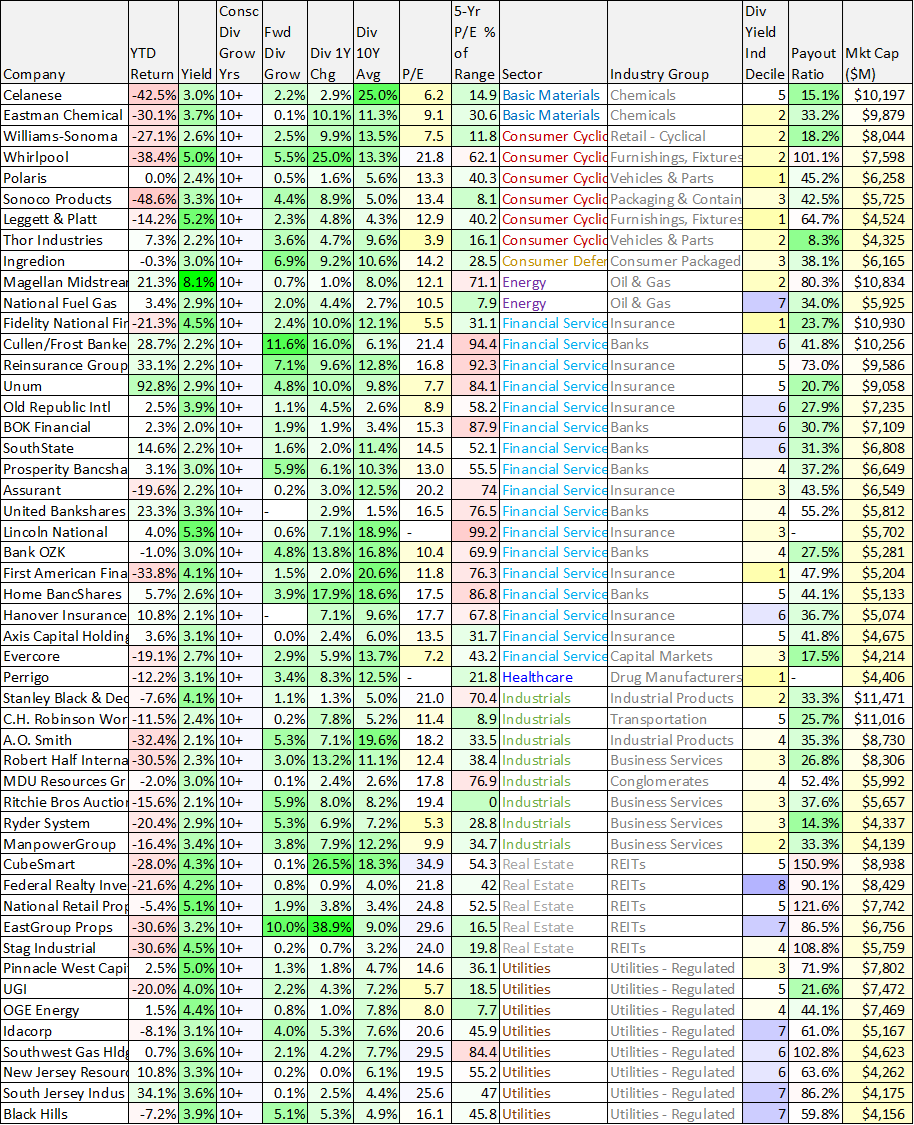

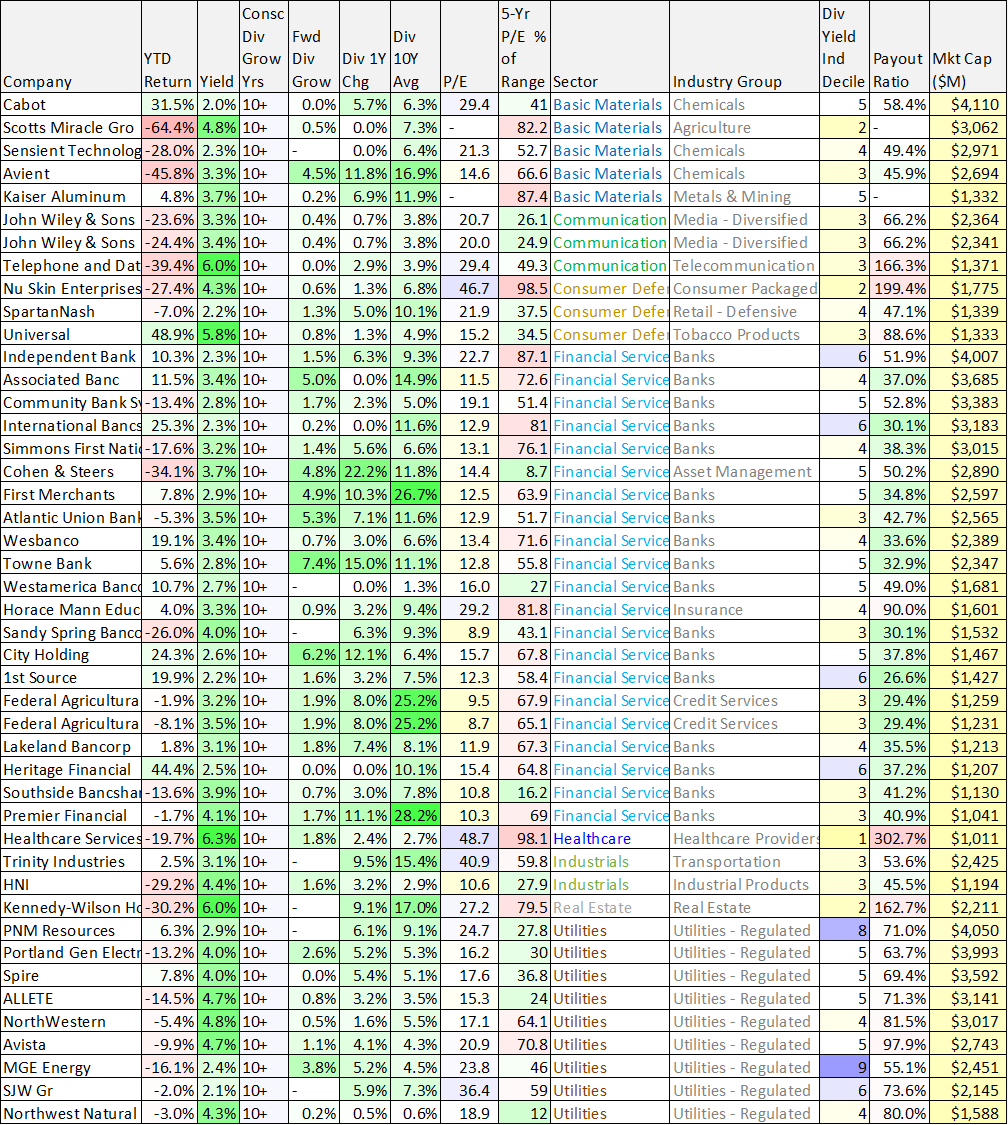

Let’s start with the data. Here is a list of over 100 dividend-growth stocks (those that have increased their annual dividend for at least 10 consecutive years), along with a variety of other valuable data including current yield, the rate of historical dividend increases, payout ratio, P/E ratio, sector, market cap and more. The list is broken into four groups by market cap, and then each of the four groups is sorted by market sector.

data as of midday Mon, Nov 8th. source: StockRover

For your information, here are a few definitions with regards to the column headings in the tables.

Dividend Growth 1-Year Change: the percentage between the last paid dividend and the corresponding dividend 1 year earlier.

Dividend 10-Year Average: the average annual compound dividend growth for the last 10 years based on the last paid dividend and the corresponding dividend 10 years earlier.

5-Year P/E Percent of Range: today's P/E ratio versus the highest and lowest P/E ratios this stock has had over the past 5 years.

Dividend Yield Industry Decile: the decile rank of the company's Dividend Yield among all companies in the same industry. Companies with the highest yields score a 1 and the lowest yielding companies score a 10.

Payout Ratio: dividend payout ratio is Dividend Per Share as a percent of Diluted Earnings Per Share based on the TTM from the most recent quarterly report. Dividend Payout ratio can be used to measure the chance of a dividend increase or cut. For example, a company with a small Payout Ratio has room to increase its dividend.

Growth Versus Value Sectors

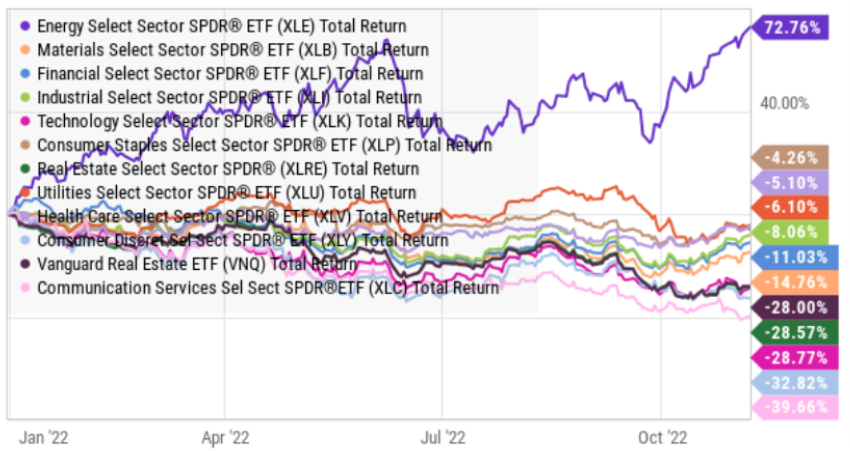

To add a little more perspective to the data in the table, here is a look at the performance of the various market sectors year-to-date. And as you can see, the value sector (such as Energy, Staples, Health Care, Utilities, Industrials and Financials) have performed better than the growth sectors (such as Technology and Consumer Discretionary).

And this year’s growth leadership is in stark contrast to the performance of the last 5 years, whereby growth sectors were more dominant, as you can see in this next chart.

Growth Versus Value (Top Down):

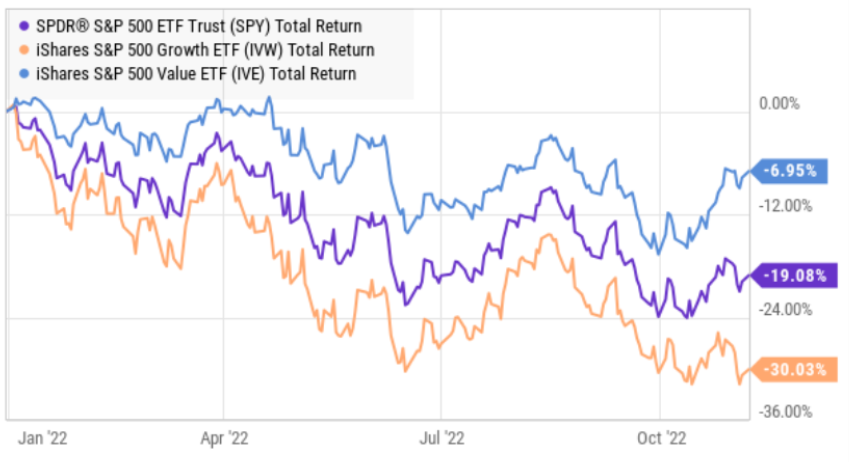

To make this growth-to-value shift more clear, here is a look at the total returns of the S&P 500 this year, versus the S&P 500 Growth and the S&P 500 Value. As you can see, value has significantly outperformed growth this year.

However, the previous 10 years have been a very different story, whereby growth was significantly outperforming value (abnormally low interest rates undoubtedly contributed to growth’s dominance because it was relatively inexpensive to fund growth).

Looking Ahead: Growth Versus Value

However looking forward, it seems unlikely that interest rates will be falling back to the roughly 0% rate of years prior. Specifically, with central bankers focused so strongly on fighting high inflation (the very inflation that was caused by extraordinarily easy monetary and fiscal policies from the Great Financial Crisis and more recently the Covid pandemic), higher rates seem here to stay—and that could support value stocks (over growth) in the years ahead (and as a reversion of the recent years prior).

Dividend-Growth Stock Opportunities

Dividend-growth stocks can offer a unique breed of value opportunities, and because they have been relatively out-of-favor for so long, they could have a lot more upside relative to growth stocks in the years ahead (and based on their lower valuations, such as P/E ratios, some of which you can see in our earlier table).

Dividend Growth “Yield on Cost”

Before getting into specific value-based dividend-growth stock opportunities, “yield on cost” is another important concept to consider. Specifically, a lot of investors avoid dividend growth stocks because there are many stocks that offer higher current yields (but have not grown their yields in the past—and likely won’t grow them in the future either). The reason dividend-growth stocks yields are not the highest current yields available is often because they have been growing the dividend AND their share price, so mathematically the current yield stays relatively lower, but the yield on cost (for example if you bought 10 years ago, or look 10 years into the future) is often MUCH higher. And in absolute dividend dollar terms, dividend growth stocks can pay a lot more after 10 years, just like they pay a lot more now than they did 10 years ago. If you are a long-term investor, it can make A LOT of sense to own dividend-growth stocks, instead of only chasing after stocks with the highest current yields, especially considering current market conditions.

4 Top Dividend Growth Stocks Worth Considering

Taking into account the current shift from growth to value, and assuming interest rates aren’t going back to near-zero anytime soon, the future may be bright for value stocks to outperform growth in a long-overdue mean reversion. Especially for attractive single-stock dividend-growth value opportunities, such as the four we highlight below.

U.S. Bancorp (USB), Yield: 4.4%

US Bancorp is an attractive dividend-growth stock that will benefit from higher interest rates because high rates increase its net-interest-margin profits (i.e. the spread between the rate they borrow at and the rate then lend at widens—thereby increasing profits). Unlike other large banks, US Bancorp in less involved in investment banking (such as IPOs, acquisitions and mergers). This may also be a good thing because where other large banks will miss out on some of the IPO and acquisition buyout revenue when the market was strong, US Bancorp won’t miss it on the way down (granted there could be other increases to investment banking activity such as distress and bankruptcy, but the revenue is still harder to come by in a bear market).

Further, USB is conservative in its payout ratio (see earlier table), its valuation is quite reasonable, and its dividend growth has been (and likely will continue to be) very strong. If you are looking for an attractively-valued, dividend-growth, blue-chip stock, US Bancorp is absolutely worth considering.

State Street (SST), Yield: 3.3%

Similar to U.S. Bancorp, State Street is another financial sector company that could benefit from similar but different factors. State Street is largely a custodian bank (they hold money for investors), and they will also benefit from higher interest rates through better securities lending rates and expanding custody fees. State Street has been raising its dividend aggressively, but the payout ratio is still very low (a good thing) and the valuation is attractively low too. State Street is another powerful dividend growth stock worth considering, especially at this point in the market cycle.

Exxon Mobil (XOM), Yield: 3.2%

It might seem odd to highlight Exxon Mobil as attractive AFTER the shares have already rallied 90%+ this year. However, it is attractive, especially with energy prices higher, because its payout ratio is still very conservative and its valuation is still very low (as it had previously been out-of-favor for many long years). Exxon Mobil is an incredibly profitable business with a truly impressive track record of dividend growth. Going forward, we expect the dividend to keep growing, earnings to keep growing, share buybacks to keep growing and the valuation multiple to expand. Exxon Mobil remains a very attractive, long-term, value-sector, dividend-growth stock.

Natural Fuel Gas (NFG), Yield: 2.9%

Readers may yawn at Natural Fuel Gas, considering it is a “boring” utility/energy sector stock (its four operating segments include Exploration and Production, Pipeline and Storage, Gathering, and Utility—its market cap is about $6 billion), but it has increased its dividend every year for over half a century, its payout ratio is very conservative (lots of room for growth) and the valuation is simply way lower than it should be (as value stocks have been out of favor for so long, and they still are undervalued after this year’s relative strength so far). If you are looking for powerful yet steady dividend growth with health share price appreciation (from earnings growth and multiple expansion) NFG is absolutely worth considering.

The Bottom Line

Value stocks have been out-of-favor for too long, and their share prices are still simply too low as compared to growth stocks, especially considering this year sharply rising interest rates and the momentum value stocks are just starting to gain.

And dividend-growth stocks represent a particularly attractive sub-opportunity within value stocks. In particular, we have shared a lot of data and four specific attractive opportunities that we believe are worth considering if you are a disciplined, prudently-diversified, long-term, income-focused investor.

If the current yield seems too low for your tastes on the four stocks we have highlighted, remember the important concept of “yield on cost,” and remember also these stocks have attractive dividend growth and share price appreciation potential the years ahead.