To some investors, Medical Properties Trust (MPW) has been an obvious short this year, and the shares have sold off dramatically while the dividend yield has climbed to an impressive 9.1%. However, there are reasons to believe the short thesis is now falling apart (for example, fundamentals are improving and macroeconomic headwinds are moderating). In this report, we share comparative data on over 25 healthcare REITs, then review the business of MPW in particular, including a discussion of how its four big risk factors are abating, dividend safety and valuation, and then conclude with our strong opinion on investing.

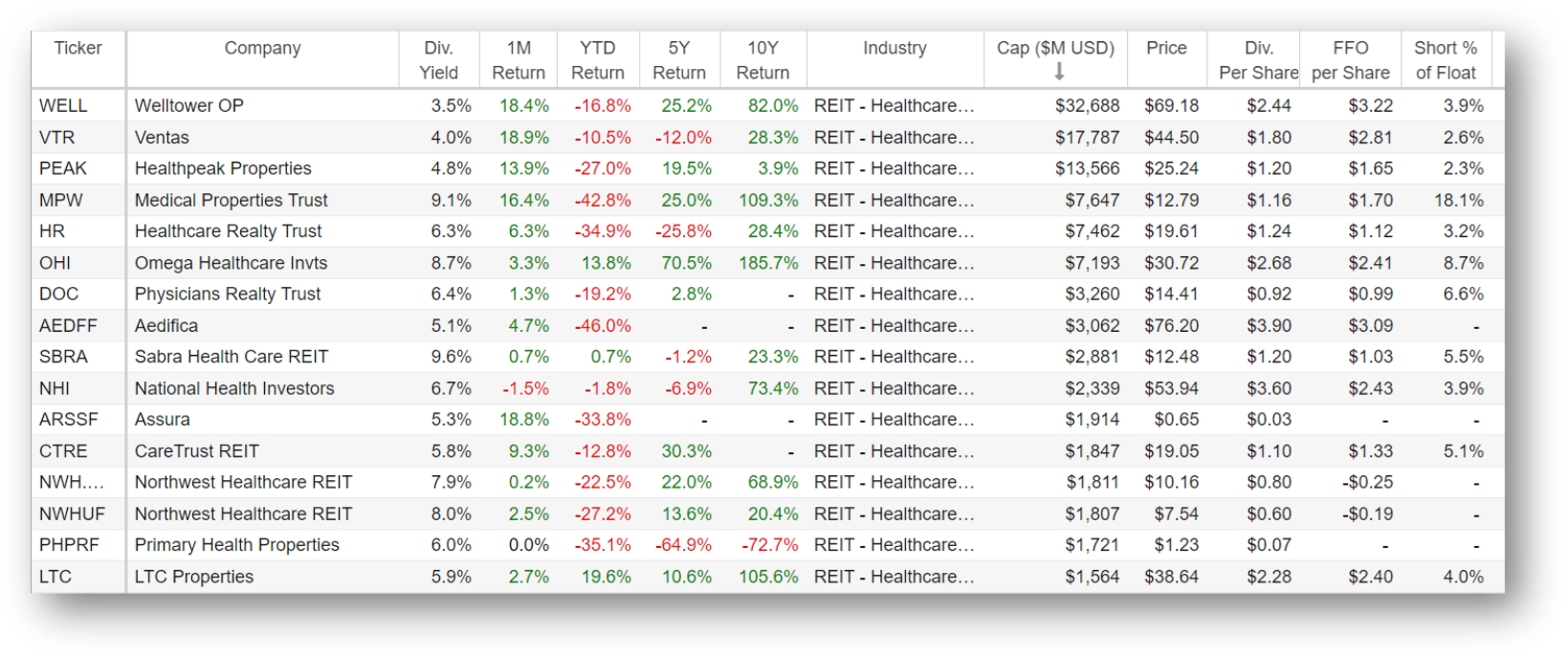

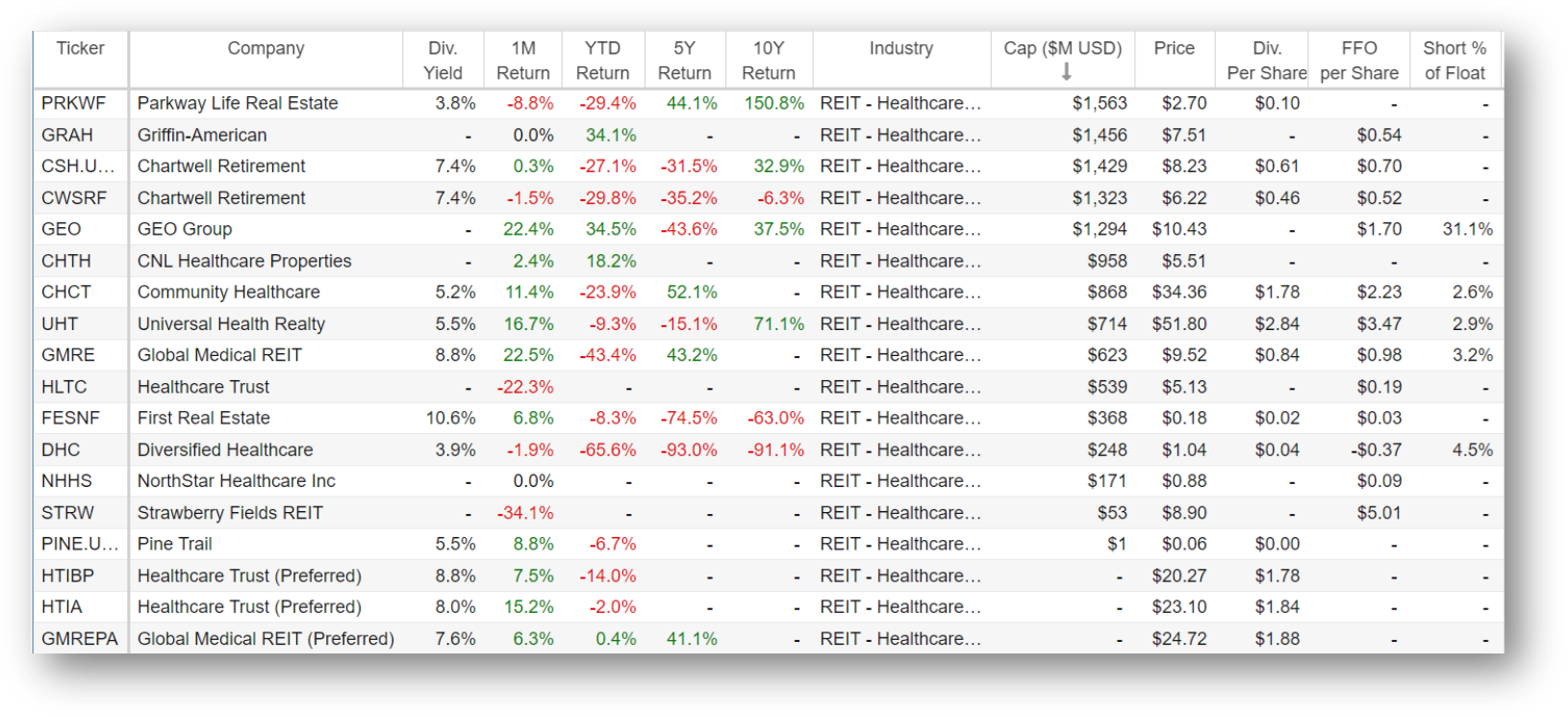

25 Healthcare REITs, Compared:

REITs are as different as apples and oranges. And even within a REIT sub-industry, such as healthcare, they’re as different as Granny Smith and Honeycrisp. Nonetheless, it can still be worthwhile to compare REITs across a variety of data points, such as the metrics in the following table.

The above table is sorted by market cap, and Medical Properties Trust stands out like a sore thumb for its terrible year-to-date performance, massive short interest and big 9.1% dividend yield.

Overview: Medical Properties Trust (MPW)

Medical Properties Trust is “the global source for hospital capital.” Basically, it provides cash to hospitals (often those that are struggling financially) by buying their physical properties (hopefully at a low price, for MPW shareholders’ sake) so the hospitals receive the cash they need to continue (and hopefully improve) their operations.

As we wrote in our previous MPW report:

“In theory, the business model goes something like this. Individual hospitals face dire cost cutting pressures and many of them have gotten into financial trouble whereby it costs them an arm and a leg to borrow capital to improve their operations because lenders don’t trust that they’ll even be able to pay back the loans. MPW can help alleviate this problem by giving the hospitals the cash they need to improve their operations in exchange for ownership of the physical hospital real estate. And MPW can get the real estate for a low price because the hospitals don’t have a lot of other financing options.

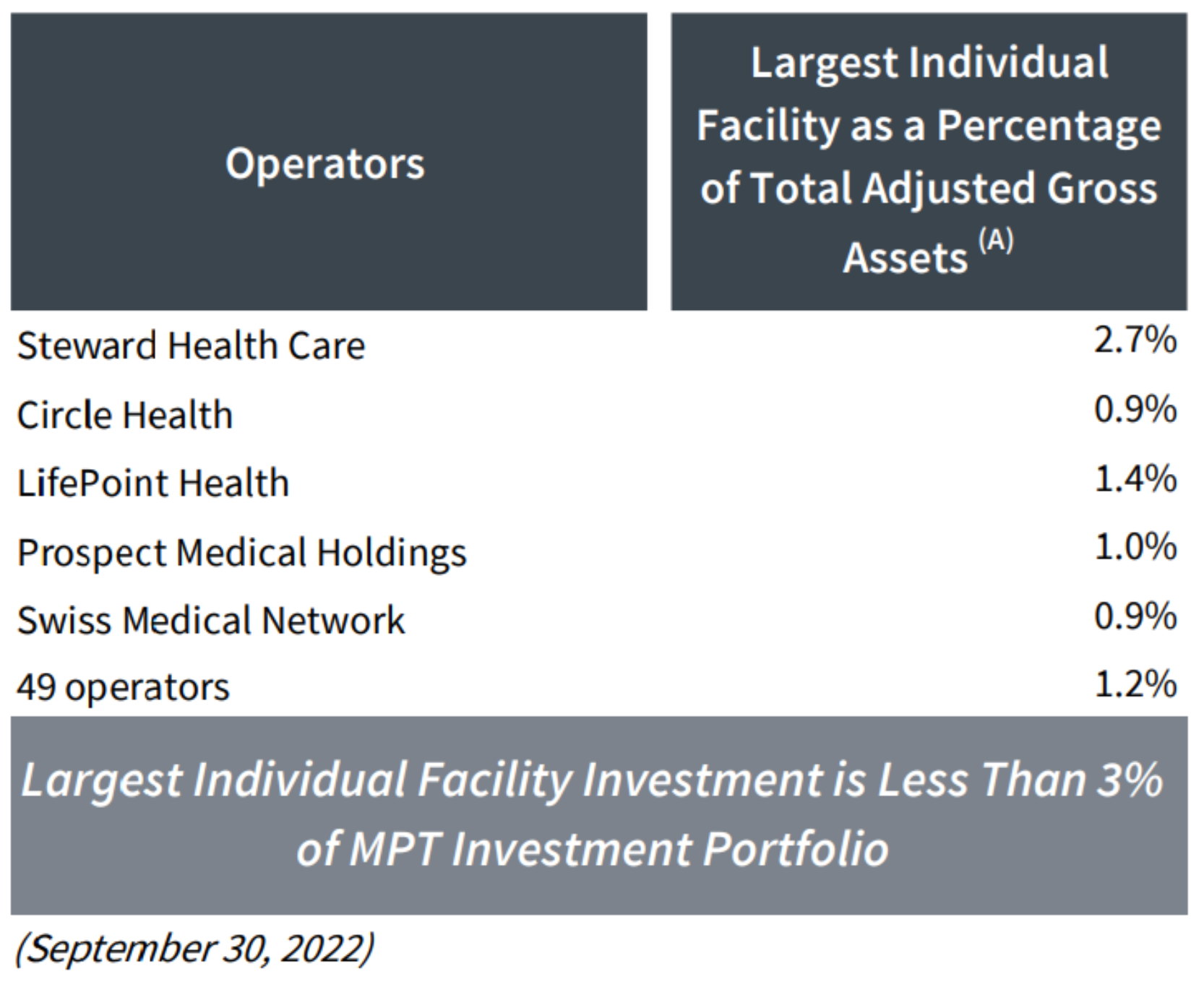

Furthermore MPW is not is great financial shape itself (it has a stable BB+ credit rating, which is below investment grade), but it’s still in much better financial shape than the hospitals themselves. And MPW can reduce its risks by diversifying across many hospitals (it owns hospitals in 32 U.S. states, seven European countries, Australia and South America) which they have done increasingly well over the years (its single largest property is less than 3% of its total portfolio). Furthermore, because MPW is organized as a REIT, it can avoid paying most corporate taxes by paying out most of its income as dividends to shareholders.

Basically, … [MPW] has the financial wherewithal to provide much needed capital to hospitals while simultaneously reducing risks through portfolio diversification and its own lower cost of capital as compared to the at-risk hospitals themselves.”

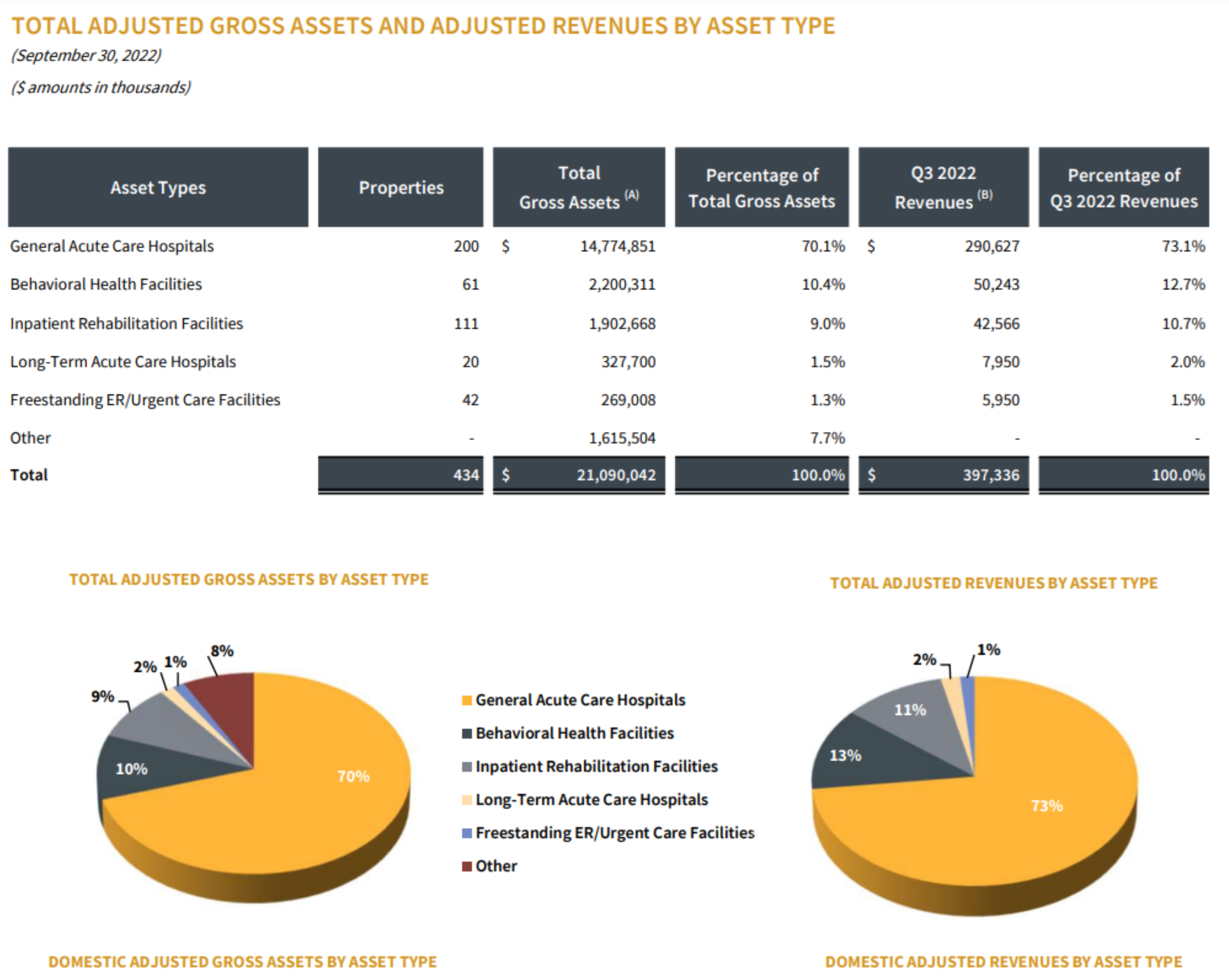

Specifically, here is a look at MPW’s updated portfolio assets, as of the end of Q3.

Four Big Risks: Overblown and Abating

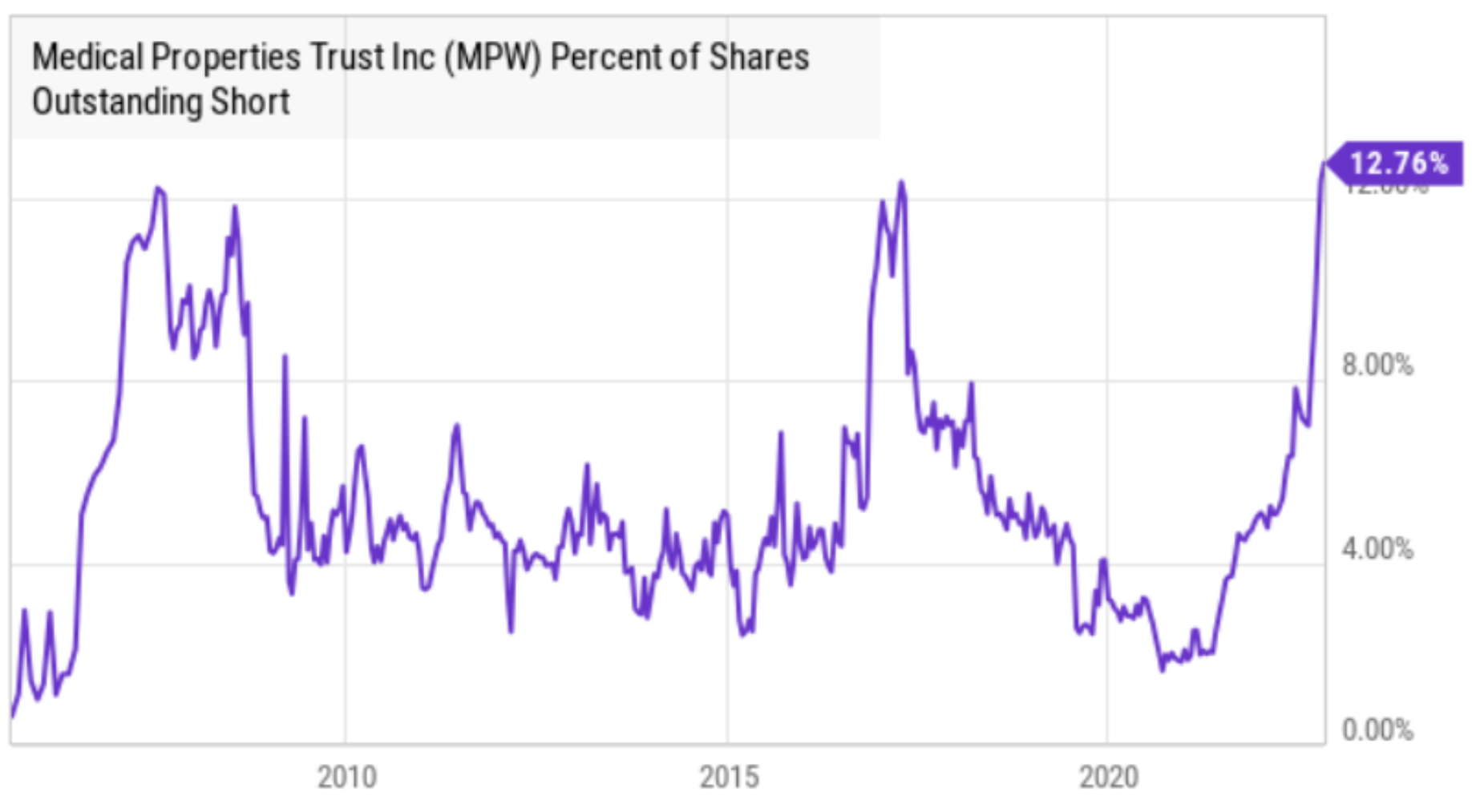

Aside from MPW’s big yield and terrible share price performance, you may have also noticed in our earlier table that it also has very high short interest (i.e. people betting against it by selling the shares short).

There are four big reasons (i.e. risks) for all the negativity, and they are arguably all improving, as we will explain below.

1. Troubled Operators: fundamentals are improving

Perhaps the number one reason MPW shares have sold off so hard this year is because many of its hospital operators were struggling to begin with and then pushed closer to the brink by pandemic challenges (such as increasing costs and risks). However, according to CEO Ed Aldag on the third quarter call, conditions are starting to improve and will continue to do so. Specifically, he explained:

“As our operators effectively work to bring down cost and as reimbursement rates increase, we expect to continue to see coverages improving within our portfolio.

It’s also important to recognize the total portfolio is well diversified and the trouble operators are relatively small (as you can see in the following table). However, to keep this in perspective, and per MPW’s most recent annual report.

Our revenues are dependent upon our relationships with and success of our tenants, particularly our largest tenants, like Steward, Circle, Prospect, Swiss Medical Network, and HCA… As of December 31, 2021, our largest tenants – Steward, Circle, Prospect, Swiss Medical Network, and HCA – represented 18.5%, 11.1%, 7.3%, 5.8%, and 5.6%, respectively, of our total pro forma gross assets (which consists primarily of real estate leases and loans).

Furthermore, Bank of America analyst, Joshua Dennerlein, recently upgraded the shares to “Buy,” explaining that “we expect the Steward ABL to be permanently extended in December, and management has alluded to a multi-party transaction involving Prospect." These are good signs for two of MPW’s largest operators (see table above). Dennerlein also noted that “tenants should start to see improving fundamentals from payor rate hikes, improving labor markets and slowing inflation.”

Further, MPW announced encouraging financial results during its most recently quarterly call whereby the company announced FFO in-line with expectations and it also raised the lower end of its guidance range. It’s also important to note that the hospitals are strategically important to the communities in which they exists, an indication of further portfolio value.

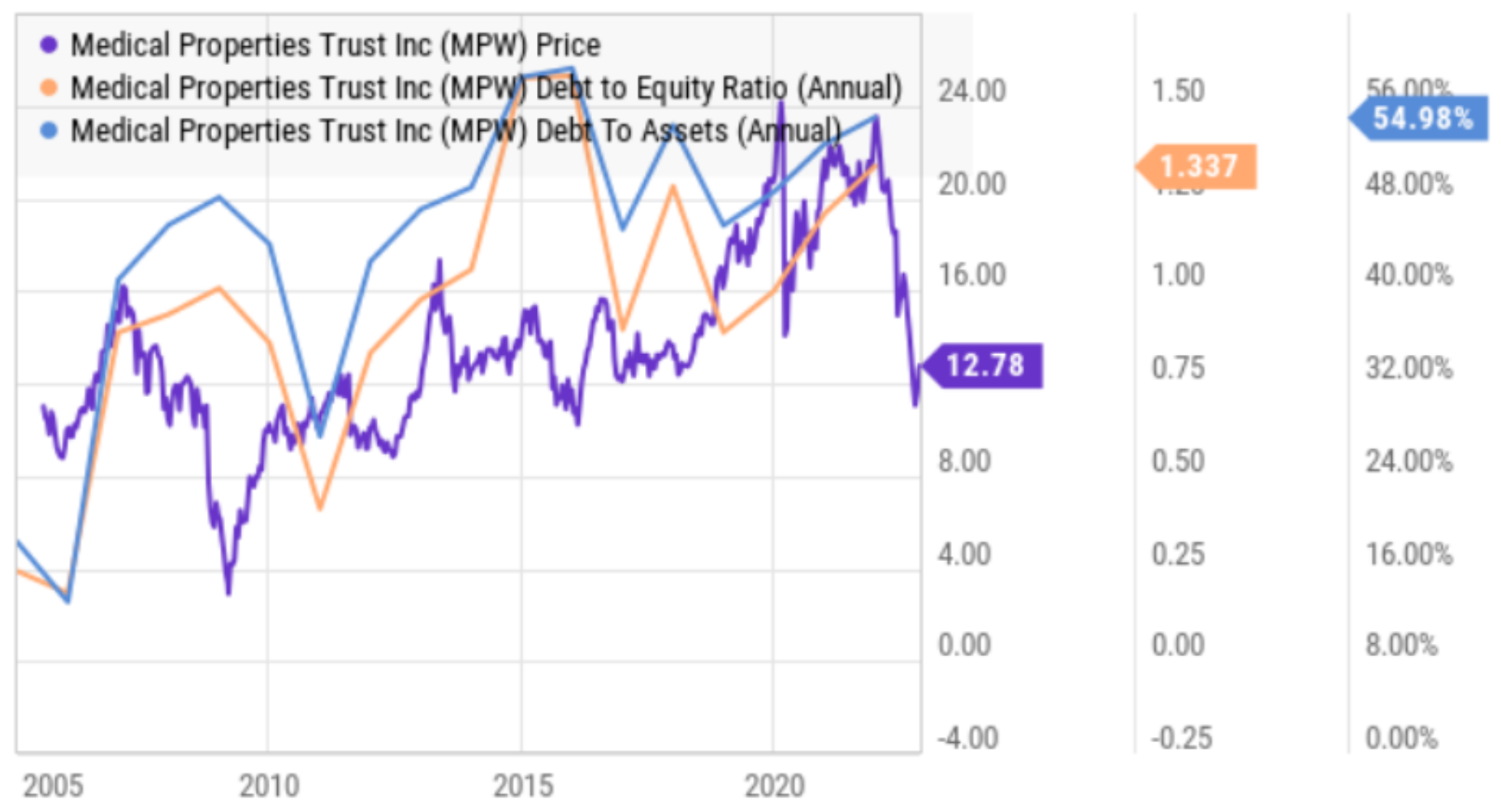

2. Significant Debt: Risks are Reducing

It’s also critically important to note that improving fundamentals will help reduce the risks related to the company’s significant debt load. Specifically, MPW currently has a debt-to-assets ratio of 55% and debt-to-equity of around 1.3x. These are significant, and the company has a credit rating of BB+/stable (from Standard & Poor’s), just barely still investment grade.

However, the companies improving fundamentals (as noted in the previous section) are a very good sign for the debt. A big part of the reasons for this year’s share price decline has been the risky operators and fundamentals. However, with conditions now improving, the high debt load risks are reducing.

3. Rising Interest Rates: Massive Fed Pivot

Another factor in this year’s steep MPW share price decline has been sharply rising interest rates from the US fed. In a complete 180 from its easy-money policies during the pandemic, the fed is now raising rates rapidly to combat high inflation (a high inflation rate they helped create in the first place), and this has been slowing the economy and crushing companies with higher risk debt (as rates rates, it costs more to refinance debt when it matures). The fed’s policies have been hurting MPWs significantly.

However, there are reasons to believe the fed may soon embark on another massive pivot. Specifically, the most recent CPI and PPI inflation readings have been lower than expected, an indication that the fed may NOT need to be so aggressive with interest rate hikes and a good sign for MPW. In fact, the same Bank of America rating update (to “Buy”) that we discussed earlier, also cites “a pivot to a more dovish Fed is a positive for this high yielding REIT."

We could offer up a litany of subjective arguments as to why the fed’s continuing interest rate hike trajectory is not believable anyway (such as (1) they cannot raise rates much further because it will crush the US economy under the weight of the interest rate payments on its own treasuries, and (2) they’ve already gone way too far (and too fast) with rate hikes considering the impacts are always lagged by 6-18 months anyway). Also noteworthy, fed fund futures are already predicting the first fed interest rate decrease before the end of 2023. Slowing rate increases (and eventually an interest rate decrease) bodes well for MPW.

4. Industry-Specific Risks: Hospitals are important

Industry-specific risks are another critical factor. For example, hospitals are heavily regulated and rely on government funding through a variety of sources, such as Medicare and Medicaid. And as the government is constantly pressured to reduce the growth rate in these costs, regulatory changes pose a significant risk for MPW. Additionally, if any hospital operator ceases operations for financial reasons, it may be difficult for MPW to find a replacement. For example, MPW has been successful in attracting private-equity capital in the past, but there is no guarantee they will have similar success in the future.

However, an important factor is simply that the hospitals MPW owns are strategically important to the communities in which they exists. Specifically, there is incentive from the communities, governments and MPW to enable the hospitals to remain a going concern. For example, here is what CFO Steve Hamner had to say on the Q2 earnings call:

…the absolute certainty that governments and people are going to support their infrastructure like hospitals. And so all of that has led to a very high level of interest in the private area, and that's with sovereigns and pension funds and asset managers and people like you just mentioned KKR.

This is further evidence of the value of MPWs assets.

Dividend Safety

An important consideration for MPW investors is simply that the annual dividend has increased for nine years straight and it continues to be well covered by funds from operations. For example, you can see in the following chart that company’s adjusted funds from operations (“AFFO”) of $0.36 and $1.08, respectively, exceeds the dividend amount for these periods of $0.29 and $0.87, respectively.

Also encouraging, the company’s fundamentals are improving, as described earlier.

Valuation:

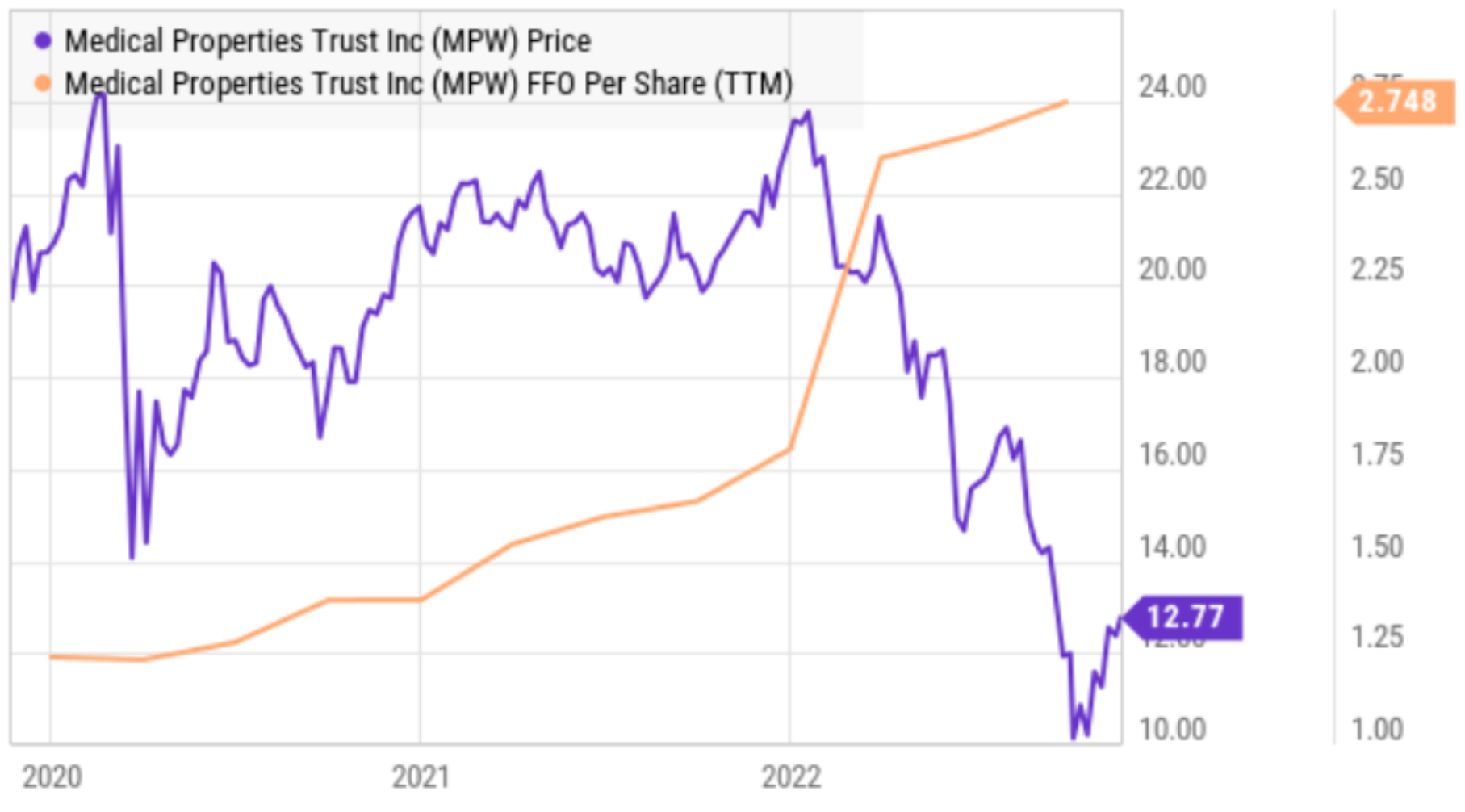

MPW’s valuation has fallen because there are significant risks, as described above. However, it has arguably fallen significantly too far. For starters, here is a look at MPW’s share price versus its Funds from Operations (“FFO”).

As you can see above, FFO has held up well over the past 12 months, while the share price has fallen in anticipation of potential risks as described above. However, it now trades at a forward P/AFFO ratio (~9.0x) that is very low as compared to peers, and the fallout from potential risks may not be nearly as extreme as feared.

Next, here is a look at MPW’s share price versus its book value per share.

And again, the book value has held up very well versus the share price—an indication the shares are undervalued. Granted, if any operators cease to be a going concern (which is unlikely considering their strategic importance to the communities in which they exists) that will create challenges, but those challenges appear less severe than the market fears, in our view.

Also worth noting, Medical Properties Trust recently announced its board authorized the repurchase of up to $500M of stock before October 2023, perhaps a strong indication of value.

Conclusion:

MPW is not appropriate for the most risk averse investors. However, MPW may be worth considering if you can tolerate the volatility and if you hold it within the constructs of a prudently-diversified long-term portfolio. In our opinion, the shares are particularly compelling if you consider the improving fundamentals combined with the potential for a massive short-squeeze (i.e. short-sellers may be forced to cover as conditions improve—which would drive shares higher) and quite possibly an epic fed pivot (as inflation slows, so too may the interest rate hikes that have been hampering MPW). We currently own shares of MPW within our Income Equity Portfolio and look forward to receiving large dividends combined with the potential for significant share price appreciation.