If you are looking for a unique combination of dividends, growth and value, this 5G-related technology stock is worth considering. The 2.0% yield may not seem high, but it has strong history (and trajectory) of growth, and so does the overall business. It also has an attractive valuation (thanks to short-term market forces), especially considering the large total addressable market and future growth opportunities. In this report, we review the business, the market opportunity, the dividend, valuation and risks. We conclude with our opinion on investing.

Overview: Qualcomm (QCOM)

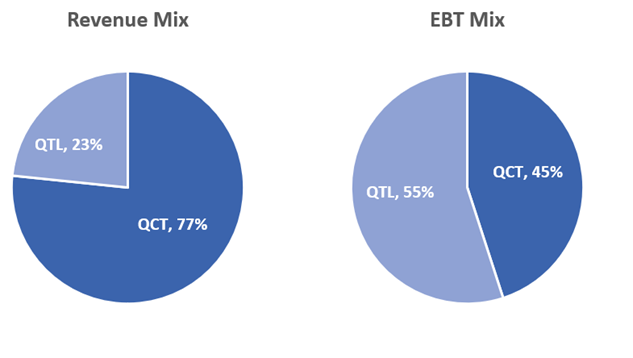

Qualcomm Inc. (QCOM) is a leading semiconductor and wireless technology company. Its technologies and products are used in mobile devices, PCs, network equipment, consumer electronic devices and other IoT devices. It primarily operates via three segments: QCT (Qualcomm CDMA Technologies), QTL (Qualcomm Technology Licensing) and QSI (Qualcomm Strategic Initiatives). Of these three, the majority of the revenue comes from QCT and QTL.

QCT: develops and supplies integrated circuits and system software based on 3G/4G/5G and other technologies.

QTL: derives revenue in the form of royalty earned from granting licenses and rights to use company’s IP for manufacturing wireless products;

QSI: QCOM venture capital arm QCOM, responsible for making strategic investments.

source: Company data

The share price has recently declined, however it seems the adverse impacts of the pandemic is now behind the company. For example, smartphone sales declined, but have since recovered. And this, combined with the rapid global roll-out of 5G, should continue to benefit the company. This appears evident in Qualcomm’s Q2 2021 results, where revenue jumped more than 50% to $7.9 billion, up from $5.2 billion in Q2 2020, driven primarily by a 55% rise in chipset sales ($6.2 billion in Q2 21 vs $4.1 billion in Q2 20). Operating income jumped 2.2x (from $991 million to $2.17 billion in Q121), and EPS increase more than 3x. And as 5G rolls on, we expect the company to continue to benefit in the medium-term.

5G Accelerating Globally

The increasing adoption of 5G globally presents a significant long-term opportunity for Qualcomm. Over 140 operators have launched commercial 5G service in nearly 60 countries so far. Further, ~270 additional operators have plans to move to 5G. Qualcomm expects 1 billion 5G connections in 2023, which is 2 years quicker than the same mark in 4G. And 5G adoption in smartphones continues to be strong. In 2020, nearly 225 million smartphones were sold with 5G, according to Qualcomm. And this is expected to grow to 500 million at the midpoint in 2021.

source: Company Presentation

And Qualcomm will benefit as more smartphones sales will result in increased chipset sales and license revenue. And in addition to smartphones, Qualcomm estimates literally billions more intelligent devices will use 5G. The IHS Markit 5G Economy Study estimates that 0ver $13 trillion of economic activity will be enabled by 5G by 2035. Qualcomm CEO, Steve Mollenkopf has noted that “5G represents the single largest opportunity in our history”.

Part of the smartphone 5G story is the increasing prospects for RF front-end solutions. Beyond smartphones, RF front-end solutions are experiencing growth in automotive, PCs, mobile hotspots, fixed wireless access in the broad IoT category. Of note, QCOM has set an RF front-end revenue target of $3.6 billion by fiscal year 2022. RF Front-end revenue stood at $903 million in Q2 2021, up 39% YOY.

5G is also expected to accelerate the pace of innovation in many industries such as automotive. Approximately 70% of new vehicles produced in 2025 are projected to have cellular connectivity, compared to 48% in 2019, according to Strategy Analytics. Qualcomm already has a significant presence in the automotive sector. It has secured infotainment and digital cockpit wins with 20 of the 25 largest global automaker brands. The automotive backlog has increased from $5.5 billion in February of 2019 to $9 billion currently. And this is expected to keep growing as the company moves into new segments such as digital chassis and ADAS.

The Qualcomm management team noted the following during J.P. Morgan 49th Annual Global Technology, Media and Communications Conference:

“the next 2 growth areas for us in this segment is what we call the digital chassis. As automotive industry change to electrification, you're really building a computer on wheels. You need a high-performance, power-efficient connected computer. We have an opportunity to replace a lot of the existing incumbent technology with our high-performance processors in the car, and we're going to apply NUVIA CPUs to the automotive segment as well. So the digital chassis becomes another one, and then ADAS.”

The next growth opportunity for 5G is IoT (the “Internet of Things”). The addressable market for 5G uses in IoT devices is increasing rapidly. The company did over $1 billion in revenue during the latest Q2. The management team also noted the following:

“The IoT one, we're just scratching the surface of the TAM. So unlike auto, which is an easy-to-understand TAM, in the case of IoT, it's a fast-growing TAM. The way you should think about our IoT business and now the way I like investors to think of Qualcomm when you look at our IoT business, if you buy the growth of the hyperscalers and everything going to the cloud, Qualcomm devices at the edge are going to be the ones generating the data and connecting with the cloud.”

Large addressable market

Qualcomm has a long runway to keep growing. The company estimates its total addressable market opportunity to be ~$100 billion by 2022 (up from ~$65 billion in 2019), as per its latest Q1 presentation. Of this figure, the handset market is estimated to grow at a 3-Year CAGR of 10% from $26 billion in 2019 to $35 billion in 2022. And Qualcomm expects to grow faster than the overall handset market. In the RF Front-end market, the addressable market is estimated to reach $18 billion by 2022, representing a CAGR of 12% during 2019-2022. The company is targeting ~20% market share for this market by 2022, which implies revenue of ~$9 billion. We note that the current annual revenue run rate is close to $4 billion (based on latest Q2 numbers).

In the automotive segment, the opportunity size is expected to reach $4 billion by 2022, while in the IoT segment it is expected to touch $13 billion by 2022.

source: Company Presentation

Dividend – Safe and Growing

Qualcomm has a strong history of growing its quarterly dividend, and it has the financial strength to continue increasing the dividend going forward. While some investors may balk at the 2.0% dividend yield, they shouldn’t. 2.0% yield is greater than the S&P 500, and the company’s growth (both dividend growth and revenue growth) exceed that of the S&P 500. This is a stock where long-term investors should not overlook the power of “yield on cost.” Specifically, the yield may appear lower than other dividend stocks, but when you factor in the rising stock price and growing dividend payments—ten years down the road your “yield on cast” can be quite impressive. For perspective on the company’s cash flow strength, it returned $2.3 billion to stockholders during the quarter, consisting of $734 million in dividends and $1.5 billion in share repurchases.

source: Company Presentation

Valuation:

Qualcomm currently trades at ~4.3 times 1-year forward sales, which is attractive compares to its strong revenue growth and large total addressable market. It’s also compelling as compared to its own history.

Further, the shares trade at just 19 times earnings, also highly compelling as investors have fearfully sold off the shares this year as the “pandemic trade unwinds” and chip shortages weigh on investors minds. However, long-term, this business simply has too much going for it for the shares to trade at this low of a multiple, especially considering the strong outlook, accelerating 5G transition and high margins (~33% forward EBITDA margin is attractive).

Risks:

Semiconductor Supply Shortage: One of the main concerns for QCOM is an acute supply shortage for a variety of semiconductor chips. Qualcomm’s ability to meet customer demand is largely dictated by the production capacity of Taiwan Semiconductor (TSM) and Samsung. However (and importantly) the company sees the shortage easing later this year.

High customer concentration: Qualcomm has a relatively high customer concentration, which is a risk. For example, top customers include Apple, Oppo, Vivo, Samsung, Xiaomi, and Huawei, each accounting for more than 10% of QCOM total revenues. In the past, Qualcomm has faced legal challenges from several of those customers with regards to it licensing fees. However, Qualcomm won the cases, and continues to sit relatively pretty considering the importance of its chips to those customers.

Competition: Apple is planning to develop its own 5G wireless modem chips for its iPhones and other devices. This remains a risk for Qualcomm, but Apple’s licensing deal with Qualcomm is valid through 2025. This means that Apple will continue paying royalties to Qualcomm until at least that time.

Conclusion:

Overall, Qualcomm is attractive. The shares have recently sold-off as investors have concerns over chip shortages and customer concentration (i.e. Apple is attempting to develop its own chips). In our view, the fears are overblown, and investors would be better served to take the long view. Specifically, Qualcomm is an industry leader with a high growth rate, a large total addressable market opportunity, and tailwinds as we come out of covid and as chip shortages are expected to abate. It trades at an attractive valuation, and we expect healthy dividend to keep growing in the years ahead. We do not currently own shares of Qualcomm, but if you are looking for a unique combination of dividends, growth and value—Qualcomm is worth considering. It is high on our watchlist, and we may add shares in the relatively near future.