Main Street Capital (MAIN) is a popular BDC (business development company) thanks to its big monthly dividend payments (which have never been reduced in the history of the company). Main Street provides financing solutions to a wide variety of smaller businesses—many of which were incidentally hit particularly hard by covid. The shares have not yet recovered to their pre-covid level, and in this report we review the business, the financials, the dividend, the risks and finally conclude with our opinion on investing.

Main Street Capital (MAIN), Dividend Yield 6.3%

Main Street invests in private debt and equity. More specifically, it provides debt and equity financing solutions to lower middle market companies (i.e. companies with annual revenues between $10 and $150 million). The companies are highly diversified across industries, as you can see in the following chart.

From a high level, Main Street has $4.3 billion in capital under management, consisting of $3.3 billion internally managed at MAIN and $1.0 billion where MAIN is the investment advisor to external parties. More specifically, MAIN’s total investment portfolio (at fair value) consists of approximately 48% Lower Middle Market investments, 27% Private Loans, 17% Middle Market investments, and 8% “Other” portfolio investments. The company also makes a concerted effort to be diversified across geographies.

Also important to note, because MAIN is internally managed (and management invests significantly in MAIN) there are far less conflicts of interest (as compared to externally managed BDCs), and main is able to maintain a significantly lower operating expense ratio (a good thing!).

Recent Business Performance (Risk vs Reward):

Like many financial industry companies, Main Street’s share price took a hit as a result of the pandemic. And as you can see in the following chart, the shares have not fully recovered from the early 2020 pandemic sell off (unlike other financial companies that have recovered).

These differences in performance highlight a critically important distinction about MAIN’s business that often gets overlooked. Specifically (and despite MAIN’s very competent management team) the types of things MAIN invests in are riskier than the types of things a typical “bank” would invest in. More specifically, banks often provided financing in the form of very large and relatively low risk loans. On the contrary, MAIN provides financing (loans and equity stakes) to smaller (Lower Middle Market) businesses that are often too small and too risky for traditional banks to consider. The tradeoff is that the types of things MAIN invests in can provide higher long-term returns (and they have—see chart above), but more risk and volatility (for example, MAIN sold off a lot more during the financial crisis). This is the risk-reward tradeoff for those that invest in MAIN. And it is a risk worth taking for many investors, especially considering the big steady dividend payments MAIN has historically been able to provide (and we believe MAIN will keep providing big steady dividend payments going forward too).

Main Street describes its own business as “niche,” and they believe they have carved out their own unique space in the market where they can deliver strong shareholder returns through their specific expertise in this niche. We agree. As long as investors understand what they are actually investing in, as well as the potential risks/rewards, we believe MAIN is attractive for income-focused investors (especially at the current share price—we expect the business to continue recovering from the pandemic).

Main Street’s Advantages

Before we go further, it’s worth highlighting a few of MAIN’s unique advantages, including:

Niche: “lower middle market” strategy

Internally managed: with lower operating expenses and less conflicts of interest.

Founder led: the CEO, President and Executive Chairman are all three co-founders of the firm.

SBA Advantage: Main Street invests with small business association subsidiaries, thereby providing access to lower cost, long-term fixed rate loans guaranteed by the US government.

RIC Tax Structure: This structure eliminates corporate level income tax, providing efficient high yield to investors (it passes through capital gains to investors).

Monthly Dividend: Investors often appreciate the monthly dividend payments, and the company’s current distributable net investment income exceeds the dividend payment amount (a good thing!).

Senior Financing: MAIN provides single source solutions (including a combination of first lien, senior secured debt and equity financing) which puts it in a senior position and simplifies workouts when necessary.

Interest Rate Sensitivity: 78% of MAIN’s outstanding debt obligations have fixed interest rates (limiting the increase in interest expense), however 71% of MAIN’s debt investments bear interest at floating rates (MAIN benefits if rates rise).

Growing Asset Management Business: MAIN continues to grow this bases providing a steady and diversified income stream.

Financial Strength / Pandemic Recovery:

As mentioned, many of MAIN’s portfolio companies (i.e. the business it provides financing to) were hit hard during the pandemic. We often heard the media discussing how small businesses were hit harder by the lockdowns, and this was true of MAIN’s portfolio companies in aggregate (for example, MAIN provides financing to ~175 lower middle market companies).

For perspective, you can see in the following chart that MAIN’s investment income (one of the most important metrics for a BDC) took a hit in 2020.

However, MAIN is already on a path to recovery as quarterly numbers have been improving, and the company already exceeded expectations in its most recent quarterly financial update. For example, you’ll notice in the first row of the following graphic that the most recent Q4 investment income number has jumped (after falling hard in the 2nd and 3rd quarters of 2020 as the economy dealt with the pandemic).

You’ll also notice that Distributable Net Investment Income, or DII, (the bottom row, and another critically important metric for a BDC) has been on the rise (after struggling in the 2nd and 3rd quarter of 2020 due to the pandemic). These metrics bode well for MAIN and suggest it is increasingly turning the corner after the pandemic challenges.

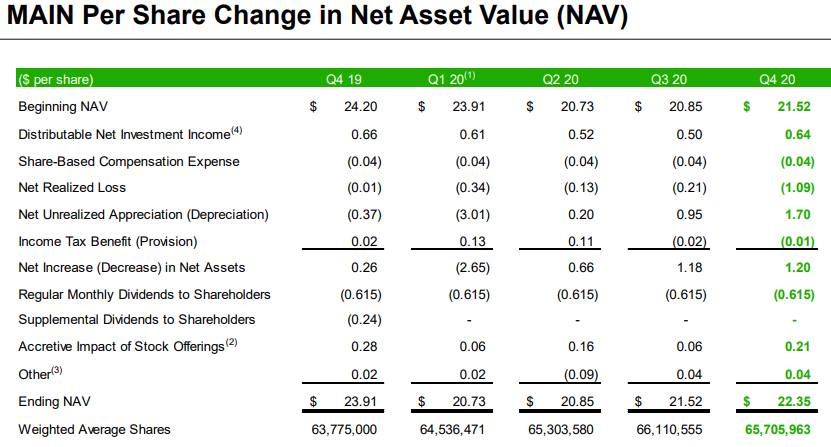

However, we’d be remiss not to mention that the company’s net asset value (“NAV”) was significantly and negatively impacted by the pandemic, as you can see in this next table (specifically, despite some recovery, NAV still remains below Q4 2019).

For additional color, you can see which part of MAIN’s balance sheet were impacted (and how) during the pandemic in this balance sheet table.

For example, the value of the middle market portfolio is still down, while private loan activity has increased, and cash balances are down.

Lastly for this section, you can see that overall liquidity has ticked lower, debt ratio has increased, and interest coverage as increased.

These are concerning metrics (and the reason why the share are still down), but metrics have been improving in the most recent quarter—some proof that the business is turning the corner from the pandemic. Also critically important to note, the company’s distributable net investment income still exceeds the dividend payment amount (a very good thing!).

The Dividend

As you can see in the following chart, MAIN has a long history of paying attractive monthly dividends. The dividend has never been reduced, not even during the pandemic (see gray bars below).

Also important to note, the company does have a history of paying special supplemental dividends when Distributable Net Investment Income (“DNII”) allows it (a good thing for income-focused investors).

More recently, as you’ll not in the chart above, DNII again exceeds the dividend (a critically important thing in the long-term) as MAIN continues to strengthen following the pandemic. Another important metric in the chart above is the company’s net asset value (NAV) per share. This is the value of all the investments on MAIN’s balance sheet (i.e. the assets that the company can use to generate income). The NAV took a significant hit during the pandemic as MAIN was forced to work through significant challenges within its book of portfolio companies. However, importantly, NAV is also now on the rise (a good thing).

Risks:

Main Street’s business does face a variety of risks. Firstly, the types of companies MAIN provides financing to are inherently more risky with regards to their smaller size and the fact that they often include the types of risks that more traditional banks try to avoid (i.e. shorter track records, less stable cash flow, less liquid collateral assets). However, MAIN’s competent management team has carved out a niche in this space and has a growing long-term track record of success throughout market cycles.

Interest rates are another risk. It is true that much of the financing MAIN has provided is tied to interest rates (i.e. floating rate loans), which means the borrowers pay more money to MAIN if/when rates rise. But realistically, if rates rise too much then the borrows may simply not be able to pay.

Overall macroeconomic conditions are another risk for Main Street. Specifically, if the economy turns south, MAIN could get hit harder than other businesses. We just recently saw an example of this from the covid pandemic whereby MAIN shares sold off harder that many other publicly traded securities. However, we view this as an opportunity, as the economy and the company appear to be turning the corner and have more upside potential ahead.

Conclusion:

Main Street is an attractive BDC that offer a compelling 6.3% dividend yield. When macroeconomic conditions are healthy, Main Street is a highly attractive business because of its well-diversified high-return investment portfolio and competent management team. However, when economic conditions turn south, BDCs (and Main Street in particular) can be hit very hard—as the company just experienced during the pandemic.

However with the economy now turning the corner, Main Street is on a continuing road to recovery. The shares have already shown strong improvement in the most recent quarterly earnings announcement, and we believe there is significantly more improvement and upside in the quarters and years ahead. And considering the healthy monthly dividend payments, these shares are particularly attractive for income-focused investors.

We currently own shares of Main Street Capital (MAIN), and we expect continuing dividends and price gains ahead.